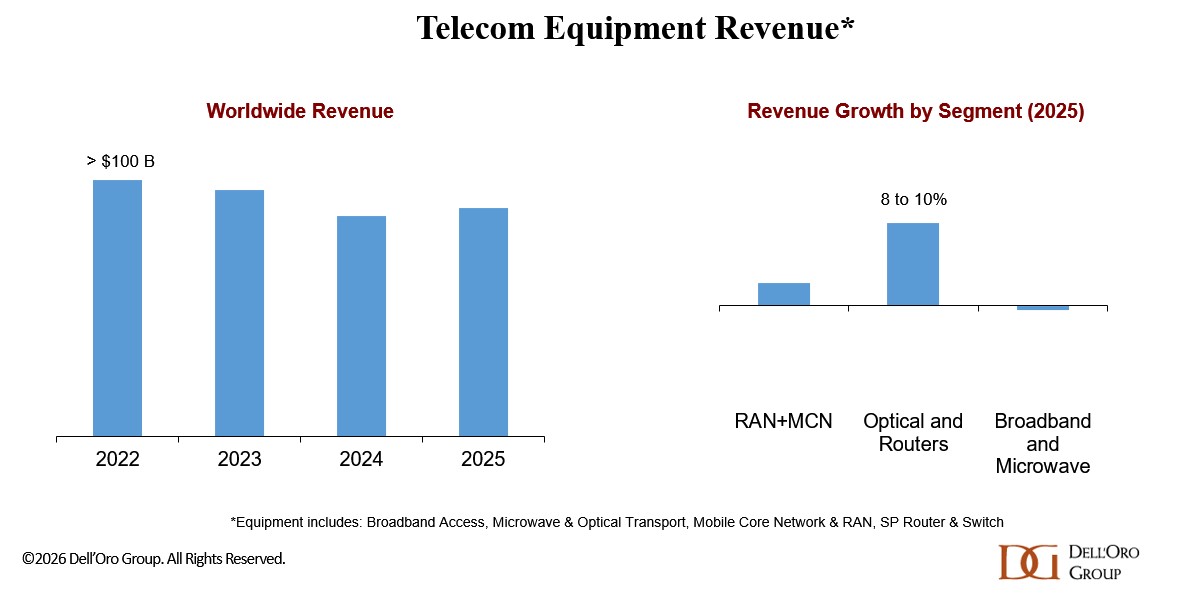

Following the 14% revenue decline between 2022 and 2024, telecom equipment investment conditions improved in 2025. Preliminary findings indicate that aggregate worldwide telecom equipment revenues across the six programs tracked by Dell’Oro Group—Broadband Access, Microwave & Optical Transport, Mobile Core Network (MCN), Radio Access Network (RAN), and Service Provider Router & Switch—increased 4% year over year (Y/Y) in 2025, supported by an exceptionally strong fourth quarter (accounting for 29% of full-year revenue).

Improved market conditions were supported by easier year-over-year comparisons, inventory stabilization, favorable currency movements, healthy demand for both wireless and wireline equipment, and robust investment from cloud providers, which contributed meaningfully to the overall growth of the telecom equipment market.

From a regional perspective, double-digit growth in North America and EMEA (Europe plus the Middle East and Africa) more than offset the more challenging conditions in the Asia Pacific. North America and China together accounted for slightly more than half of the overall market in 2025.

While growth was supported by both wireless and wireline segments, Optical Transport and SP Router & Switch stood out, partly reflecting their exposure to data center infrastructure investments.

Relative to our expectations heading into 2025, market performance was slightly stronger than the flat outlook initially outlined, supported by better-than-expected growth in MCN, Optical Transport, and SP Routers. Per the MCN report, the 5G MCN market reached an inflection point in 2025.

