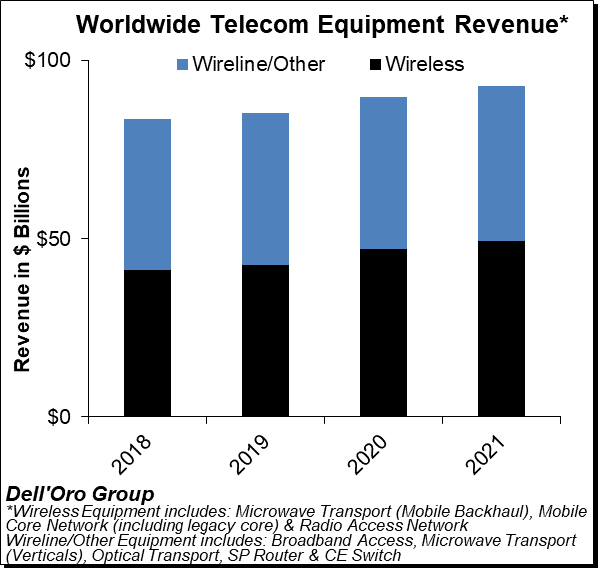

We just wrapped up the 3Q20 reporting period for all the Telecommunications Infrastructure programs covered at Dell’Oro Group. Preliminary estimates suggest the overall telecom equipment market – Broadband Access, Microwave & Optical Transport, Mobile Core & Radio Access Network, SP Router & Carrier Ethernet Switch (CES) – advanced 9% Year-Over-Year (Y/Y) during 3Q20 and 5% Y/Y for the 1Q20-3Q20 period.

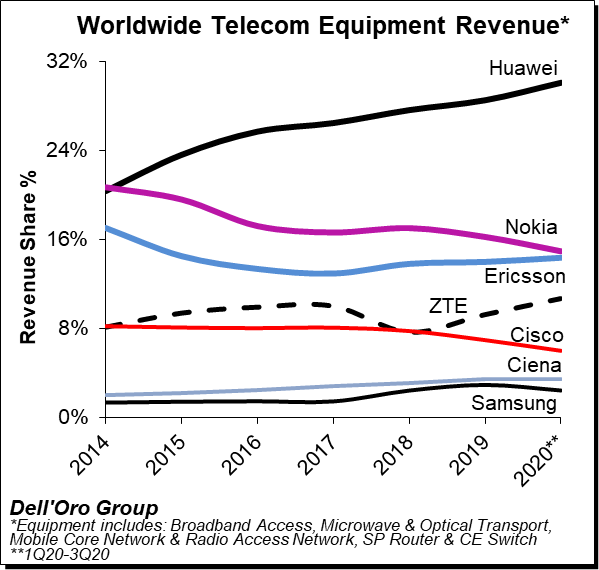

The analysis contained in these reports suggests revenue rankings remained stable between 2019 and 1Q20-3Q20, with Huawei, Nokia, Ericsson, ZTE, Cisco, Ciena, and Samsung ranked as the top seven suppliers, accounting for more than 80% of the total market. At the same time, revenue shares continued to be impacted by the state of the 5G rollouts in highly concentrated markets.

We estimate the following revenue shares for 2019 and the 1Q20-3Q20 period for the top seven suppliers:

Top 7 Suppliers

Year 2019

1Q20 to 3Q20

Huawei

28%

30%

Nokia

16%

15%

Ericsson

14%

14%

ZTE

9%

11%

Cisco

7%

6%

Ciena

3%

3%

Samsung

3%

2%

Additional key takeaways from the 3Q20 reporting period include:

Following the 4% Y/Y decline during 1Q20, the positive trends that characterized the second quarter extended into the third quarter, underpinned by strong growth in Optical Transport and multiple wireless segments including 5G RAN, 5G Core, and Microwave Mobile Backhaul. Technology segments that were impacted more materially by COVID-19 and the lockdowns during 1Q20 continued to stabilize in the quarter.

Preliminary estimates indicate increasing Mobile Infrastructure and Optical Transport revenues offset declining investments in Microwave Transport and SP Routers & CES for the 1Q20-3Q20 period.

