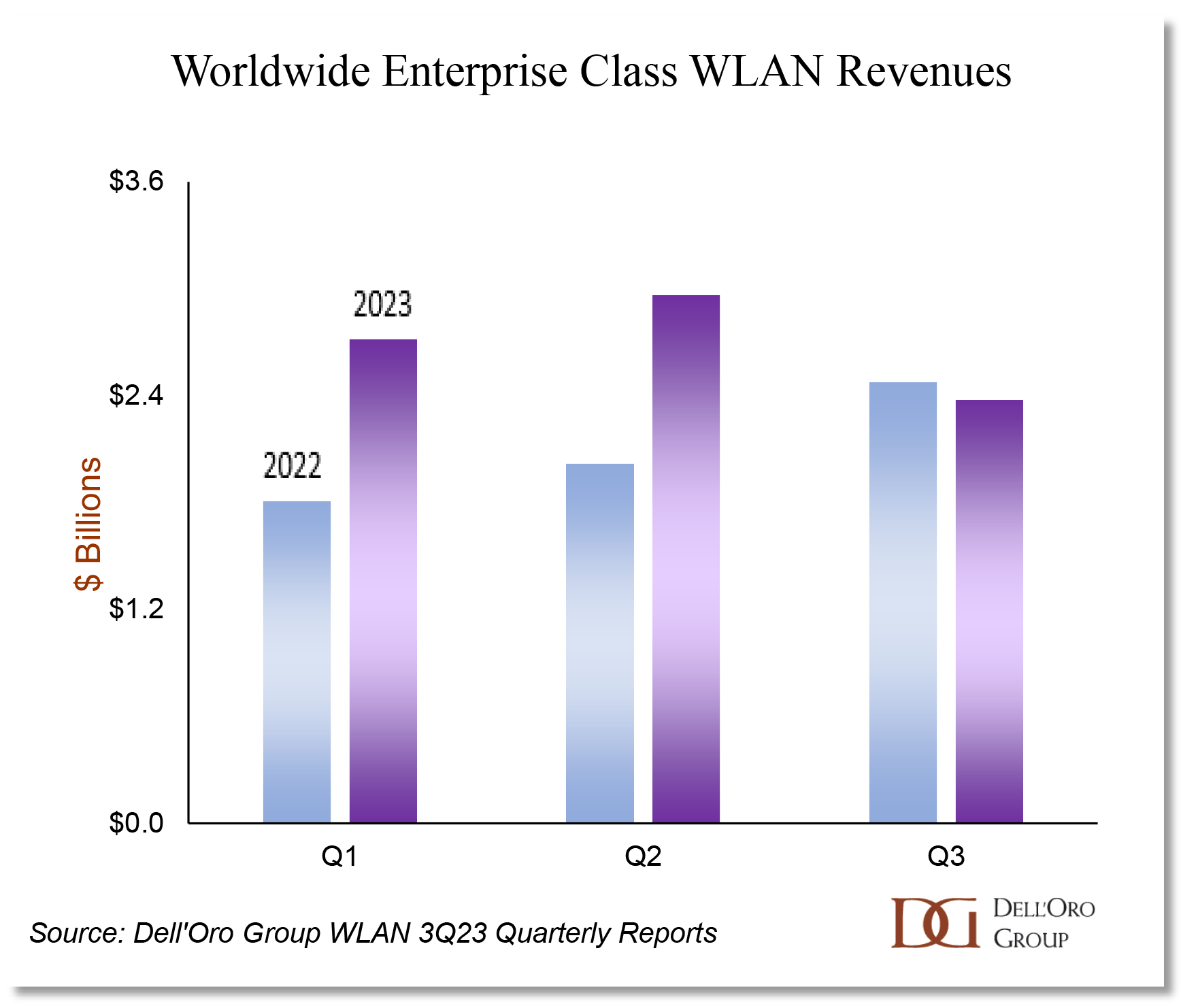

Early last year, we predicted that the enterprise class WLAN revenues would surpass $10 B in 2023 and that sales would be weighted to the first half of the year, defying the usual seasonal patterns. Although 4Q23 results have not yet been published, the first three quarters of the year indicate that 2023 is unfolding as we anticipated.

In the first half of 2023, manufacturers shipped more Access Points (AP) than any first half in history. In the aftermath of the pandemic, a lack of components had created pent-up demand, just as businesses wanted to adapt their networks to accommodate hybrid work models. With equipment in short supply, prices rose and were locked into orders awaiting fulfillment. Once the shortages were alleviated, unit shipments flooded into the channels and manufacturers recognized record revenues.

The good times showed signs of waning in 3Q23, as it became evident that the distribution channels were holding excess equipment, and enterprises needed time to deploy the high volumes of units that had shipped. This led to a drop in unit shipments from manufacturers, with the blow to revenues softened by growth in average prices.

The party may be over, at least temporarily, for the WLAN market; but scratching the surface, there were a couple of gems in 2023 that point to longer-term expansion.

First, use of the new 6 GHz band for Wi-Fi expanded. The spectrum was approved for unlicensed use in the US in 2020, but worldwide shipments of APs supporting the new band stayed below 3% until 2023. In 3Q23, Wi-Fi 6E shipments rose to 10% of units shipped, representing almost a quarter of worldwide revenues. Wi-Fi 6E shipments grew despite a lack of coordination by worldwide regulatory bodies regarding which portions, if any, of the 6 GHz band are allocated for unlicensed (Wi-Fi) use. Then, as the cherry on the 6 GHz sundae, Wi-Fi 7 APs became commercially available for enterprises in 2023. The new standard (also known as 802.11be) promises higher throughput and lower latencies and will operate in 6 GHz where available, but it will also work in the legacy frequency bands.

Second, AIOps and network automation moved to the forefront of IT decision making. Manufacturers introduced new AI-driven operations features for troubleshooting and recommending configuration changes. Startup Wi-Fi vendors marketed services based on fully automated network operations. Enterprises who deployed AIOps began reporting a dramatic reduction in network trouble tickets. In 2023, the automation of network operations became a paragon of AI’s value proposition to enterprises.

This context leads us to the following predictions for the WLAN market in 2024:

The WLAN digestion period will take hold and continue well into 2024

It will take several quarters for the excess WLAN equipment to clear itself from the distribution channels and enterprises’ inventories. In addition, some enterprises are concerned about the economic context and are elongating their decision-making. We project an overall contraction in WLAN revenues in 2024, especially given the record high sales that occurred in 2023.

