As mobile networks evolve to support more bandwidth, multiple technologies/frequencies, and increasingly diverse use cases—from eMBB to FWA, private wireless, and IoT—the complexity of operating the Radio Access Network (RAN) continues to rise. At the same time, revenue growth remains constrained, limiting operators’ ability to scale opex alongside this complexity.

Intelligent RAN Automation—combining automation, AI/ML, and advanced analytics—is emerging as a critical enabler for managing network complexity, enhancing network performance, curtailing energy consumption, supporting new service models, and managing efficiencies/reducing opex. Most operators still remain between the Level 1 and 2 categories per the TM Forum; however, some of the early adopters are now slowly moving beyond basic automation toward Level 3 and 4 autonomous networks, where systems can reason, decide, and act with minimal human intervention. In this blog, we will review progress and expectations with autonomous networks.

The Autonomy Journey

RAN automation and intelligence are not new concepts. Existing 4G and early 5G networks already relied heavily on automation, but the role of automation has steadily evolved. Initial efforts focused on task-level efficiency, such as provisioning, configuration management, software upgrades, and alarm handling. With the first wave of 5G deployments, automation expanded into more advanced optimization use cases—building on 4G SON foundations—with closed-loop control for mobility management, load balancing, energy efficiency, and performance tuning using policy engines and domain analytics. Now, the industry is entering a new phase—AI-driven autonomy—where systems are no longer limited to predefined rules but can dynamically adapt to changing network conditions.

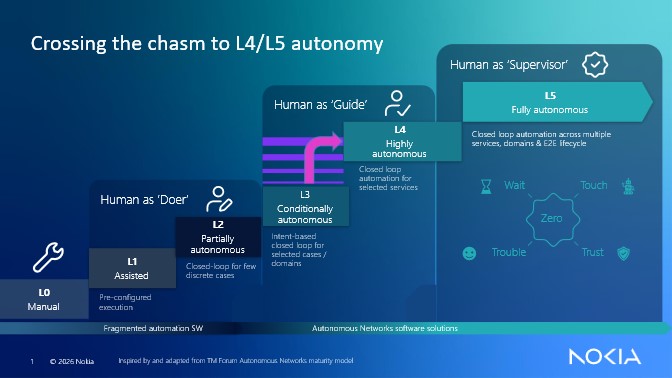

This evolution is captured in the TM Forum Autonomous Network framework:

- L0 – Manual operations: Everything is driven by humans

- L1 – Assisted operations: Manual and assisted human-based operations

- L2 – Partial automation: Some automation but humans still address the lion’s share

- L3 – Conditional automation: More AI, closed-loop operations and maintenance for select scenarios

- L4 – High autonomy: Nearly full automation for many scenarios

- L5 – Full autonomy: All AI, 100% automation, no human intervention – this is the end goal

Each transition brings the operators one step closer to the end goal of full autonomy without human intervention. The transition toward Level 4 represents a fundamental shift—from automating tasks to automating decisions. Vendors and operators broadly align on this transition. But the level of automation and pace of adoption will vary significantly depending on a confluence of factors. Still, the objective is clear: reduce human intervention while improving network performance/reducing opex.

Why Automation Matters

Mobile data traffic is still growing at a double-digit rate, though the pace is clearly slowing (up 16% in 2025 per Ericsson Mobility Report). At the same time, operator revenue growth increased at a 1% CAGR over the past ten years (Dell’Oro Capex Report). This implies that the operators have minimal wiggle room to expand capex and opex to manage the increased complexity required to deliver the appropriate network performance while supporting more demanding and diverse end-user requirements.

Operators believe RAN automation is essential and can help to deliver several key benefits:

- Maximize ROI on network investment

- Improve performance and experience

- Boost network quality

- Accelerate time to market

- Reduce complexity

- Reduce energy consumption

- Bring down CO2 emissions

Performance gains underpinned by Intelligent RAN will vary. Ericsson estimates that Intelligent RAN Automation solutions can improve spectral efficiency by 15%, while Huawei has demonstrated that its Intelligent RAN multi-band/multi-site 3D coordination feature can improve the user experience by up to 50% in some settings. Nokia has reported up to 80% efficiency gains with zero-touch radio network optimization. Meanwhile, ZTE has demonstrated tangible benefits from large-scale L2/L3 automation, including around a 30% reduction in fault recovery times and roughly 20%+ improvements in resource utilization. Samsung has incorporated AI and automation into its 5G RAN portfolio, although publicly disclosed large-scale L4 deployments remain more limited than those of larger RAN suppliers.