The overall telecom equipment market continued to appear disconnected from the underlying economy. While the on-going transition from 4G to 5G is helping to offset reduced capex in slower-to-adopt mobile broadband markets, we also attribute the disconnect to the growing importance of connectivity and the nature of this recession being different than in other downturns improving the visibility for the operators.

With investments in China outpacing the overall market, we estimate Huawei and ZTE collectively gained about 3 percentage points of revenue share between 2019 and 1Q20-3Q20, together comprising more than 40% of the global telecom equipment market.

The Dell’Oro analyst team has not made any material changes to the overall outlook and projects the total telecom equipment market to advance 5% to 6% in 2020 and 3% to 4% in 2021. Total telecom equipment revenues are projected to approach $90 B to $95 B in 2021.

Dell’Oro Group telecommunication infrastructure research programs consist of the following: Broadband Access, Microwave Transmission & Mobile Backhaul, Mobile Core Networks, Mobile Radio Access Network, Optical Transport, and Service Provider (SP) Router & Carrier Ethernet Switch.

[wp_tech_share]

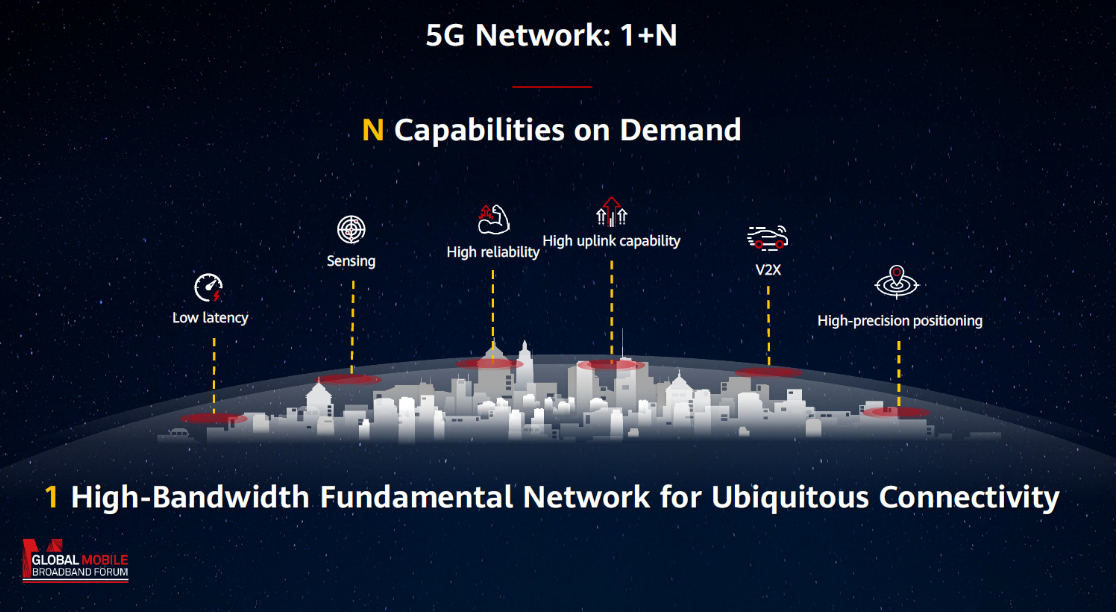

Huawei recently held its annual MBBF Forum. Even though we were not able to attend in person, it was an interesting event. Below we will add some color to five radio access network (RAN) related takeaways including 1) 5G=1+N; 2) Massive MIMO is a massive success; 3) There is more room left in the sub 6 GHz tank; 4) Site simplification will play an increasingly important role; 5) The outlook for vertical 5G activity is improving.

5G = 1+N (One foundational network plus N capabilities on demand)

If there is one thing we can all agree on after these first two years of commercial 5G deployments, it is that 5G means different things to different people.

While there is little disagreement that 5G now initially is just another G, providing operators with a compelling technology and business case to expand their respective mobile broadband networks to address todays use cases, the interpretation about the 5G opportunity tends to become more interesting as we look beyond the smartphone MBB use case. Because even if the narrative has morphed somewhat and the lion share of the capex in this initial wave is addressing what we know today, the long term vision still holds, namely that 5G has the potential to expand the role of connectivity beyond the MBB usage scenario and pave the way for new applications and use cases and expand the wireless based economy.