Wi-Fi 6E adoption will begin to decline as the availability of Wi-Fi 7 expands

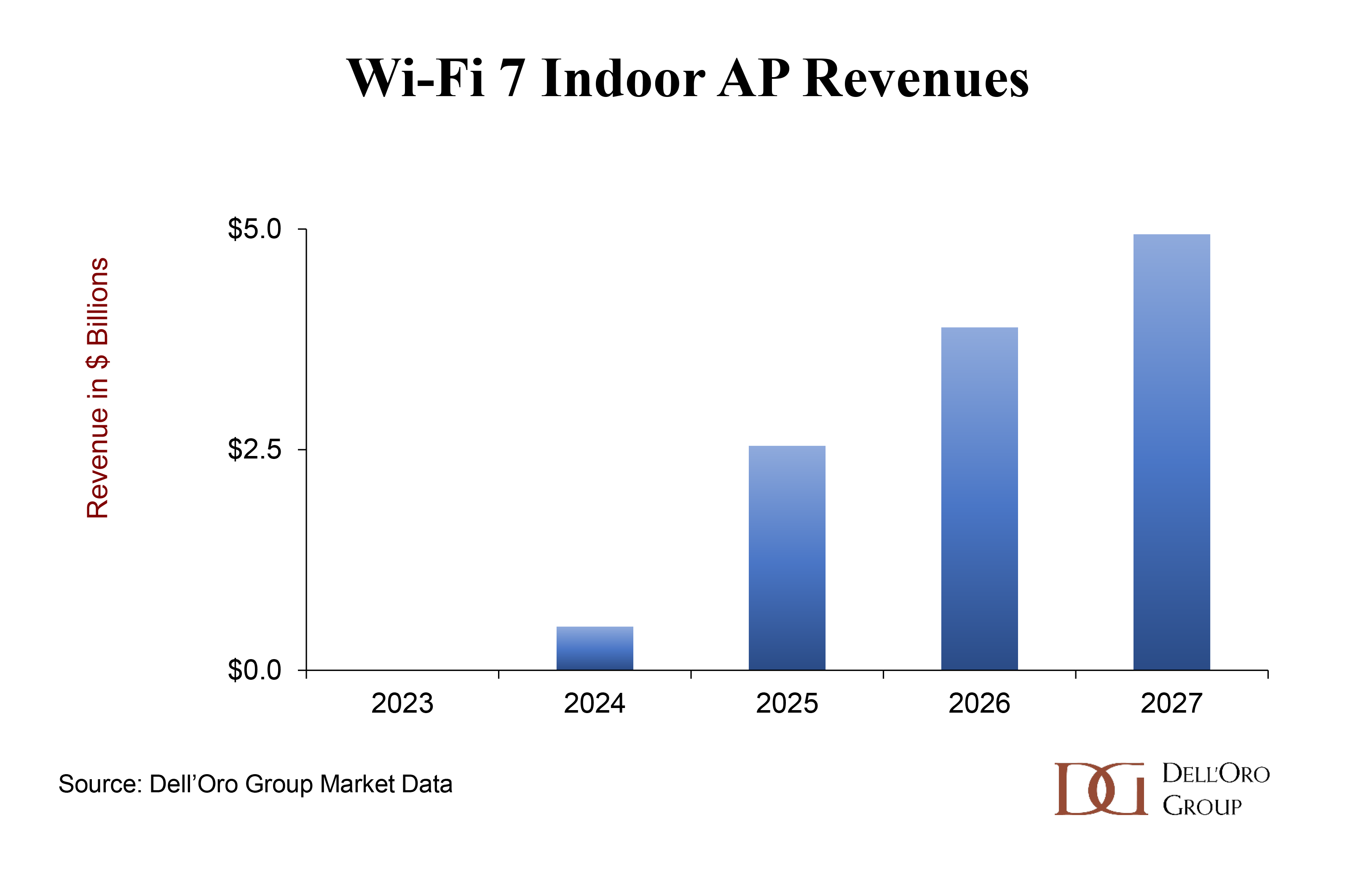

There are already 6 vendors selling Wi-Fi 7 APs to enterprises, and the rest of the major vendors are expected to introduce Wi-Fi 7 APs in 2024. Over the course of 2024, vendors will ship more Wi-Fi 6E than Wi-Fi 7 APs. However, 2024 will be the year that Wi-Fi 7 establishes a hold on the market. As a broader range of configurations becomes available, sales of Wi-Fi 7 will begin to displace sales of Wi-Fi 6E. Wi-Fi 7 adoption is expected to grow significantly over the next few years, representing 45% of the Indoor APs shipped in 2027.

Software revenues will dampen the effects of lower unit shipments

As WLAN management applications add features that enterprises value, enterprises are more likely to accept the associated recurring costs. The results from 3Q23 showed an early indication that the market is entering into a digestion period: unit shipments dropped by 14% year-over-year and AP revenues contracted by 10%. Meanwhile, Controller & Licenses revenue grew by over 20%. The recurring license fees paid by the installed base of users helped to grow this line item, even as unit shipments dropped. This phenomenon may soften the downturn, especially for the vendors who have managed to shift their customer base to a recurring model.

Campus NaaS will gain traction as enterprises focus their priorities

In last year’s predictions, we indicated that some clarity was needed to define Campus Network as a Service (Campus NaaS) offers – many manufacturers were using the term NaaS to mean different things. In our June 2023 report, we were able to broadly categorize the offers into three groups: Enabler, Turnkey, and Wi-Fi as a Utility. Since then, more vendors have begun to offer LAN equipment and software in cloud consumption model, and the offers have begun to appeal to a broader set of enterprise verticals. In 2024, the definition of Campus NaaS should become even crisper, and enterprises will begin to consider the service as a way to outsource their IT connectivity, allowing them to focus on their core business priorities.

Yesterday’s announcement of HPE’s plan to purchase Juniper Networks for approximately $14B rocked the networking world. Impacts on the switching and security aspects of the business have been covered in briefs by analysts Sameh Boujelbene and Mauricio Sanchez. As the overlap in portfolio seems especially important in Wireless LAN, here is my take from a WLAN perspective.

Market Size

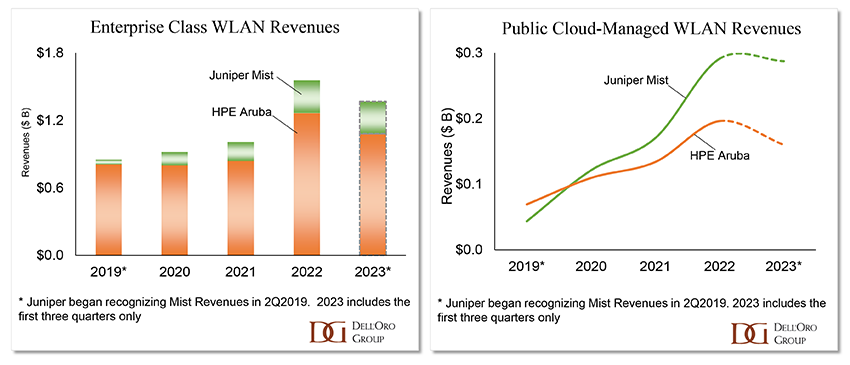

In the Enterprise Class WLAN market, HPE is the second largest by revenues. The company recognized $1.1 B for the first three quarters of 2023, giving it a 13% market share. This compares to Juniper’s WLAN revenues of $ 288 M (4% market share) for the same period. Combined, the two companies’ WLAN revenues are still well under half of Cisco’s, who is the market leader. However, this view belies the market potential.