RAN Automation Achievements

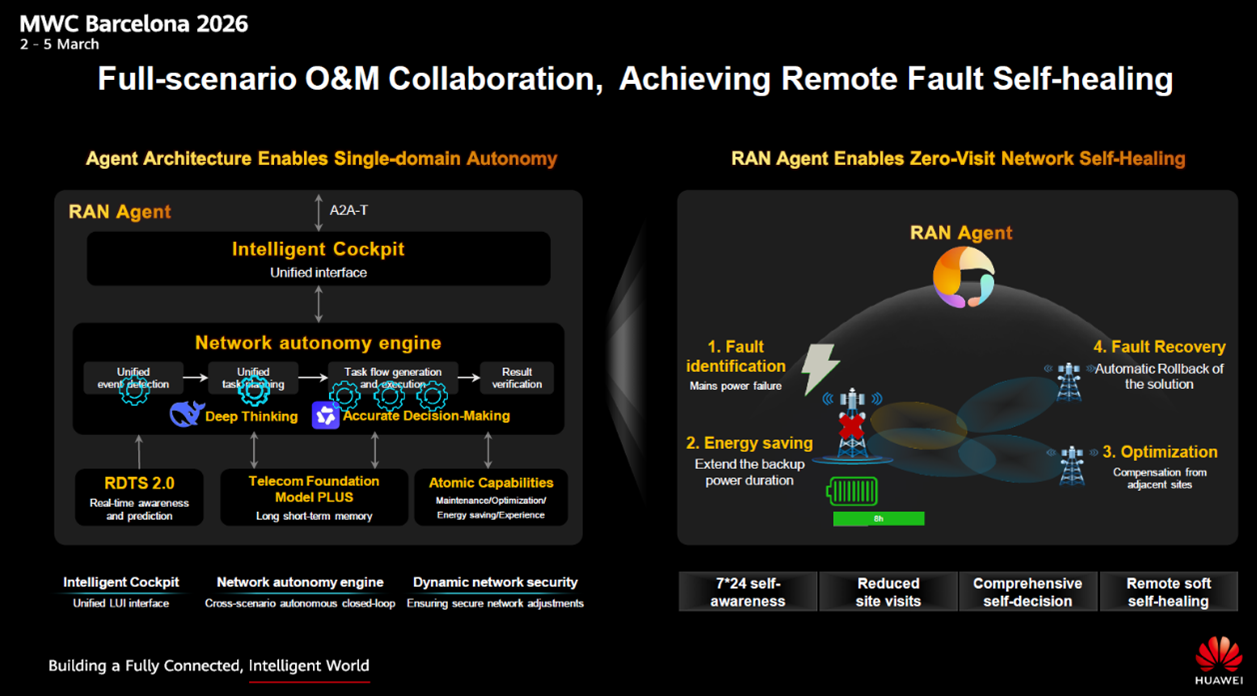

Level 4 takes it a step further. While Level 3 involves AI-driven closed-loop automation in defined scenarios, often with human oversight, L4 networks increasingly leverage multi-agent and AI-driven systems that can independently analyze, decide, and act within defined parameters with minimal approval. L4 is key to realizing zero-touch networks that detect and fix problems before they become major issues.

At L4, networks can:

- Execute closed-loop automation across domains

- Predict and resolve issues before they impact users.