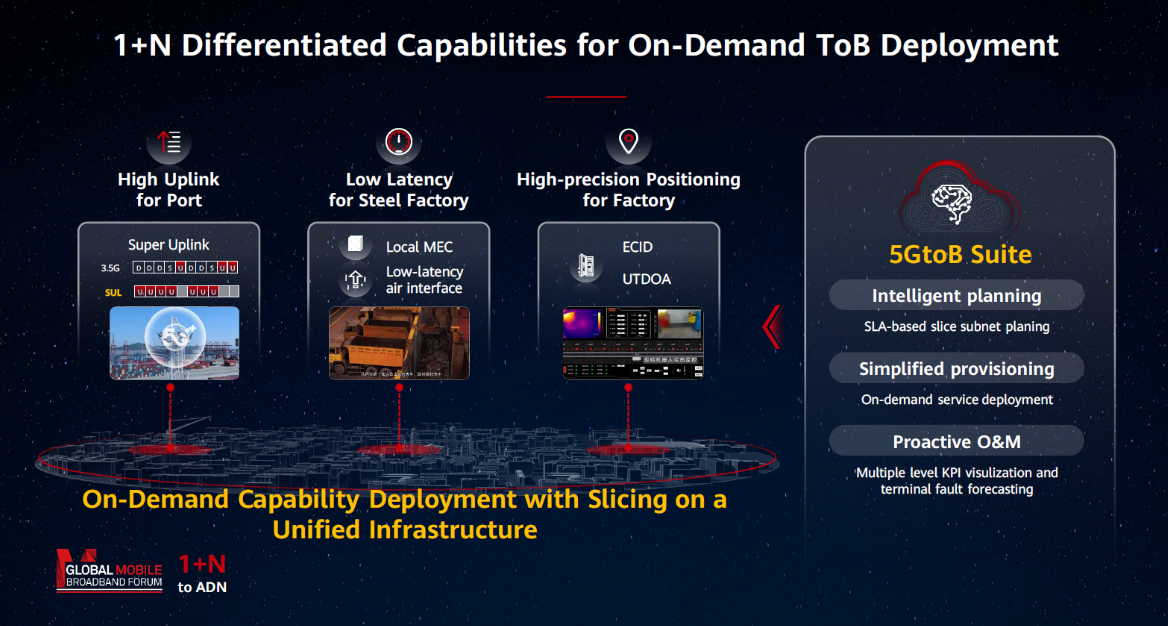

In order to address both the known and unknown opportunities with extremely diversified service requirements, Huawei is recommending operators build one foundational wide-area mobile broadband network with ubiquitous connectivity. The vision here is resting on the assumption that this foundational network combined with flexible on demand capabilities leveraging various spectrum bands (such as those designed for FDD or Super Uplink) to address diversified 5G service requirements for various people, things, and industries will ultimately enable the operators to provide optimized solutions from a technology and business case perspective for the various 5G opportunities.

Huawei MBBF 2020

Huawei MBBF 2020

TDD Massive MIMO is a mainstream technology

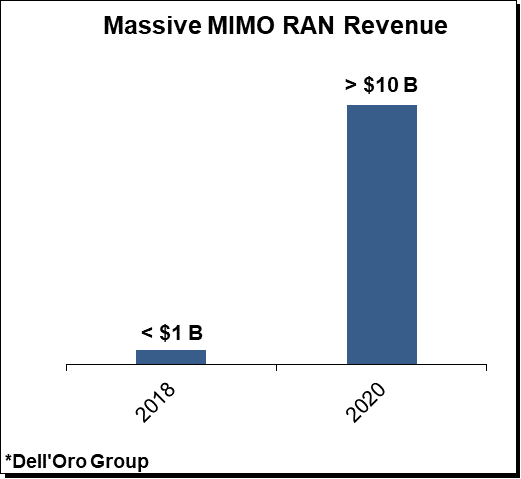

For a technology that was initially viewed as being mostly a fit for hotspot scenarios, Massive MIMO has come a long way, accelerating at a much broader and faster pace than initially expected. Preliminary estimates suggest Massive MIMO RAN investments remain on track to surpass $10 B for the full-year 2020, up nearly 20-fold in just two years. Cumulative Massive MIMO transceiver shipments are projected to approach 0.1 B to 0.2 B in 2020.

