If you want to amp up the pressure in your life, try getting up in front of twenty to thirty thousand people, some of whom influence whether or not you keep your job, and lay out a clear, concise strategy in a world full of upheaval.

That’s what Cisco and HPE’s leaders did this month, addressing customers, shareholders, employees, and analysts and making the case for why their respective IT brands are best suited to guide enterprises through the uncertainties of AI.

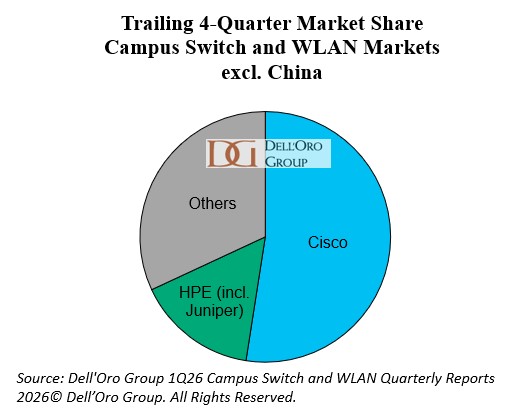

Together, these two vendors dominate more than two-thirds of the campus networking market outside China (see Figure). But while industry focus is on the jaw-dropping spending on GPUs and Data Center infrastructure, it’s a challenge for both Cisco and HPE to explain why campus networking remains relevant. Executive quotes captured during the conferences reveal similarities and differences in these vendors’ messages—and provide insight into where they see opportunities to gain share.

Theme 1 – The Enterprise AI Revolution

Takeaway

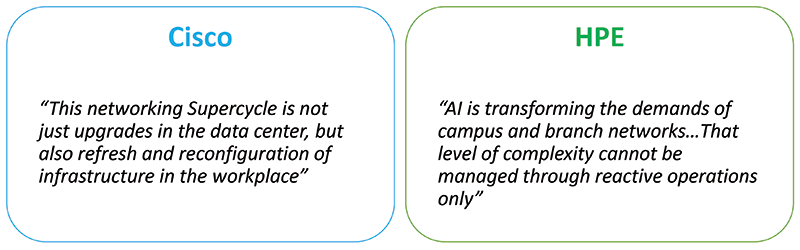

Both vendors have tied the AI revolution to changes required in campus networks. Cisco executives pointed to higher traffic levels extending bottlenecks from GPUs to networking, even to the campus, driving the need for refresh. To meet this new demand, Cisco announced the C9550, a 400G Fixed form factor switch for the Campus core.

HPE executives positioned the impending AI transformation first and foremost as an operations challenge, emphasizing Juniper’s advanced AI operations capabilities, such as a powerful set of AI Agents and skills, a Large Experience Model to prevent problems with Zoom, and a suite of autonomous actions that can be undertaken by Marvis.

Theme 2 – Security and Networking

Takeaway

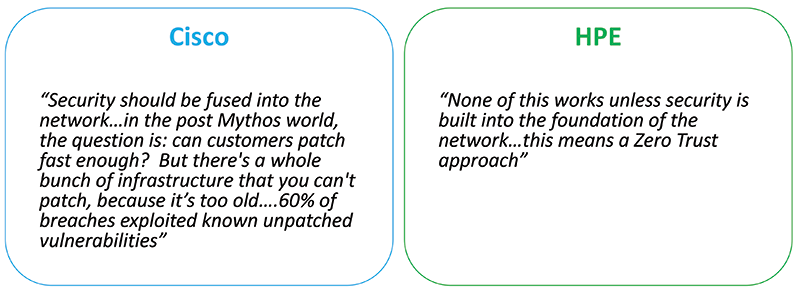

Neither Cisco nor HPE has been able to challenge Palo Alto’s lead in the network security space, so arguments that leverage strengths in networking to advance security market share gain make sense.

Cisco brought a new angle on security at Cisco Live, dubbing the “Mythos Moment” as a wakeup call for enterprises with unsupported equipment. They announced Live Protect on their new Campus Smart switches (GA September 2026), which will allow enterprises to track whether specific vulnerabilities are being exploited, and then apply compensating remediation, even before patches are available. Cisco also emphasized post-quantum security of their new switches.

HPE’s security focus was on converging SSE and SD-WAN, announcing HPE Networking EdgeConnect, which unifies the two products in an AI-native console. HPE executives underlined the importance of a universal ZTNA, covering universal policy as well as universal identity for humans, workflows, and agents. Identifying, securing, and putting up guardrails for AI Agents was seen as a critical step by both vendors.

Theme 3 – Digital Complexity

Takeaway

Both Cisco and Juniper addressed the increasing complexity of IT by presenting a single point of entry to their management ecosystems; to systems managing campus equipment as well as other domains such as compute, applications and workflows.