Juniper Mist has been on a rocket ship trajectory over the past four years. The company has been displacing Cisco and HPE with Fortune 100 companies that are becoming more open to public cloud-managed WLAN, the only architecture that Juniper offers. In contrast, HPE Aruba has been underperforming in cloud-managed WLAN, with market share hovering around the 6% mark. Juniper’s revenues surpassed HPE’s public cloud-managed WLAN revenues in 2020. Mist WLAN grew 47% y/y for the first three quarters of 2023, compared to a 4% growth for Aruba public cloud-managed WLAN revenues in the same period.

Synergies

On the face of it, the two companies have WLAN solutions that compete head-to-head. However, each company has different strengths.

Whereas Juniper has been making waves with its AI-Ops network management engine, Aruba is known for its high-quality radio solutions. HPE took an early leadership position in the new 6 GHz band and shipped more Wi-Fi 6E APs in 2022 than any other vendor, more even than Cisco. The company also just won Wi-Fi Now’s Best Enterprise Wi-Fi solution for two of its 6E APs with a specialized design that maximizes use of the 6 GHz band.

Juniper’s Mist solution was developed by ex-Cisco executives who found the Cisco Meraki cloud too restrictive for their micro-services architecture. A cutting-edge software architecture has allowed Juniper to develop high-traction features, such as an AI-driven personal assistant, Marvis, to help operations staff with network decisions, and analysis of Zoom telemetry to improve videoconferencing quality.

Competitive Positioning

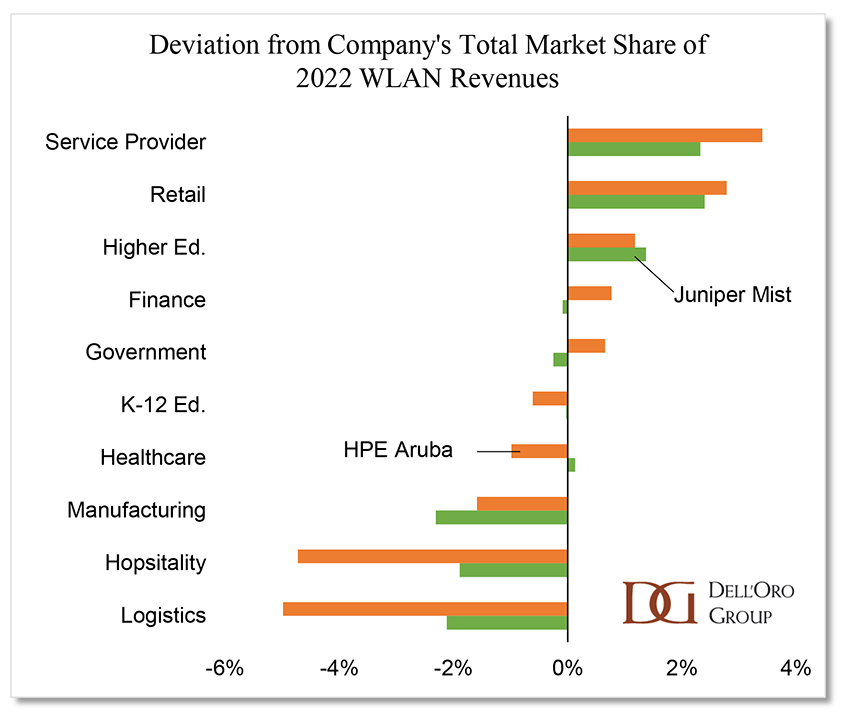

Antonio Neri, HPE’s CEO, has pointed to the complementarity of the two companies’ targeted market segments. An analysis of their 2022 WLAN market share by vertical indicates that Juniper and HPE have similar strengths in Service Provider, Retail, and Higher Education – in these segments, their market share is above their company’s overall share and future cannibalization of revenues in these segments seems inevitable. The analysis shows potential for HPE’s scale to boost Juniper’s WLAN performance in the Finance & Professional Services and Government segments. HPE’s GreenLake has obtained FedRAMP certification, which will boost government opportunities for Mist once the acquisition is complete.

The biggest upside for Juniper Mist sales will be in the geographic reach that HPE can provide. HPE provides access to a larger volume of channel partners, and Juniper underperforms in all macro regions outside North America.

What to watch for in the converged WLAN portfolio

Juniper’s impressive growth has been fueled by their AI-Ops solution, and HPE has the scale of Juniper executives’ dreams. However, pointing to complementary strengths in public cloud-managed WLAN (Juniper) and on-premises managed WLAN (HPE) is too simplistic. Today, the cloud is hybrid, and distributed enterprises want a campus networking solution that can work seamlessly whether it’s managed from the public cloud or on-premises.

Developing a coherence across the two architectures is a challenge that Cisco has been struggling with for the past year and a half. In mid-2022 they announced the intention to converge the Meraki and Catalyst platforms, but WLAN APs capable of operating under both management systems remain a small minority of their sales. Executives have told us that it is a long and complex endeavor to ensure that detailed networking parameters are represented and configured the same way from both Meraki and Catalyst management applications.

Once the HPE-Juniper deal closes, the first task for the combined company’s campus networking teams will be the migration of micro-services-based Mist into the GreenLake environment. Executives will have painful memories of the disruptive integration of Aruba Central into GreenLake in 2022. It will be crucial to maintain the same extensibility, the same high-frequency delivery of software updates, and the same large-volume data analysis that customers expect from Mist, at the risk of losing their customers’ goodwill.

However, the bigger technological challenge will be the development of a hybrid WLAN roadmap – involving seamless functionality across public cloud and on-premises managed WLAN equipment. Cisco and Extreme Networks already have a head start on that front.

Today, CommScope announced an enterprise-class, Wi-Fi 7 Access Point (AP), making the company the largest enterprise-class WLAN vendor outside China to announce an AP that supports the cutting-edge standard. When the R770 begins shipping in December it will take its place on the Wi-Fi 7 shelf with APs from H3C that are already shipping, from Huawei that have been delivered to over 50 customers, and from EnGenius that are expected to ship in November. HFCL has also promised several OpenWiFi Wi-Fi 7 APs, although none of them support the new 6 GHz band.

