First Commercial 5G Core expected in 2020

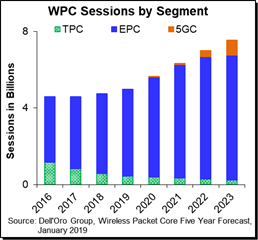

The latest Wireless Packet Core 5-Year Forecast report shows that the projected five-year compounded annual revenue growth rate (CAGR) for the Wireless Packet Core (WPC) market is 3 Percent (2018-2023).

“Initial 5G New Radio (5G NR) network launches are being implemented with 5G Non-standalone (5G NSA) architectures that utilize the 4G Evolved Packet Core (EPC); therefore we have pushed out by one year (from 2019 to 2020), our expectations of when we will see the first commercial deployments of 5G Core,” said Dave Bolan, analyst with the Dell’Oro Group.

“Initial 5G New Radio (5G NR) network launches are being implemented with 5G Non-standalone (5G NSA) architectures that utilize the 4G Evolved Packet Core (EPC); therefore we have pushed out by one year (from 2019 to 2020), our expectations of when we will see the first commercial deployments of 5G Core,” said Dave Bolan, analyst with the Dell’Oro Group.

“WPC revenue growth is expected to continue throughout the forecast period due primarily to subscriber growth, migration of more subscribers to VoLTE, and increasing data usage per subscriber. Other factors contributing to growth is the upgrade of EPC to a control and user plane separation (CUPS) architecture to handle 5G traffic and Internet of Things (IoT),” added Bolan.

Other highlights from the Wireless Packet Core 5-Year Forecast Report:

- EPC will be the workhorse for the core throughout the forecast period. We expect it to peak in revenue in 2022. From a volume perspective, the number of sessions for EPC will increase through 2023.

- The drive toward Network Function Virtualization (NFV) with cloud-native virtual network functions (VNFs) will continue in the forecast period increasing the share of the revenue to 88% in 2023.

The Dell’Oro Group Wireless Packet Core 5-Year Forecast Report offers a comprehensive overview of market trends by network function implementation (Non-NFV and NFV), covering revenue, sessions, average selling price, and regional forecasts for various network functions.

To access the full report, contact us at dgsales@delloro.com.

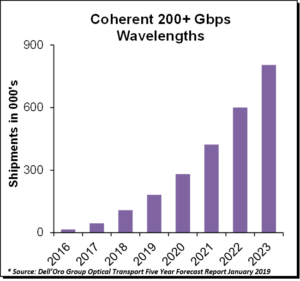

to approach $80 billion over the next five years. The majority of the Optical Transport revenue will be driven by demand for coherent 200+ Gbps wavelengths.

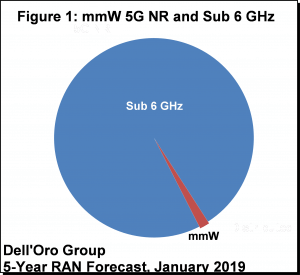

to approach $80 billion over the next five years. The majority of the Optical Transport revenue will be driven by demand for coherent 200+ Gbps wavelengths. The latest Mobile RAN 5-year forecast report claims the robust demand for 5G NR will propel the cumulative worldwide RAN market to nearly $160 B over the next five years.

The latest Mobile RAN 5-year forecast report claims the robust demand for 5G NR will propel the cumulative worldwide RAN market to nearly $160 B over the next five years.