Open RAN has made significant progress since the O-RAN Alliance was formed in 2018 to “re-shape the RAN industry and ecosystem towards more intelligent, open, virtualized, and interoperable networks.” However, the results to date have been mixed. Open fronthaul (Open FH) is increasingly being specified as a baseline capability for next-generation RAN platforms. At the same time, supplier diversity has not improved. In fact, RAN market concentration is higher today than it was before the alliance was established. Also, uneven adoption across greenfield, early-adopting, and early-majority operators contributed to a sharp capex deceleration following the Open RAN peak in 2022. That slowdown fueled concerns about the movement’s momentum, even with single-vendor Open RAN.

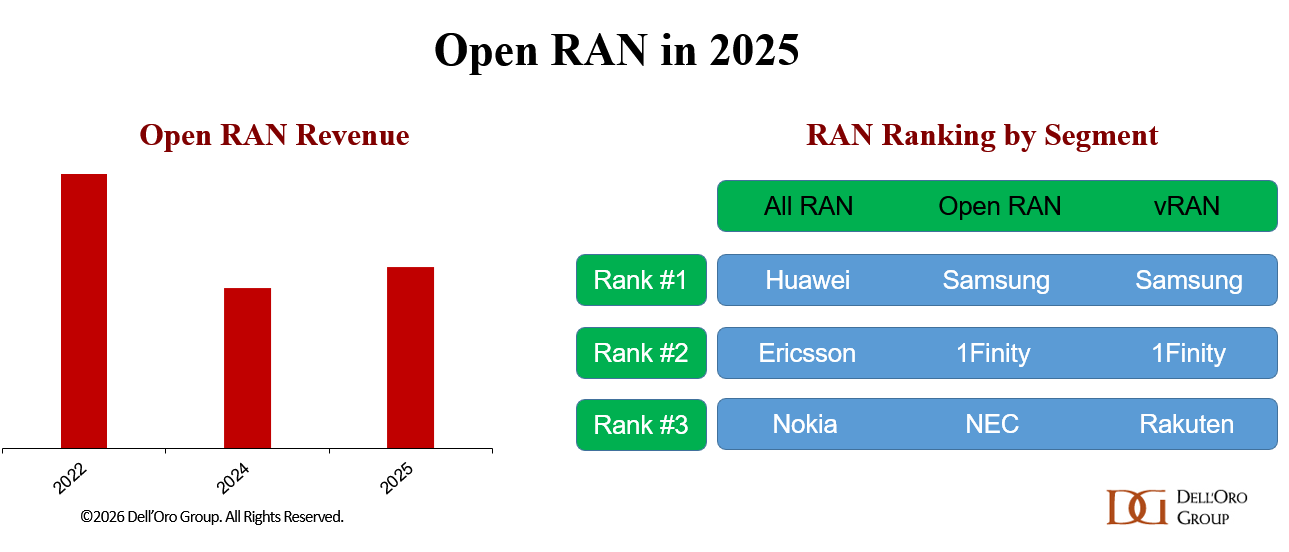

Market conditions improved in 2025. Following the roughly 40 percent decline between 2022 and 2024, preliminary findings suggest worldwide Open RAN revenue grew at a double-digit rate in 2025. Virtualized RAN (vRAN) revenue also stabilized, although at a more modest pace. Several factors help explain this reversal, including easier year-over-year comparisons, more favorable RAN spending trends in regions with strong Open RAN exposure, and, to a lesser extent, increased activity among early-majority adopters.

Vendor rankings did not change significantly, but the broader RAN landscape evolved in ways that also affected the Open RAN and Cloud RAN ecosystems. Both Mavenir and NEC revised their RAN strategies. Mavenir is now focusing more on small cells and non-terrestrial networks (NTN), while NEC is prioritizing vRAN and Massive MIMO. Meanwhile, 1Finity moved up one spot in the Open RAN ranking.

The incumbent Western suppliers are fully hedged. Ericsson and Nokia continue to support Open RAN while maintaining integrated portfolios. According to Ericsson’s latest update, 160 radio models will be Open-RAN-proven by the end of 2026. Likewise, Nokia’s recently introduced AI-RAN-ready Doksuri radios include compatibility with Open fronthaul standards.

Looking ahead, the positive momentum is expected to continue into 2026, with both Open RAN and vRAN projected to grow this year. The longer-term outlook for Open RAN and Cloud RAN also remains favorable. We have not changed the long-term assumptions communicated in the most recent forecast update. To recap, near-term Open RAN revenue projections were revised downward, while long-term growth expectations strengthened.

Virtualization remains a key pillar of next-generation RAN platforms. At the same time, Cloud RAN projections were lowered in the most recent five-year forecast. Still, Cloud RAN is expected to account for roughly 15 to 20 percent of the total RAN market by 2030.

Although the narrative around Open RAN improving supplier diversity has clearly cooled, the emerging GPU-RAN and software RAN wave is reopening the conversation about non-traditional suppliers playing a larger role in the RAN ecosystem. That said, the base case outlook for mixing and matching vendors remains limited. Multi-vendor RAN is still expected to account for less than 5 percent of total RAN deployments by 2030.

For more information about our RAN and Open RAN coverage, please see https://www.delloro.com/advanced-research-report/openran/