For some in the industry, these announcements seem early, since the standard underlying Wi-Fi 7, named 802.11be, is not expected to receive the IEEE’s official stamp of approval until 2024. The Wi-Fi Alliance has not announced a timeline for its AP certification process, either.

This fact did not stop today’s announcement by CommScope, who released details of the new AP which is based on a Qualcomm chipset. CommScope Ruckus representatives confirmed to us that the company will begin selling the R770 before it has been certified and begin certification as soon as the process is available.

Now that the new Wi-Fi standard is a reality, it is legitimate to ask the question: What value are enterprises really going to get from upgrading to Wi-Fi 7?

This time around, the IEEE has spun its magic to obtain much higher speeds than previous generations of WLAN technology. 802.11be was labeled “Extremely High Throughput” and, in theory, brings 5 times more throughput compared to 802.11ax, which was commercialized as both Wi-Fi 6 and Wi-Fi 6E. Speed improvements have been made possible by the introduction of a higher order modulation scheme and wider channels, among other innovations.

In reality, throughput speeds will not match the theoretical maximums and will depend on several variables. The maximum data transfer rates of the newly announced Wi-Fi 7 APs are two to four times the rates of similar Wi-Fi 6 products, which gives enterprises an idea of the improvements they can realistically target.

The ability to improve data rates will be a boon for enterprises who are experiencing Wi-Fi congestion as their employees return to the office, relying heavily on videoconferencing applications. But Wi-Fi 7 will bring more than just higher bandwidth. Evolved security, lower latency and enhanced power efficiency could also push an enterprise to upgrade its Wi-Fi network.

One of the headline features of 802.11be, called MLO or Multi-Link Operations, has been the subject of several academic papers. Tests have demonstrated that the ability to communicate over multiple radio interfaces (for example by switching rapidly between bands) lowers latency and increases reliability. CommScope has jumped on this advancement. The R770 supports MLO across all three frequency bands: the legacy 2.4 GHz and 5 GHz bands as well as the freshly minted 6 GHz. However, it is important to consider that MLO needs to be supported on both the AP and the end device.

On the device side, several smartphone manufacturers have announced Wi-Fi 7 in their line-up, and some of them explicitly call out MLO. Xaiomi was early to the Wi-Fi 7 market with the M13 Pro and other manufacturers have followed suit, with the most recent announcement from Google, adding the Pixel 8 and Pixel 8 Pro to the Wi-Fi 7 device list.

Source: GSMArena.com

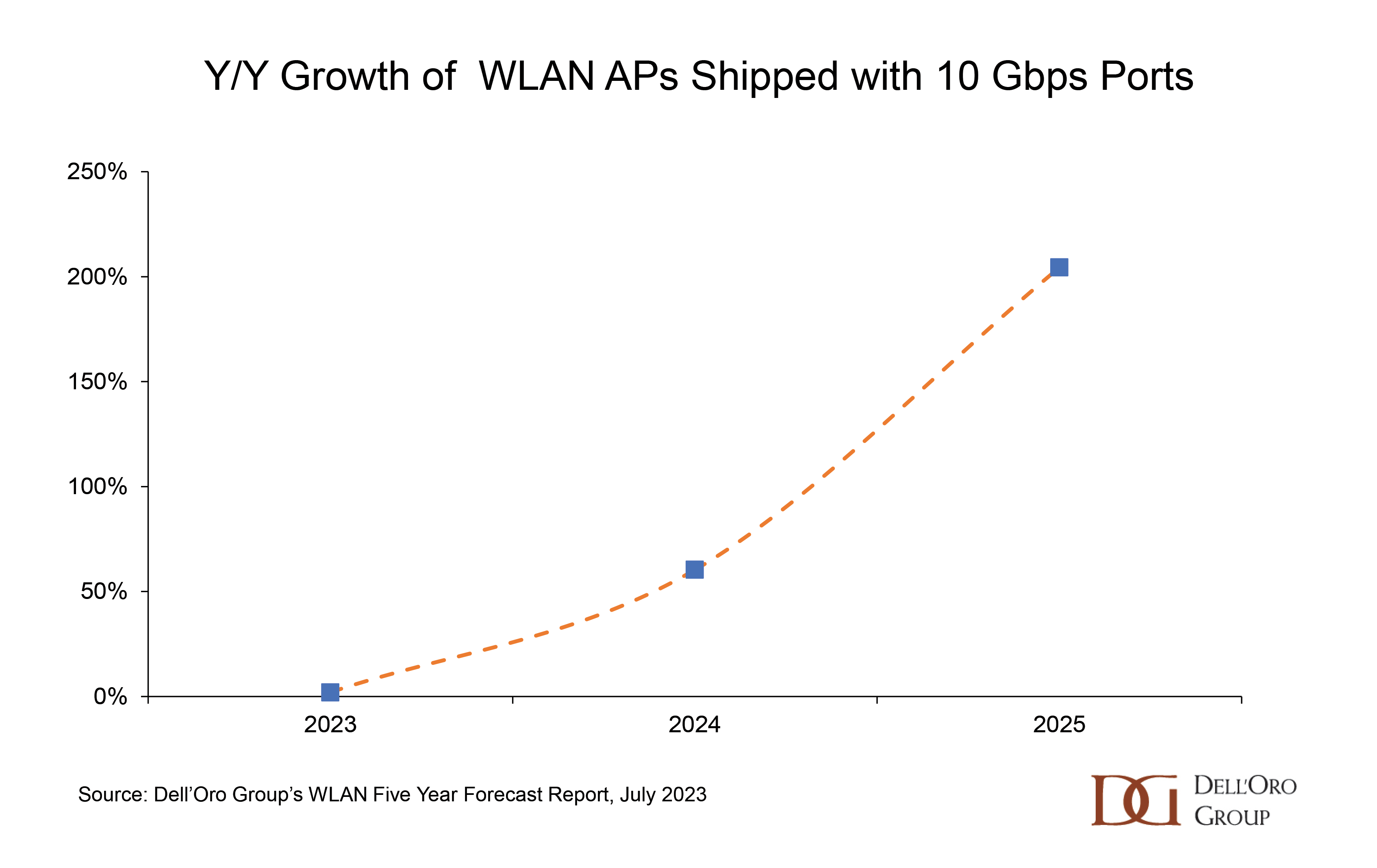

As enterprises upgrade their Wi-Fi networks to the latest generation, they will need to think about more than acquiring new APs. The availability of switch ports and the cabling infrastructure is of particular importance, as all of the Wi-Fi 7 APs introduced to the market so far have a 10 Gbps port to connect the AP to the switch. This will be a fundamental change for many organizations, whose APs currently have uplinks that range between 1 and 5 Gbps. Many enterprises will need to upgrade cabling infrastructure to Cat 6A and may find the distance limitation of 100 meters (328 feet) problematic. Huawei’s AirEngine 8771-X1T also has a fiber 10 Gbps port, opening the possibility for enterprises to lay optical cable or a combined fiber-electrical cable.