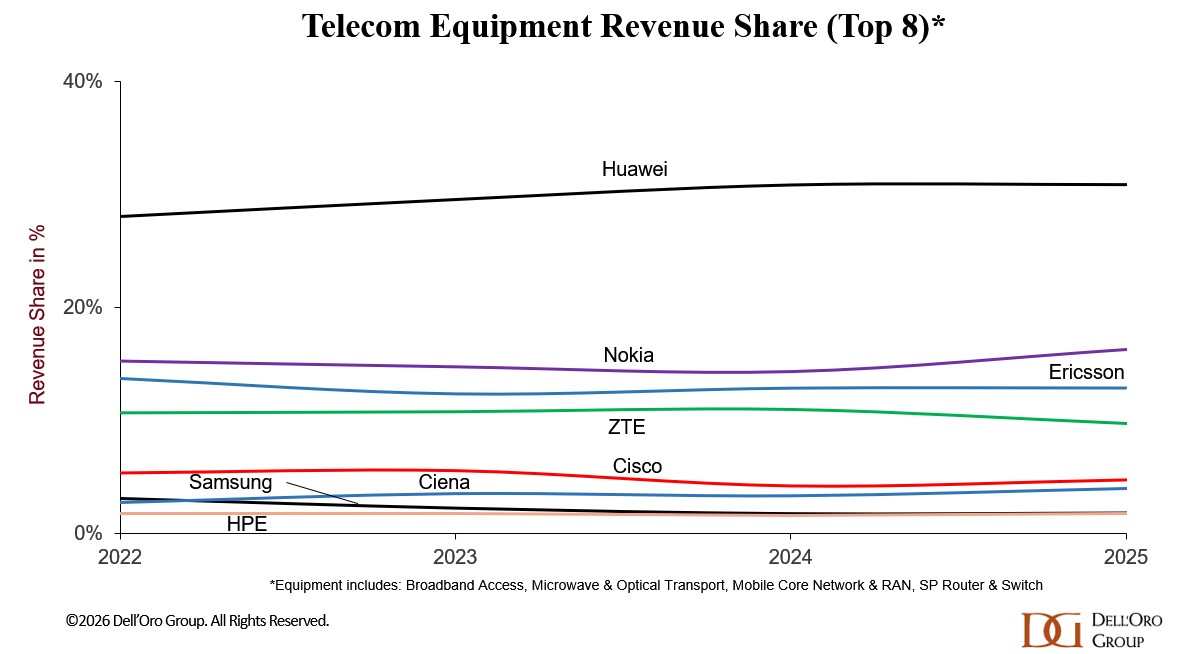

Global supplier rankings remained largely unchanged, although revenue shares shifted modestly. Nokia gained share, while Huawei and Ericsson remained broadly stable. Nokia’s share gains were partly driven by its acquisition of Infinera.

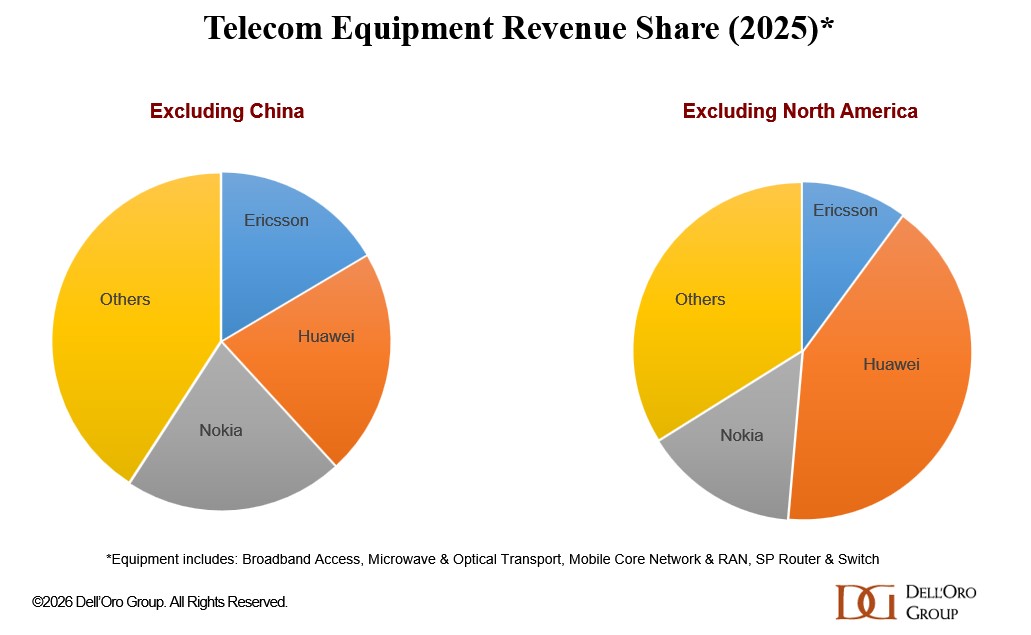

Regional dynamics vary significantly. Excluding China, the revenue distribution among the top three suppliers is more balanced. In contrast, excluding North America, Huawei’s overall revenue share reached a new high of 41% in 2025.

We attribute Huawei’s strong performance in markets where it is permitted to compete to three key factors:

- First, a comprehensive telco strategy, with Huawei ranking as the #1 supplier by revenue across all six telco programs.

- Second, technology leadership, supported by R&D investments that continue to exceed those of its competitors.

- Third, footprint expansion, as Huawei has adapted to geopolitical constraints limiting its total TAM by focusing on share gains in markets where it can operate.

Looking ahead, the analyst team expects the positive momentum to extend into 2026. Global telecom equipment revenue across the six programs is projected to grow 2% to 4% in 2026, though the outlook for wireless infrastructure remains more muted.