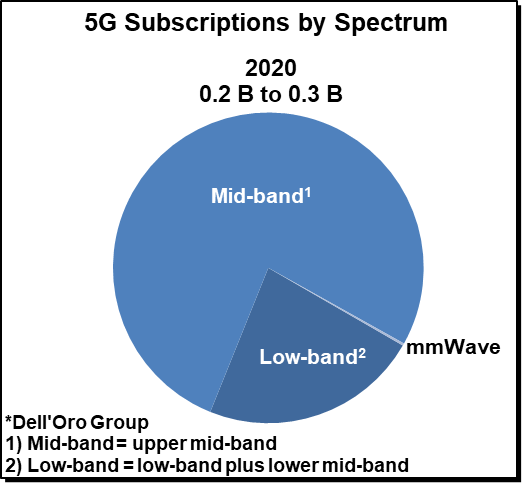

Not surprisingly, Massive MIMO based technologies are powering the vast majority of the 100+ commercial 5G networks. And more than 75% of the projected 0.2 B+ 5G subscriptions by year-end 2020 will likely utilize the upper mid-band.

While Massive MIMO has surprised on the upside when it comes to form factor, weight, performance, cost, and price, one of the key takeaways from the event was that this technology has more room to advance and will continue to play an extremely important role going forward.

Sub 6 GHz enhancements

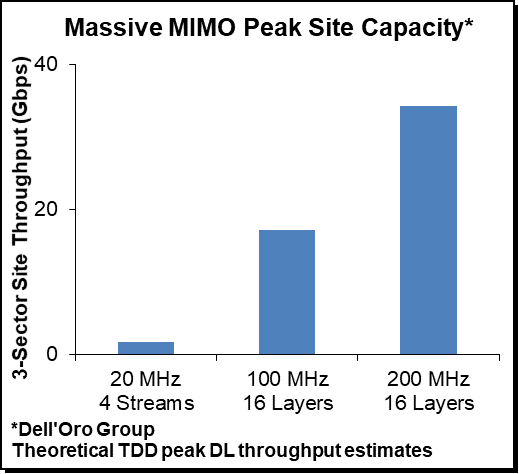

During the event, Huawei discussed the prospects of another potential 2x of cell capacity using its Adaptive High Resolution (AHR) algorithm to enable a premium experience in locations with high user density and interference.

There is indeed something to be excited about. In this scenario, theoretical 3-sector peak capacity would approach 17.1 Gbps if used in conjunction with the AHR (100 MHz of BW, 8 users). This is consistent with Ericsson and T-Mobile’s recent 16-layer MU-MIMO demo with peak cell throughputs of 5.6 Gbps.

More importantly, Huawei also shared data from real deployments, showing that these types of algorithms can improve the performance outside the lab in non-ideal conditions producing around 3.8 Gbps of cell capacity in 100 MHz of bandwidth.

Huawei MBBF 2020

Huawei also signaled some optimism about the FDD Massive MIMO opportunity, announcing the FDD-based 32T32R system, primarily targeting operators with limited upper mid-band spectrum. As a reminder, FDD-based Massive MIMO systems are not new and this concept has been around for some time. However, FDD-based Massive MIMO technologies have not gained the same mass-market acceptance as TDD-based solutions. In addition to the relative efficiency gap between FDD and TDD as a result of leveraging channel reciprocity in TDD systems, FDD-based solutions typically also operate in a lower spectrum band, increasing the physical size of the antennas.

Measuring 0.5 meters in width and weighing around 50 kg, it remains somewhat unclear at this juncture how operators will prioritize FDD-based Massive MIMO in the broader long-term capacity roadmap. Even though preliminary Huawei tests suggest 32T32R can deliver 3x to 4x of capacity growth relative to 4T4R, we expect that FDD Massive MIMO adoption will remain limited for some time and likely be a stronger candidate for mass-market acceptance once operators exhaust the upper mid-band spectrum. At that point, operators can assess what the best tool in the toolkit might be to deliver the next most economical and sizeable capacity boost – FDD Massive MIMO, 6425-7025 MHz, or mmWave.