The value of Wi-Fi 7 is in the higher order modulation and in the MLO, but most of all in the access to the new 6 GHz frequency band. Enterprises that operate in regions of the world whose regulators have freed up the whole 6 GHz band – such as North America, Brazil, and Saudi Arabia, have the most to gain. Enterprises in countries where unlicensed use of the 6 GHz band is not permitted, such as China and India, will benefit from incremental improvements without the lower congestion and larger channel widths introduced with the new frequency.

Sales of Wi-Fi 7 APs are expected to remain relatively small in 2023 and will begin to become material next year – a year that may be difficult for some Wireless LAN manufacturers. After living through two years of component shortages and ballooning backorders, manufacturers have released a huge wave of enterprise-class WLAN APs in the past three quarters. We expect 2024 will be a digestion period, a pause while enterprises deploy their equipment and distributors clear the excess inventory from the channel. If this scenario plays out as we expect, Wi-Fi 7 sales may be the bright spot of the year, enticing enterprises to refresh old networks with higher-priced, cutting-edge equipment.

While the vendors are gearing up for new sales, the industry as a whole is busy developing new use cases for the Extremely High Throughput Wi-Fi. The Wireless Broadband Alliance (WBA) and its partners have documented their vision that by supporting higher speeds, lower latency, and higher density deployments, Wi-Fi 7 will play a pivotal role in the Enterprise Metaverse and Industrial IoT. The industry organization is also actively collaborating with its members to conduct field trials of these technologies in real-life Wi-Fi 7 networks.

A recent discussion with Bruno Thomas, CTO of the WBA, served to emphasize the innovation that the new protocol will bring to the market. “Wi-Fi 7 will enable enterprise use cases that have been impractical or impossible with other wired of wireless technologies. It will drive innovation…in vertical sectors like healthcare for telemedicine, and within industrial settings for machine-to-machine communication, remote monitoring and predictive maintenance.” In other words, we are on the doorstep of a critical intersection. Technological advances have combined with a brand-new frequency band, and enterprise connectivity has leapt into the future.

Enterprise Class WLAN sales increased by 47% Y/Y in the first half of 2023. With this meteoric acceleration in manufacturer revenues as a backdrop, industry luminaries gathered in Toronto this week at the Wi-Fi World Congress North America. Wi-Fi NOW’s CEO, Claus Hetting, hosted and facilitated the conference, peppering the speakers with questions that highlighted the innovation and thought leadership in the room. Chetan Hebbalae, formerly at Meta on TIP’s OpenWiFiproject, and now VP of Products at Kyrio, summarized the essence of the event by quoting science fiction writer Arthur C Clarke: “Any sufficiently advanced technology is indistinguishable from magic.”

Advanced technology was on full display as Akoustis showed off the company’s ultra-wide bandwidth RF filters, used in HPE’s 655 access point (AP). Dave Aichele, VP of Business Development, explained that Akoustis’s mastery of material science allowed the Wi-Fi 6E AP to make full use of the new 6 GHz band, one of the few APs on the market to do so. Qorvo referenced the increased power consumption of triband APs, pointing to the power conservation of their Front End Module (FEM), and the increased competition in the FEM market keeping them on their toes.

At their booth, VVDN Technologies displayed a Wi-Fi 7 AP produced from their cutting-edge reference design. The enterprise market is seeing early product announcements in the new 802.11be (Wi-Fi 7) protocol, with H3C already selling a flagship product in China and EnGenius promising an AP in November.

Malcolm Smith of Cisco’s CTO Advisor group described how TSN (Time Sensitive Networking) with scheduling in Wi-Fi 6 and 7 could lead to bounded latency for applications such as VR. Hyper directional antennas were evangelized by Bill Anderson, AmpThink’s founder, as a game changer in stadium deployments, allowing installations at a quarter of the cost of under-seat APs. Bart Giordano, President of Ruckus at CommScope focused on the technology that has been front of mind for IT leaders since the advent of Chat GPT; explaining that the drastic reduction in the cost to train AI models will revolutionize not just enterprise WLAN, but all jobs in all domains.

The advanced science turned to the magic that Arthur C. Clarke predicted, as speakers and panelists shifted to discuss use cases and end-user experience. Elizabeth Parks, President of Parks Associates, kicked off the second day of the conference by promising that the 4th industrial revolution would be all about services and pointing to the enormous Wi-Fi opportunity in the MDU market. Only between 1 and 2% of MDU homes have access to a managed Wi-Fi service. Robert Grosz, President of WorldVue, urged conference attendees to focus on the needs of MDU property owners by emphasizing Wi-Fi as a capital asset with revenue potential, instead of just an expense.

There were plenty of other Wi-Fi use cases discussed, both practical and entertaining.

Bahador Amiri, Senior Director of Wireless Engineering at Cisco, explained that a combination of different location technologies: GPS, Wi-Fi FTM (Fine Timing Measurement or 802.11mc), and 802.11az, among others, enables asset tracking, indoor navigation, and smart workspaces. He then took the audience on a cruise ship journey, with room doors that unlocked automatically, guests that were prevented from enjoying the amenities until they had watched the safety video, and a drinks service that delivered your order wherever you were on the ship – with all of these use cases relying on Wi-Fi location services.

Keeping the focus on user experience, Michael Penney, SVP of Engineering at American Bandwidth, promised to turn Wi-Fi APs into mini cell towers, using Passpoint and OpenRoaming to transparently move end users between cell and Wi-Fi service – solving the problems related to poor cell coverage indoors.

Amidst the speakers’ presentations and panels, some contentious questions were addressed, answered, or debated during the conference.

Will Campus Network As A Service expand Wi-Fi’s addressable market? There was a divergence of opinion on whether Campus NaaS was an innovative architecture or a new business model. Bob Friday, CTO and Co-Founder of Juniper’s Mist, pointed to the foundational role that AI operations played in automating Wi-Fi management. Nile’s impressive demo underlined the service’s potential. Dell’Oro Group has quantified the size of this market and its accretive potential in an Advanced Research Report entitled Campus NaaS and Public Cloud Managed LAN.