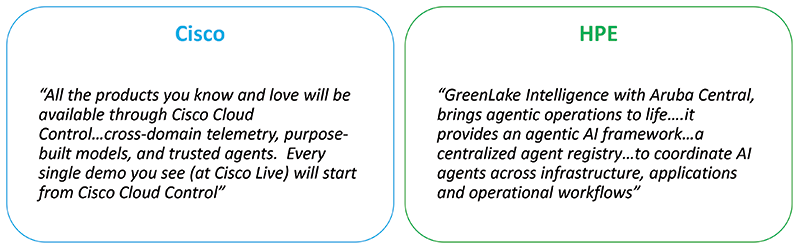

Through Cisco Cloud Control (which is in “controlled availability” in the US), enterprises can gain access to the Meraki Dashboard and, through the dashboard, access Catalyst Center. Cisco executives hope that Cloud Control will be a breakthrough in addressing enterprises’ complaints about the complexity of Cisco’s deep feature list. However, the coexistence of Meraki Dashboard, AI Canvas, and Cisco Cloud Control may also contribute to enterprises’ perception of complexity.

HPE emphasized the necessity of an agentic framework in hybrid deployments (across different clouds and on premises) and announced GreenLake Intelligence, which is being rolled out across 2026 and 2027. While the HPE Discover keynote showed it interacting with Aruba Central, Mist is not available in GreenLake Intelligence today.