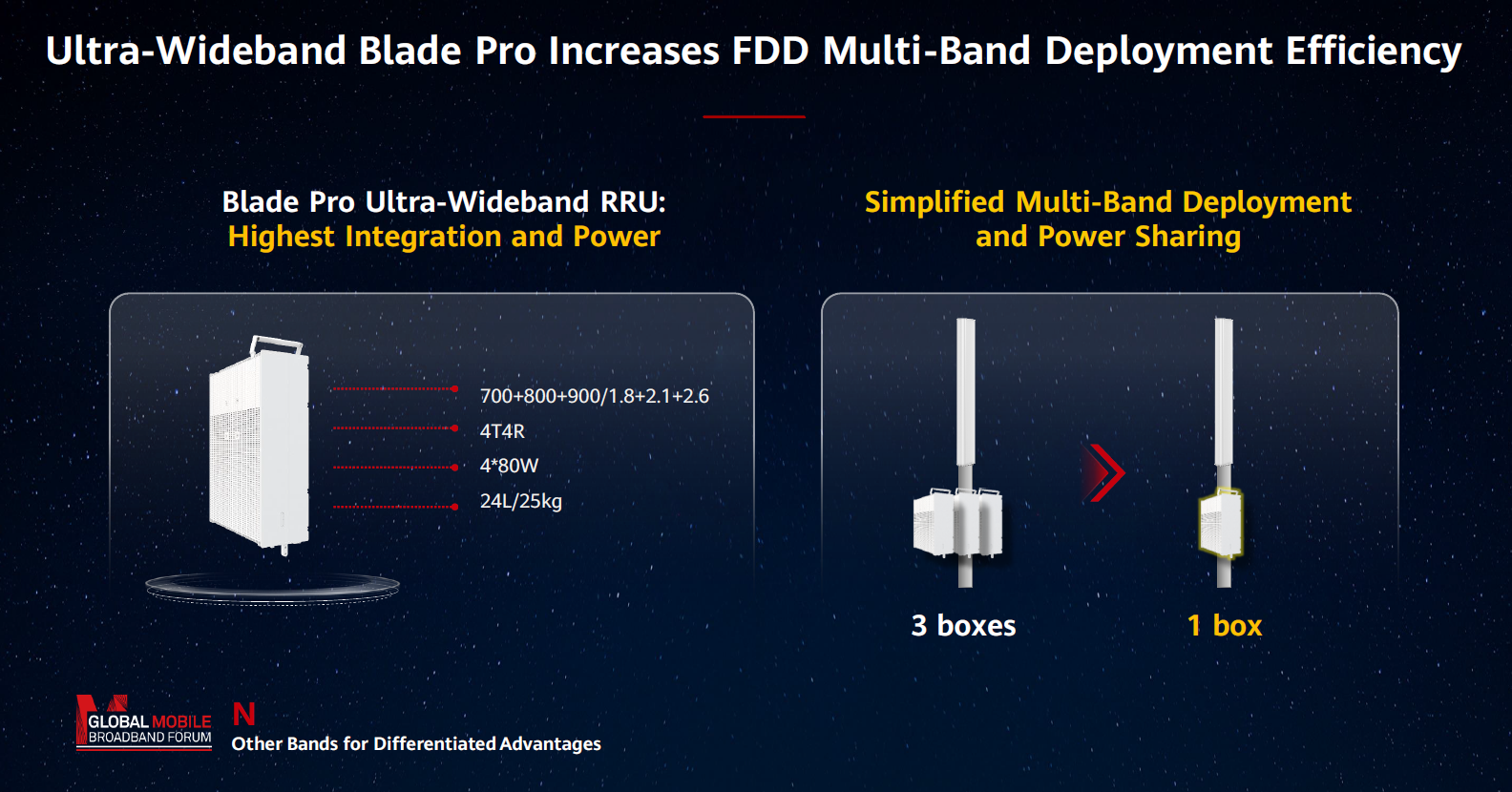

Site simplification

One of the reasons this shift from passive 4G to active antenna based 5G has accelerated at a much faster pace than initially expected is the fact that operators can for the most part leverage their existing macro grid, which has been a major benefit both from a time-to-market and TCO perspective as it reduces the need to add more outdoor sites to realize 5G NR coverage that is equivalent to the outdoor sub 3 GHz LTE coverage. This model of adding new technologies to the existing sites at a faster pace than legacy technologies are sunset will naturally complicate the situation as the sites are becoming increasingly crowded. Although suppliers have invested heavily to address some of the shortcomings at the site with more power-efficient systems and smaller form factors to manage the challenges with adding both Massive MIMO and non-Massive MIMO configured systems, there is more work to be done to support the various frequency and passive/active antenna systems.

