What Market Share Says About Börje Ekholm’s Legacy

Leadership transitions often invite instant verdicts. But as the Wallenberg family noted during Ericsson’s previous leadership transition, turnarounds in the telecom space are measured in decades rather than quarters. As Ericsson enters a new chapter, it is still too early to fully assess the long-term impact of Börje Ekholm’s strategic decisions. What we can evaluate today, however, is how Ericsson’s competitive position in the telecom equipment and Radio Access Network (RAN) markets evolved during his tenure.

Market share is not a perfect measure of success. It says little about profitability, shareholder returns, or the quality of strategic investments. Still, it remains one of the clearest indicators of whether customers continued to choose Ericsson in an intensely competitive market.

From Decline to Stability

When Ekholm became CEO in early 2017, Ericsson was emerging from a challenging period. The company had experienced deteriorating profitability, multiple restructuring programs, and significant losses in its RAN revenue share.

We estimate that Ericsson lost approximately 10 percentage points (PPs) of global RAN revenue share between 2011 and 2016, in part due to an intensified competitive landscape. Reversing that trend would not be trivial.

While Ericsson did not dramatically increase its global market position over the next decade, it largely succeeded in reversing the negative momentum that characterized the years leading up to 2017.

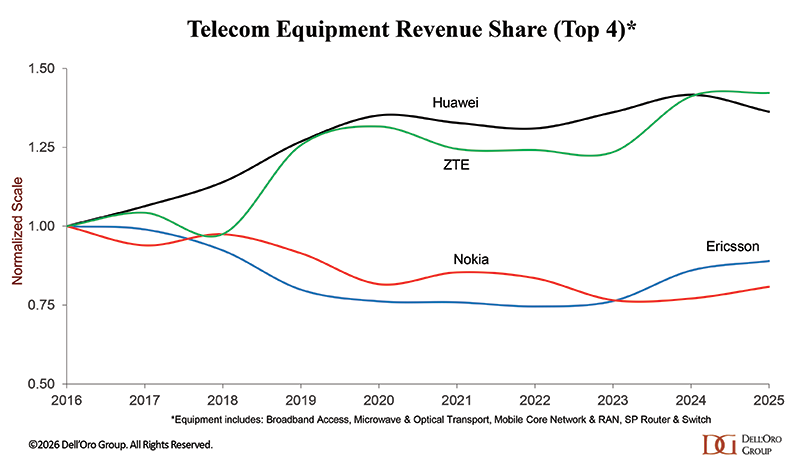

Our preliminary analysis suggests Ericsson’s overall telecom equipment revenue share declined by one to two percentage points between 2016 and 2025, settling at roughly 15% of the worldwide telecom equipment market in 2025. Considering the significant changes affecting the industry—including geopolitical shifts, supply chain disruptions, and the 5G investment cycle—this represents a fairly stable competitive position.

Looking Beyond the Headlines

At first glance, Huawei appears to be the clear winner of the past decade. Among the largest suppliers, Huawei and ZTE posted the strongest relative market share gains, increasing their telecom equipment positions across the six telecom programs tracked by the Dell’Oro Group by roughly 40% between 2016 and 2025.

Ericsson’s trajectory looks different. Instead of pursuing aggressive share gains across the broader telecom equipment market, Ericsson largely defended its position. Ericsson’s wireless focus is key. Wireless infrastructure has consistently represented nearly half of the telecom equipment market, making leadership in RAN strategically more important than expanding into adjacent segments.

The RAN Picture is More Favorable

The picture becomes even more interesting when focusing specifically on RAN.

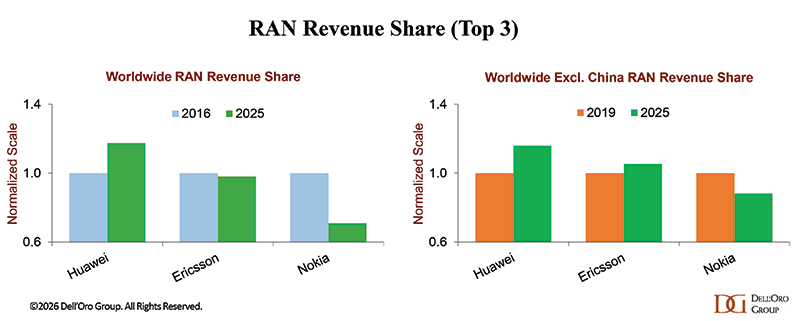

Globally, Ericsson’s RAN revenue share has remained relatively stable in the 25% to 30% range throughout most of Ekholm’s tenure. This stands in sharp contrast to the steep losses experienced between 2011 and 2016.

Meanwhile, Nokia experienced a more pronounced decline over the same period, while Huawei continued strengthening its global leadership position. Stability may not generate headlines, but in a mature infrastructure market dominated by a handful of global suppliers, maintaining share can be an important achievement.

The China Impact

Any assessment of Ericsson’s market position should also consider regional dynamics.

China has become increasingly difficult for foreign vendors, particularly amid geopolitical tensions and reciprocal restrictions affecting telecom infrastructure procurement—we estimate Ericsson and Nokia’s combined RAN revenue share in China has declined by 11 PPs between 2019 and 2025. As a result, global market share figures understate Ericsson’s competitive performance in many of its core markets.

Excluding China, Ericsson’s position actually improved between 2019 and 2025, gaining approximately four percentage points of RAN market share. Huawei also gained share outside China, while Nokia lost ground.

It is also worth noting that the US has played an outsized role in Ericsson’s RAN performance. In fact, if we normalize for both China and North America, Ericsson’s RAN share is stable while Huawei and Nokia are up.

Market Share Is Only One Part of the Story

Of course, market share does not provide the full picture.

Investors will also judge the period based on profitability, shareholder returns, and the success of strategic initiatives such as the enterprise expansion and the Vonage acquisition. Some of these initiatives remain works in progress, and their long-term value may not be fully understood for years.

Nevertheless, market share provides an objective scorecard. By that measure, Ericsson appears to have successfully halted a long-running decline, maintained its RAN leadership position, and strengthened its standing in some markets outside China.

Looking Ahead

The next CEO will inherit a company facing new challenges. Mobile data traffic growth is slowing, and operator capital spending is moderating. And within the capex mix, operators are shifting focus toward areas more closely tied to the data center wave, creating a double headwind for suppliers that remain more dependent on wireless infrastructure. AI is on the rise in network operations and in the RAN. And the role of SW is evolving. 6G is on the horizon, but cumulative 6G RAN revenue in the first six years of its cycle is projected to be 10% to 20% lower than the comparable period in the 5G cycle.

At the same time, Per Narvinger will inherit a company whose competitive foundation is considerably more stable than it was in 2017. While the industry appears to be changing faster today than it did when Börje took over, and some believe Ericsson has missed the data center wave, I get the impression that Ericsson is more confident in its position and prospects today than it was when Börje began.

That may ultimately become one of Börje Ekholm’s most long-lasting contributions. At the end of the day, he may be remembered less for any single metric—whether RAN market share, profitability, or shareholder returns—and more for restoring Ericsson’s competitiveness and preserving its position among the world’s leading telecom infrastructure suppliers.