Theme 4 – Convergence

Takeaway

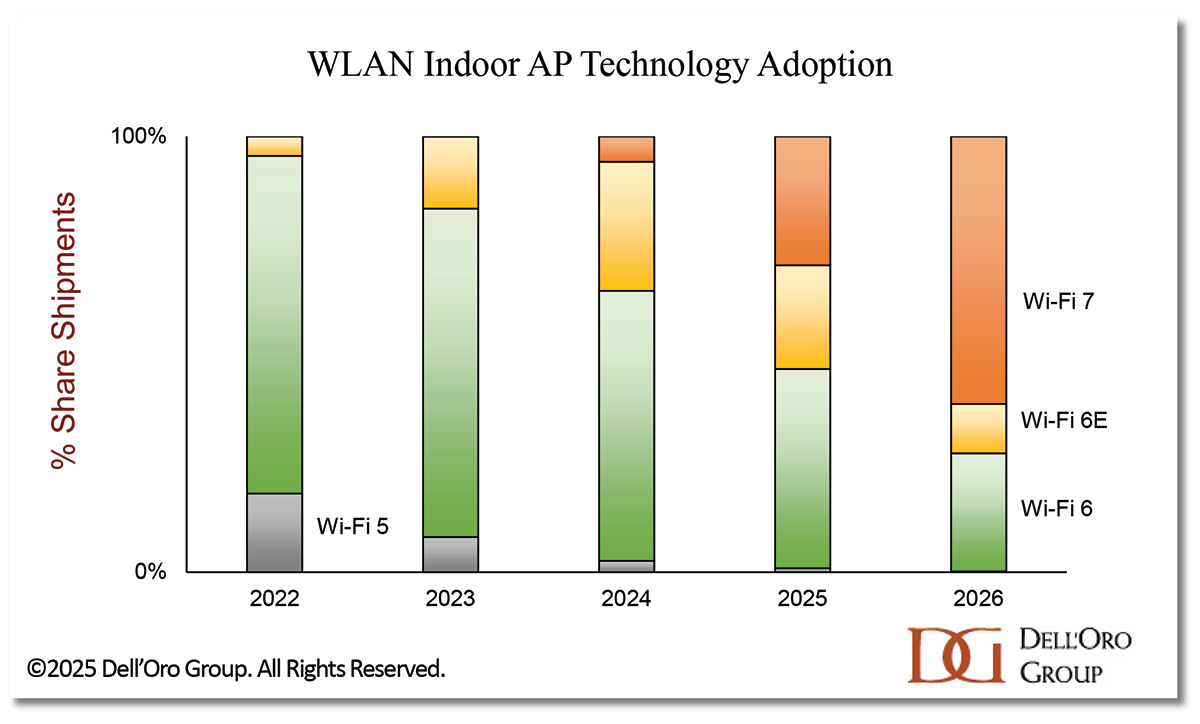

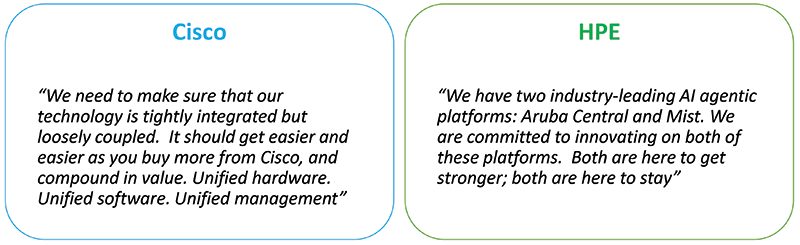

It took Cisco about ten years to combine the Catalyst and Meraki product teams, something that HPE did (by combining Aruba and Mist development teams) in a few months. However, Cisco has now passed through the heavy lifting phase: their Wi-Fi 7 APs can be managed either through the cloud or by a controller, and at Cisco Live, the company completed its WLAN lineup by introducing the CW9177, an outdoor Wi-Fi 7 AP. The newer Catalyst switches can also be managed from the cloud. This has allowed Cisco to shift the focus onto convergence across their broader portfolio, with Cisco Cloud Control as a key piece of this strategy.

Meanwhile, less than a year after HPE acquired Juniper, the company announced that its first converged AP was generally available. The hospitality AP (723H) can be deployed with Mist or Aruba Central, has the Aruba tessellated case design, and includes the dedicated scanning radio to provide the necessary telemetry for Mist. HPE also announced that Aruba’s CX switches are now supported in Mist, although some variants will become available in the fall.

Over and above the hardware platforms, HPE has continued on its journey of cross-pollinating Aruba Central and Mist. At HPE Discover, they announced that Marvis Actions would be available in Aruba Central. The company’s consistent message about commitment to both cloud-managed platforms is reassuring to existing customers, but can confuse new, potential customers interested in a cloud-managed solution from HPE.

Is Campus Networking Relevant?