Will private 5G take market share from Wi-Fi? AmpThink’s Bill Anderson presented a fascinating analysis of two stadium deployments, one with Wi-Fi and one with cellular technology. The Wi-Fi installation was 105 times less expensive than the private cellular deployment, dropping the price per Tb from $3.9 M to $0.192 M. With its Zero Effort Networking (ZEN), American Bandwidth’s Michael Penney decried the onus of having to prove to a carrier that indoor coverage is bad, with a call to focus on user experience instead. Says Penney: indoors, Wi-Fi is the clear winner.

Is there an advantage to disaggregating Wi-Fi? OpenWiFi was front and center in a panel discussion with representatives from several companies, along with the Telecom Infra Project (TIP), demonstrating the breadth of the ecosystem. Tony Stramandinoli, VP of sales at Edgecore, explained that his company’s focus on AP hardware, and using OpenWiFi software, has enabled faster innovation. Robert Grosz of WorldVue, who deploys networks with Ruckus, Aruba, Meraki, and Cambium, has also deployed OpenWiFi solutions. He explained that after a family moves out of an apartment in an MDU, the cleaning crew can rip out or paint over the AP accidentally. For this use case, disaggregating the hardware from the software is most beneficial! Opening up the interface between the controller and the AP enables redundancy of hardware suppliers. C3Spectra and NetExperience are two companies that offer OpenWiFi compliant controllers. An SDK interface encourages innovation at the application level, highlighted by GoZone and Spectra who develop compatible application suites. Bernard Herscovici, CEO of NetExperience, referenced Purchase Orders for 5 Million Open Wi-Fi APs.

The buzz of the Wi-Fi Now Toronto event was palpable. During an evening of fancy cocktails, attendees lined up to get a signed copy of Greg Ennis’s book, Beyond Everywhere: How Wi-Fi Became the World’s Most Beloved Technology. Bart Giordano highlighted the depth of experience in attendance as he quipped that despite being around since 802.11g, he didn’t even merit a footnote in Greg’s book. With a Wi-Fi ecosystem this deep and broad, it’s no wonder it can spin science into magic.

Since 2020, a change in network usage patterns has imposed new requirements on IT infrastructure. Enterprises, educational institutions, and governments have experienced a seismic shift in the way they operate. Some organizations now have an entirely remote workforce. Other businesses have hybrid models, with a variety of work-from-home and work-in-the-office permutations. Even companies with exclusively on-site employees have enabled new video applications. Videoconferencing improves employee efficiency but also swamps the network with traffic, exposing network performance problems.

Defining the Future of Campus Networks

Amidst these profound changes in work patterns, enterprises are renewing their strategic IT plans. Companies must ensure that investments in their communications infrastructure support their current work patterns–but also that they are on a path to meet their future needs. Luckily, while enterprises are focusing on understanding today’s requirements, IEEE committees are playing a foundational role in developing IT standards for the future.

The IEEE 802 standards committee is responsible for the evolution of local, metropolitan, and other area networks. They tend to work with the two lower layers of the OSI reference model (the Data Link and Physical layers) and refer to the IETF’s work to define the upper layers.

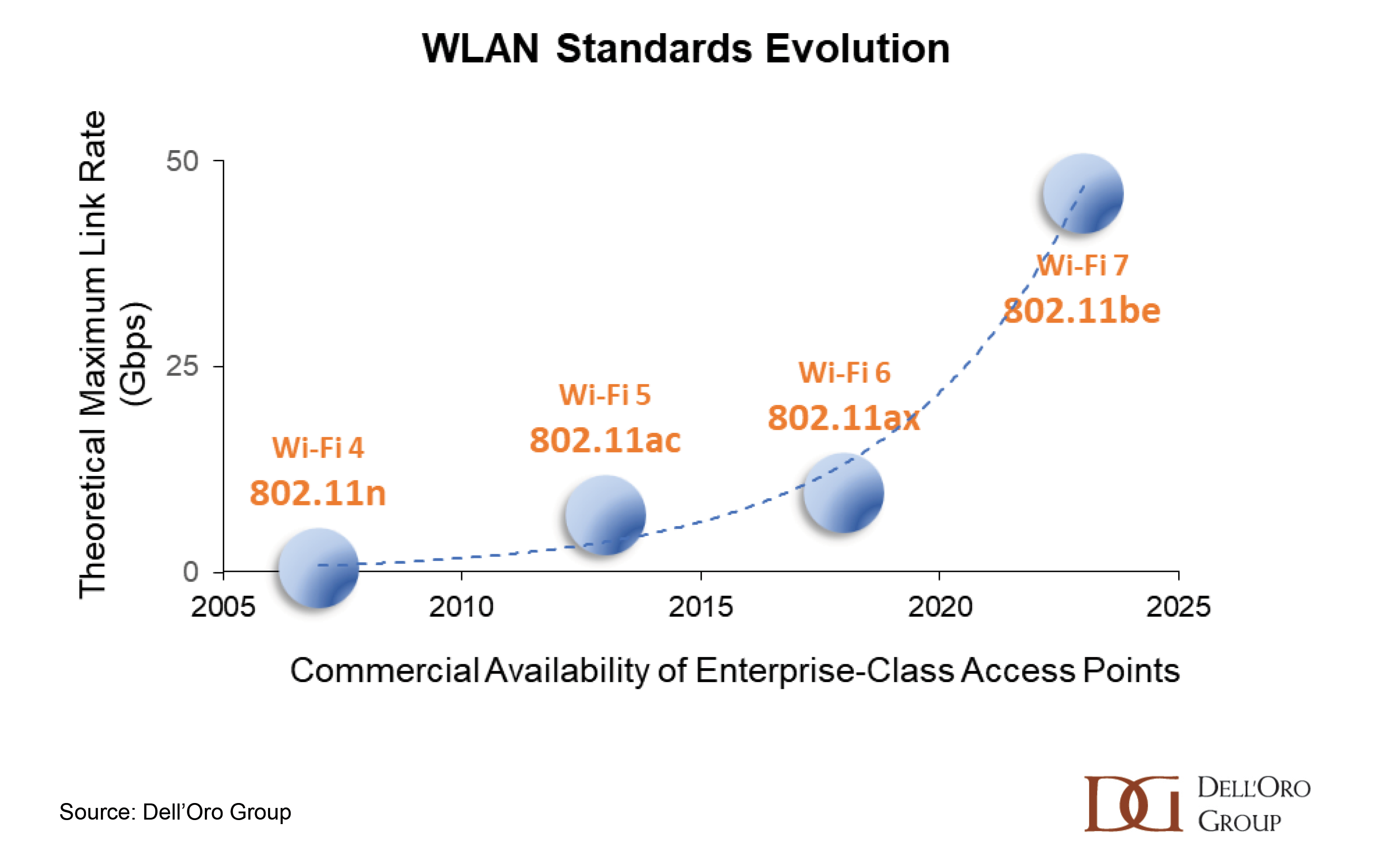

For example, the evolution of Wireless LAN protocols, as defined by the 802.11 WLAN working group, has been addressing organizations’ hunger for more wireless bandwidth in campus networks. With each successive 802.11 version, enhancements to modulation and coding schemes have increased spectral efficiency and lowered interference. Each WLAN standard has increased its maximum theoretical link rate, with Wi-Fi 7’s maximum rate over 75 times that of Wi-Fi 4, shown below.