- Continuously optimize performance with real-time decisions

- Improve spectral efficiency, user experience, and network reliability

- Reduce energy consumption

- Full-scenario O&M collaboration

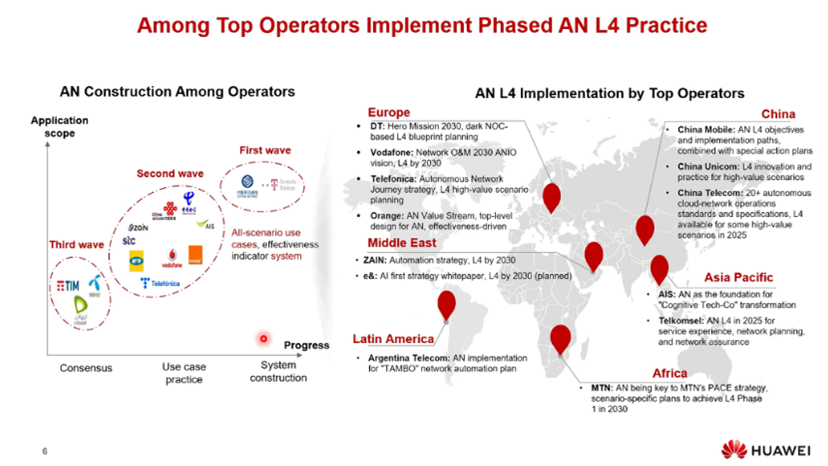

L4 Market Status: Early Days, but Real

While some advanced domains like RAN optimization are approaching Level 3, the overall industry remains in the Level 1-2 range (TM Forum), where automation is still largely domain-specific and rule-based. Most deployments today are still limited to specific use cases rather than full network-wide autonomy. At the same time, Level 4 is no longer theoretical. Implementations remain limited to a small group of leading operators, but real progress is now visible.

Rakuten Mobile has already proven L4 at scale in a live RAN network, with TM Forum validation for RAN energy efficiency. Based on production traffic, Rakuten is able to realize 20% RAN energy savings using AI-driven closed-loop control with no impact on customer experience.

In June 2025, TDC NET and Ericsson achieved TM Forum Level 4 autonomy certifications for a live RAN deployment. The Level 4 validation focused on Ericsson’s PCEM software, which reduced the energy required to transmit 1 GB of data by approximately 5% under live network conditions.

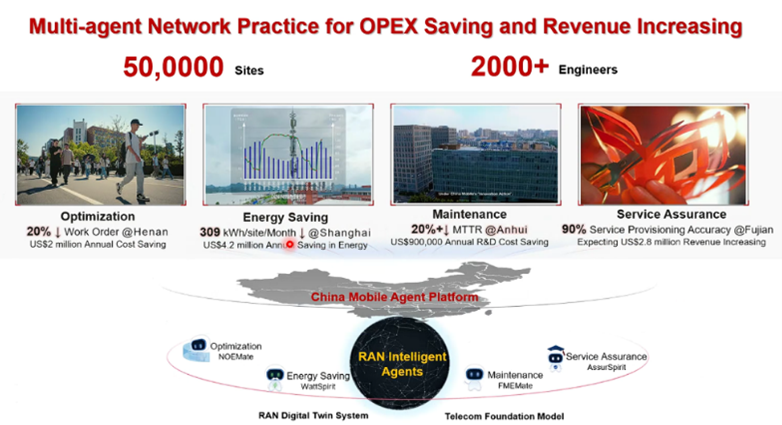

China Mobile reported Level 4 progress through TM Forum ANLAV assessments at Innovate Asia 2025, receiving certifications across multiple operational domains, including service assurance, wireless energy optimization, and IP fault management. While these scenario-based assessments do not imply end-to-end network-wide Level 4 autonomy, they reflect meaningful progress toward large-scale operational automation in several high-value functions.

China Telecom is an emerging L4 RAN adopter, applying automation in high-value domains such as optimization, assurance, and energy savings, with selected AI initiatives delivering double-digit efficiency improvements.

China Unicom is demonstrating targeted L4 RAN automation in areas such as traffic optimization, automated assurance, and energy efficiency, with broader deployment still maturing.

Huawei is also working with operators globally on large-scale L4 trials. In addition to the Chinese carriers, Huawei has indicated engagements with 10+ international operators implementing L4 autonomous networking in live production environments.

Nokia and STC have demonstrated Level 4 autonomy in live RAN operations, moving beyond traditional SON toward AI-driven closed-loop operations. During the Hajj period, despite traffic increasing by 40%, the network executed 10K autonomous operations per hour, helping improve DL throughput by approximately 10%.

Although newer entrants/smaller RAN suppliers are contributing to SMO, rApps/xApps, and cloud automation, most scaled L4 RAN deployments today remain associated with the largest established RAN suppliers.