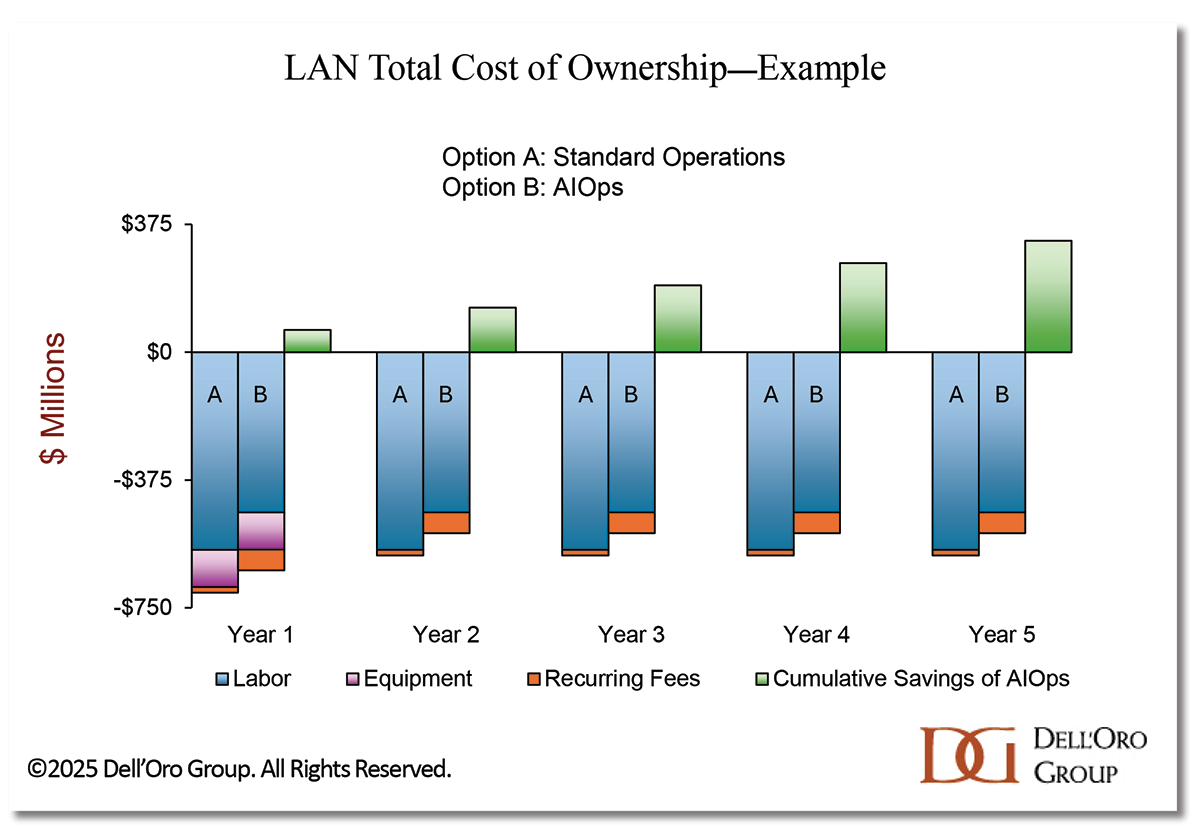

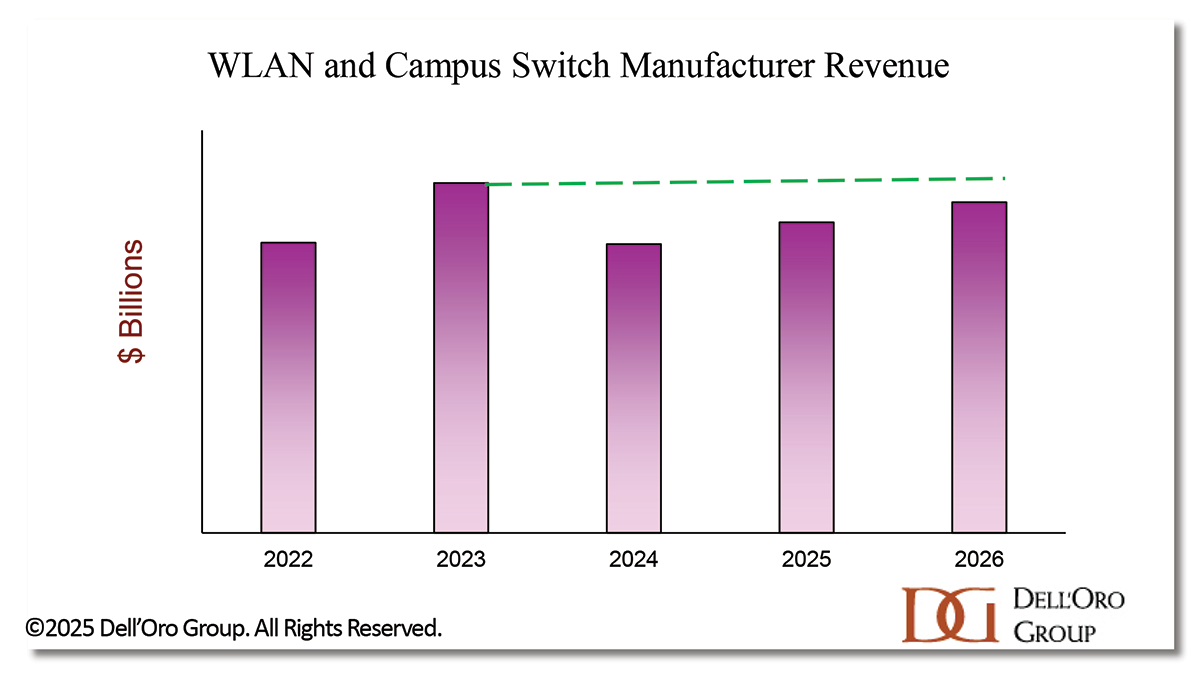

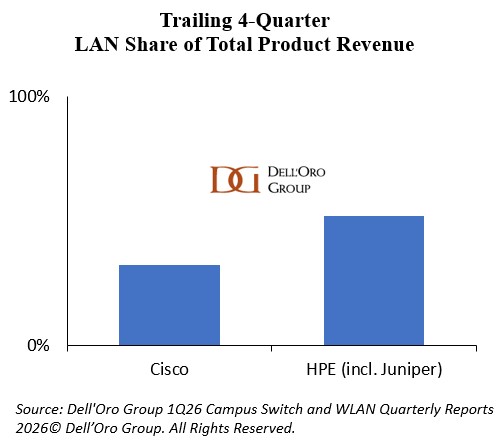

With enterprises increasingly distracted by AI projects, the emphasis on campus network security, operational simplicity, and automation by both Cisco and HPE was designed to refocus attention back to basics. Revenue from LAN equipment (WLAN and Campus Switches) represents a significant portion of both companies’ sales (see Figure).

With enterprises increasingly distracted by AI projects, the emphasis on campus network security, operational simplicity, and automation by both Cisco and HPE was designed to refocus attention back to basics. Revenue from LAN equipment (WLAN and Campus Switches) represents a significant portion of both companies’ sales (see Figure).

In Cisco’s vision of the future, every worker manages a team of AI Agents, with these agents behaving more like unruly teenagers than fully formed humans. The vision is underpinned by an urgency to refresh campus equipment, both for security and to prepare for growing agentic traffic.

HPE, on the other hand, is focusing attention on reassuring its Aruba customer base as Juniper is brought into the fold. AI is only as strong as the foundation beneath it, say HPE executives. Autonomous operations and AI-driven networking are prerequisites for scaling enterprise AI, and a solid foundation starts with a self-driving network.