Last week, izzi, Mexico’s largest cable operator, announced that it was deploying Harmonic’s cOS virtualized broadband platform alongside its Pearl Remote Optical Line Termination (R-OLT) modules and Pearl outdoor node enclosures to extend its fiber network. The announcement is noteworthy because it is further evidence of the region’s cable operators continuing a wholesale shift away from DOCSIS and HFC to fiber. But it is also noteworthy in that it signals a shift towards more flexible R-OLT platforms as the fiber foundation for both cable operators and telcos in the region. Latin America is experiencing a fiber overbuild cycle that, in many markets, is more aggressive than anything North American cable operators have faced. Lower labor costs across the region have made greenfield fiber construction economically viable for a wide range of players — telcos, utilities, and new entrant ISPs — reshaping competitive dynamics almost city by city.

The specific benefits of R-OLTs are well matched to what izzi and other telco and cable operators in the region need to execute a large-scale fiber migration efficiently and competitively:

- Reduced fiber feeder costs. Traditional centralized OLT deployments require operators to run long fiber feeder routes from a headend or hub site out to the access network. R-OLT platforms eliminate much of that feeder infrastructure by pushing the OLT function out to the node, dramatically shortening the fiber runs required to reach subscribers. In a market where izzi is deploying across a large and geographically diverse service territory, that reduction in feeder fiber translates directly into lower capital expenditure per home passed. Just as important as reduced capex is the faster time-to-market that an R-OLT architecture can provide.

- Ability to leverage existing node infrastructure. One of the most underappreciated advantages of R-OLT platforms for cable operators is the ability to reuse what they already own. Izzi has an established outside plant with node locations distributed across its footprint — real estate, conduit, power feeds, and field infrastructure that took years and significant capital to build. Being able to drop into those existing locations rather than requiring new facility construction to keep overall deployment costs down and to get to market faster.

- Right-sized port density and scalability. R-OLT modules are built for high PON port density within a compact form factor, which matters significantly when you’re trying to maximize the number of subscribers serviceable from a single field location. Higher port density means fewer node sites required to cover a given subscriber footprint, fewer truck rolls per unit of coverage, and a more scalable architecture as izzi expands its fiber deployment over time. It also provides a cleaner path to adding capacity incrementally as subscriber uptake grows, rather than requiring operators to over-provision upfront

- Power and space savings. Traditional OLT cabinet deployments carry substantial power and space requirements — challenges that become acute when you’re trying to deploy at scale across a distributed field network rather than in a controlled headend environment. Optical node housings are designed for outdoor deployment with power consumption and thermal management designed for the field, not the headend. For izzi, those savings compound across hundreds of node sites over the course of a multi-year rollout, with meaningful implications for both capital and operating expenditures.

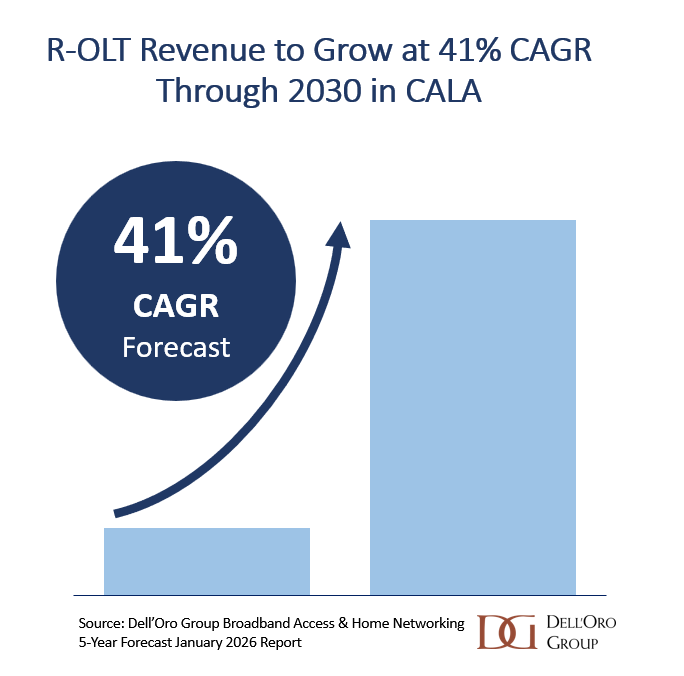

The Remote OLT Trend in Latin America

izzi’s decision is not happening in isolation. R-OLT as an architecture is gaining traction across Latin America largely because it aligns well with the region’s deployment realities. Unlike central office OLT deployments that require operators to run long fiber runs from a headend or hub site out to the field, a R-OLT pushes the OLT function closer to subscribers — reducing fiber costs, improving latency, and allowing operators to expand incrementally without massive upfront infrastructure investment.

izzi’s decision is not happening in isolation. R-OLT as an architecture is gaining traction across Latin America largely because it aligns well with the region’s deployment realities. Unlike central office OLT deployments that require operators to run long fiber runs from a headend or hub site out to the field, a R-OLT pushes the OLT function closer to subscribers — reducing fiber costs, improving latency, and allowing operators to expand incrementally without massive upfront infrastructure investment.

The broader point is that Latin American cable operators looking at fiber migration are increasingly finding that R-OLTs strike a favorable balance of deployment cost, operational simplicity, and competitive positioning. The architecture doesn’t require operators to choose between upgrading their HFC plant and building fiber — it gives them a fiber-first path that can be executed in parallel with or as a replacement for legacy infrastructure, depending on the specific competitive and financial dynamics of a given market.

Harmonic certainly isn’t the only R-OLT supplier benefiting from this trend. Huawei and ZTE both have node-based OLT platforms they have been shipping into the CALA market for some time. Calix and Vecima have also found some traction for node-based OLT platforms in the region.

ONT Flexibility Just as Critical

One detail in the announcement that deserves more attention than it typically gets: izzi’s deployment integrates third-party ONTs through Harmonic’s Open ONT strategy. This is not a trivial design choice. CPE procurement is one of the larger ongoing cost variables in a multi-year fiber deployment, and vendor lock-in on ONTs has historically been a significant source of margin erosion for operators. By explicitly engineering an open ONT architecture into the deployment, izzi retains the flexibility to source CPE competitively as the deployment scales, rather than being captive to a single supplier’s pricing and roadmap.

For operators in Latin America where broadband ARPU is often significantly lower than in North American markets, total cost of ownership discipline in CPE is a necessity. It can be argued that ONT costs are a significant reason why Huawei, ZTE, Fiberhome, Humax, and Skyworth have found success in the region. Offering operators low-cost GPON ONTs has helped reduce the success-based capex budgets for operators in Brazil, Argentina, Mexico, and Uruguay, among others. For izzi, being able to mix-and-match ONTs will give them pricing leverage as they look to expand their fiber homes passed and connected.