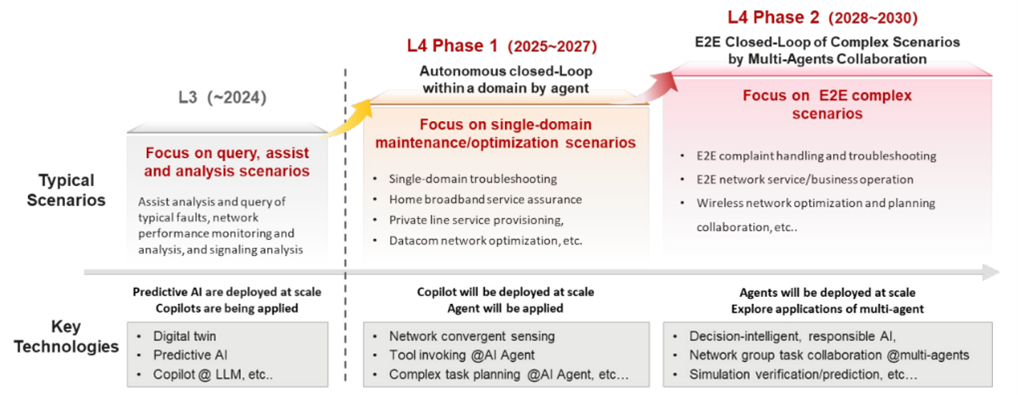

Level 4 Roadmap

Most L4 deployments today are scenario-based rather than network-wide, with autonomy achieved in specific domains such as energy optimization or traffic management. And it will still take time before even the leading operators implement L4 across the broader network. Although the TM Forum envisions that the next couple of years will be critical for the autonomous closed-loop of L4 single-domain maintenance, optimization, and operation, the path to L4 will likely be slow and gradual and can at a high level be divided into two phases.

Phase 1: Single Domain-Level Automation Scenarios (Near-Term)

This phase focuses on high-value, low-risk use cases within individual domains:

- Closed-loop automation within RAN

- AI-assisted decision-making with human-defined guardrails

- Limited cross-domain coordination

- Energy optimization, automated fault detection, traffic and load optimization

Phase 2: Cross-Domain Autonomy (Medium-Term)

This phase extends autonomy across domains, enabling end-to-end service orchestration:

- Multi-domain coordination (RAN, transport, core)

- Intent-driven automation

- Minimal human intervention

- E2E assurance, cross-domain root cause analysis, mobile network optimization

RAN agents are emerging as a key enabler in accelerating the transition to Level 4 autonomy by shifting networks away from rule-based automation toward a more adaptive, goal-driven model. Unlike traditional systems that depend on predefined scenarios, these agents can interpret intent, assess real-time conditions, and take action while continuously learning from new data. This allows networks to move beyond static workflows into context-aware decision-making, real-time adaptation, and ongoing optimization.

In the near term, RAN agents enhance domain-level automation by making operations more scalable and efficient—for instance, by dynamically adjusting energy usage based on traffic patterns or continuously tuning network parameters. The real step change is expected to come from cross-domain collaboration, where distributed agents coordinate across RAN, transport, and core to address issues such as congestion and enforce end-to-end service-level objectives. While this multi-agent approach should unlock greater scalability, faster innovation, and continuous improvement, it also introduces new challenges around coordination, interoperability, and building trust in autonomous decision-making.

In summary, the shift towards RAN Automation is happening. The journey is taking longer than expected (many operators promised large-scale L4 by 2025). In most cases, autonomy today is achieved within well-defined guardrails, with humans still setting policies and objectives. Still, there is no question that this is a key pillar in all future RAN and telecom roadmaps. The transition to Level 4 marks a pivotal shift—from automating tasks to automating decisions—enabling networks that are more adaptive, efficient, and resilient. While most operators remain in the early stages, the trajectory is clear. Early deployments demonstrate that L4 is achievable today, particularly in targeted domains.

The pace of this next phase remains highly uncertain. The transition to L4 autonomous networks is as much a human challenge as a technical one. It is natural to fear losing control and giving it up to machines. At the same time, networks will become more complicated, and the revenue upside remains limited, meaning operators who can accelerate this transition towards cross-domain autonomy and RAN agents will likely be in a better position. Ultimately, RAN automation will play a growing role in the second half of 5G and likely from the start with 6G.