However, the IEEE 802.11 organization focuses on more than increasing throughput. Made up of a multitude of discussion groups, study groups and more formal work groups, the IEEE is working to improve IoT (Internet of Things) functions, reliability, latency, power consumption and security of the LAN. All of these new capabilities should be considered by enterprises that are committed to transforming their networks.

Organizations Begin Their Network Transformations

To meet the dramatic shift in employee work behaviors, companies are rethinking the optimal use of office space. In its 2022 Occupancy Benchmarking Program, the CBRE (a global leader in commercial real estate services and investments), found that 87% of commercial real estate occupiers surveyed from across the world wanted to optimize their real estate portfolios. In the survey, real estate occupiers identified the need to invest in technology that integrated physical and virtual work experience.

Many different enterprise verticals are investing in IT infrastructure to meet new requirements. For instance:

Multinational banks with high volumes of video conference traffic.

Municipal Governments with wireless-first, smart city roadmaps.

Real estate owners and operators providing high-end WLAN coverage to their tenants in dense urban environments.

Universities transitioning to a Wi-Fi-only model for their students and staff and preparing for immersive learning by means of AR/VR applications.

Manufacturers interested in integrating WLAN in their operations, requiring low-latency and deterministic connectivity.

Retail operations revolutionizing processes such as self-checkout, inventory management and product labelling.

From our discussions with systems integrators, manufacturers, service providers and enterprises, we have identified five key trends that will reshape the enterprise LAN over the next three to five years.

1. A Wi-Fi First strategy

Prior to 2020, many IT departments worked with a standard metric of “number of Ethernet ports per desk”. For companies with employees working from home or in a hybrid model, this metric is no longer valid.

Wi-Fi first implies the deployment of low-density Access Points (APs) to provide connectivity in areas where there had previously been Ethernet ports, such as dorm rooms or low-density cubicles. Wi-Fi first can also involve covering common areas with high-density, high-performance APs to accommodate surges in traffic, such as in conference rooms or stadiums. Finally, a Wi-Fi first strategy often involves providing WLAN signals in new areas that had never had connectivity before; for example, urban centers, company patios, or school gymnasiums.

In addition to ensuring that the WLAN is delivering high bandwidth with low interference, an enterprise must ensure that the network backbone can support the traffic. Organizations’ strategic IT plans must include a provision for the growing bandwidth of WLAN uplink ports.

Most enterprise APs shipped today are equipped with a 1 Gbps port. However, APs supporting the latest standards are capable of higher data transfer rates; they can support 2.5 Gbps, 5 Gbps or even 10 Gbps interfaces. As Wi-Fi 7 is adopted in the market, we expect 10 Gbps ports to grow considerably, allowing higher bandwidth applications to operate in the LAN.

2. A Smarter Network Means Efficiency and Automation

With new demands on the network, organizations need a better understanding of how their facilities are being used. A wide range of applications and services are available to provide insights into meeting room occupancy, environmental readings, and the location of assets.

To enable these insights, enterprises are integrating more and more “things”, instead of just “people”, onto their LANs. The IoT can involve wired devices, such as security cameras and monitors for video conference rooms. The IoT can also rely on wireless devices, such as occupancy sensors, electronic labels, or environmental sensors.

Some devices, such as video cameras or VR headsets, can increase LAN traffic considerably. However, organizations also need to consider the growing need for Power over Ethernet (PoE) ports on their campus switches. These ports are required to deliver more power to high performance APs, as well as to devices such as cameras. We expect that the percentage of switch ports that support PoE will continue to rise as the demand for high-end devices grows.

In addition to feeding applications with data to improve enterprise efficiency, the next generation of campus technology allows for the automation of network management. AI-Ops refers to features that use advanced analytics to simplify network operations, helping to filter alarms, predict network performance issues, or even automatically suggest and apply fixes to network problems.

The head of IT of one organization with which we spoke was amazed that activating AI-Ops features in the campus LAN uncovered existing network configuration problems that were previously undetected; these problems had been affecting quality of service for years. In addition to improving the user experience, AI-Ops reduced the number of trouble tickets by 95%.

3. Emphasis on Sustainability

Enterprises concerned with the environment are analyzing every step in their value chains to eliminate waste, decrease dependence on non-renewable resources, and reduce power consumption.

Initiatives that environmentally conscious enterprises are taking in their LANs include:

Configuring Energy Efficient Ethernet (EEE) on switch ports, which moves ports to a low-power state when they are not carrying traffic.

Replacing high-capacity copper cable with fiber. Fiber-optic Ethernet cables can support 10 Gbps and higher, and they can withstand longer distances with lower losses.

Flattening the network hierarchy and reducing the number of switches in the network.

Purchasing equipment made of recycled materials and packaged in a sustainable manner.

Moving to commercial models (such as Campus Network as a Service) that incorporate the re-purposing of old IT equipment when it is replaced.

4. Low-Latency Communications

WLAN revenues generated from sales to manufacturing companies grew by more than $500 Million in 2022, an increase that exceeds the growth in any other vertical that we track. Industries that adopt wireless infrastructure for their industrial processes often need low-latency, deterministic communications.

In November 2018, the IEEE 802.11 Real Time Applications Topic Interest Group (RTA-TIG) published a report outlining the usage model and technical requirements of an array of real-time applications. The report cites a wide range of applications for industrial systems. Applications categorized as “Class B”̶ including AR/VR and remote Human-Machine Interaction ̶ had a latency bound requirement of between 10 and 1 ms, with “latency bound” defined as the worst-case one-way latency measured at the application layer.

Other verticals, apart from manufacturing, will also require low-latency capabilities. For instance, VR or AR applications relying on interactive video are relevant to logistics, education, and retail verticals.

As low-latency applications become more common, deploying Wi-Fi 7 will be an important initiative for enterprises. A study at Virginia Tech showed that Wi-Fi 7, with its inclusion of Multi Link Operations (MLO), lowers the latency of communications by allowing devices to operate in multiple bands simultaneously. Enterprises can also benefit from Wi-Fi 7’s ability to support a diversity of channel widths. By means of the judicious assignment of certain channels to latency-sensitive applications, enterprises will be able to lower the latency for the users who are most sensitive to this parameter.

In addition to upgrading to Wi-Fi 7, enterprises may further lower latency by investing in local computing infrastructure to avoid processing data from latency-sensitive applications in the cloud.

5. A Network That Prioritizes Experience

In its spring 2023 survey of office occupiers, CBRE determined that the average utilization rate of office space in Asia Pacific was 65% and, in North American and Europe, was below 60%. These low office utilization rates are the main reason that the quantity of video traffic on the LAN has exploded. Employees now take videoconferencing capabilities for granted, in their daily interactions with colleagues and with their customers.

The reliance on videoconference puts the spotlight on the network performance. A user of a popular videoconference application can require up to 3.3 Mbps of bandwidth for a meeting with 6 participants and content sharing. As the number of concurrent videoconferences grows, the bandwidth expands accordingly, and network congestion becomes apparent, impeding employees’ ability to communicate effectively. Now that doing business deals over videoconference is a regular occurrence, a dip in video quality can affect a company’s revenues.

To ensure that employees can rely on high-quality videoconferencing, enterprises are adding capacity to their networks, but they are also taking other approaches. IT departments are collecting data from end-user devices, videoconference applications, and the network operations platforms, and using Machine Learning to identify the source of network problems as well as for resolution suggestions. Networking equipment schedulers can also be enhanced to optimize video streams or to improve the performance for certain groups of users, for specific applications, or for special events. Enhancements to support the high bandwidth of today’s video applications will lay the groundwork for the next generation of applications using very high resolution and volumetric video.

Campus Networks Must be Ready to Support Future Applications

An organization’s strategic IT plan will cover the five themes discussed above to varying degrees, depending on the different use cases and priorities. The need to increase bandwidth will be a common element of all the plans.

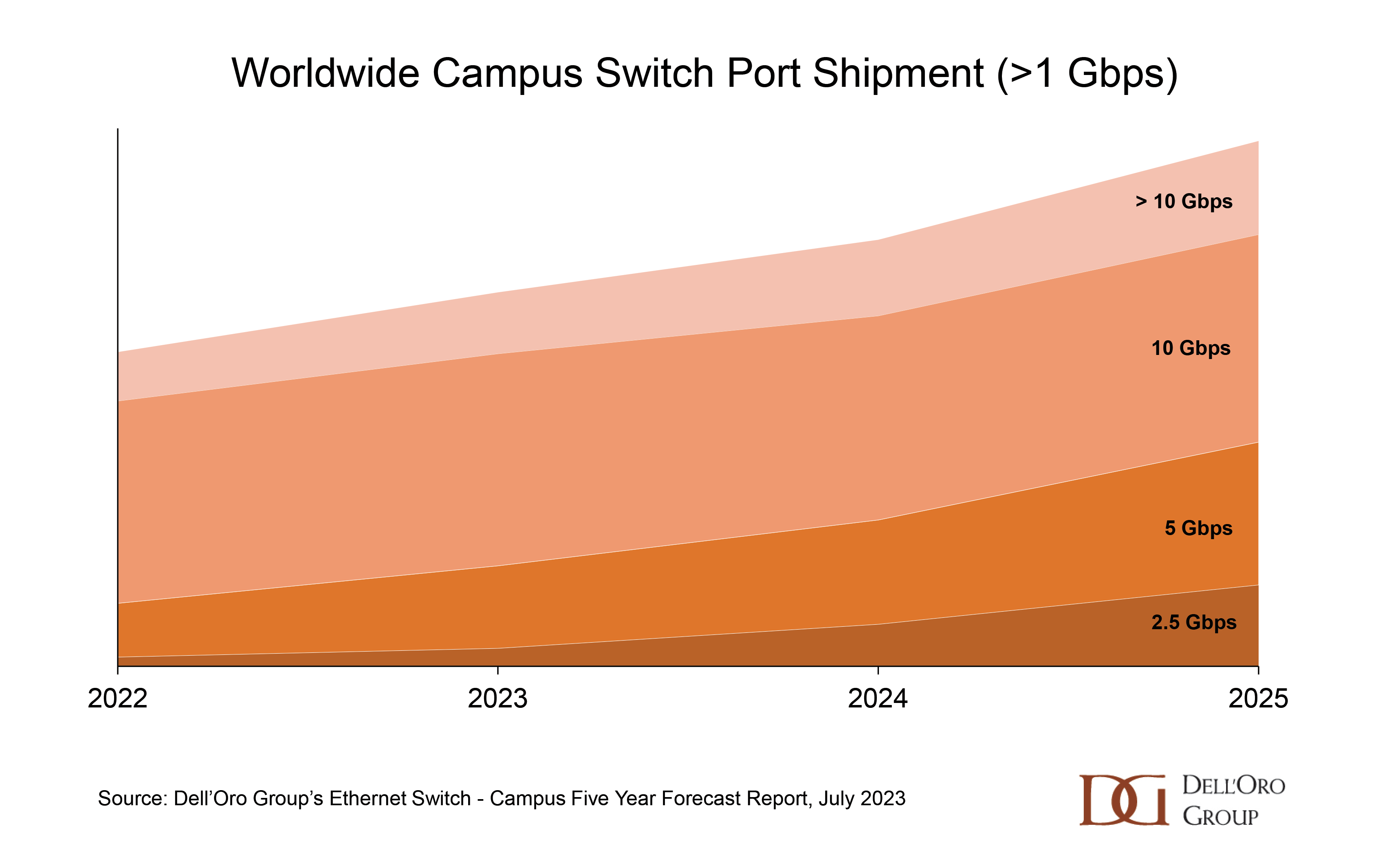

Although 1 Gbps ports will remain the speed of the majority of campus switch ports shipped over the next few years, we predict the growth of higher-speed ports in the LAN. This push to higher capacity links, shown below, will be driven by the need to connect branch offices at high speeds, by the elevated traffic generated by campus applications, and by the deployment of Wi-Fi 7 APs.

To build an IT strategic plan that will stand the test of time, enterprises must consider that their network traffic patterns will evolve along will their mode of work operations, whether it be mainly work-from-home, hybrid, or fully on-premises. The IEEE has laid a foundation of next generation campus IT functionality to meet the objectives of an organization’s IT plan, such as providing higher visibility into the usage of resources, improving the efficiency of workers, and increasing the sustainability of operations. Underlying all requirements is the need for greater bandwidth to the branch, in the LAN, and directly to end users. By moving to 10 Gbps in the campus, enterprises are taking an important step in readying their network for the future.