During the MBBF event, Huawei announced various RAN enhancements as part of its continuous journey to simplify site deployments including the Blade AAU Pro, which combines a 64T64R 200 MHz Massive MIMO antenna with passive sub 3 GHz band support. As a reminder, Ericsson has its Hybrid AIR antenna system and Nokia and CommScope recently announced they are working on a new hybrid passive/active antenna solution addressing similar site challenges. Huawei is claiming this is the first 64T64R and full sub 3 GHz hybrid unit.

Also, Huawei released its highly integrated Blade Pro portfolio for FDD applications. This portfolio includes the Blade Pro Ultra-Wideband RRU, which reduces the number of required devices at the cell site by integrating three low-band or three intermediate FDD bands into one box, providing operators with more tools to simplify and manage increased site complexity.

Huawei MBBF 2020

In addition to the increased focus on form factor, power consumption, and radio integration, this on-going shift towards multi-technology sites addressing legacy technologies and all the various 5G solutions targeting a wider scope of use cases spanning across potentially multiple industries will also complicate the overall site simplification objective from an operations & maintenance (O&M) perspective. In order for the operators to maintain the performance for 2G-5G consumer networks and simultaneously target capabilities for vertical opportunities while balancing the user experience and optimizing the use of the all the resources to ensure the right KPIs are delivered without breaking the energy or opex budgets, increasing the reliance on more intelligent solutions will be paramount. During the event, Huawei reiterated the importance of introducing more intelligence to simplify the networks and manage the increased complexity without growing opex. AI-assisted autonomous driving of networks will play an increasingly important role to address the challenges O&M poses in the 5G era.

The outlook for vertical 5G is improving

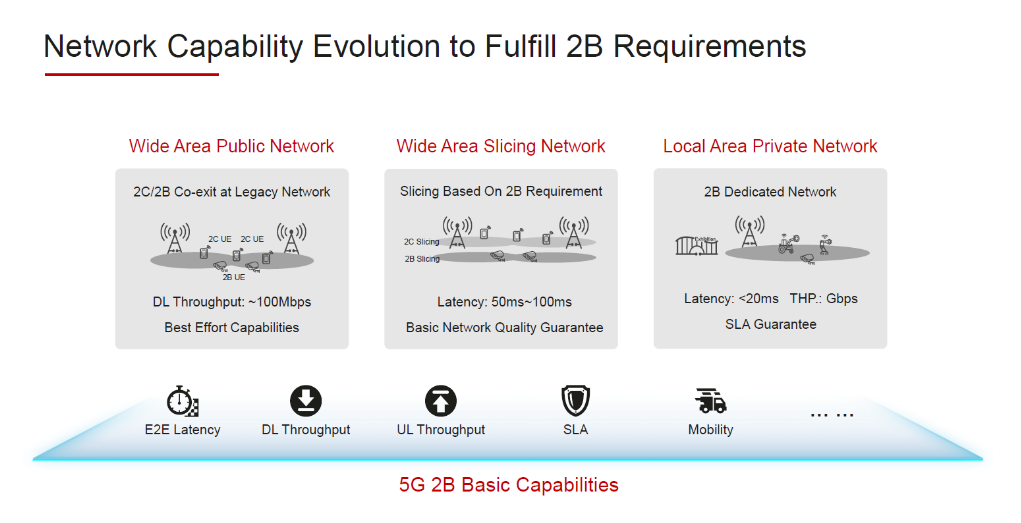

5G eMBB (and FWA) is driving the lion share of the current 5G RAN capex (>99%), still, one of the more exciting takeaways from this event was the progress beyond the eMBB/FWA use cases. At a high level, it is still very early days for private wireless, which is currently dominated by LTE. The private 5G market is even more nascent but with standards ready, 5G and private spectrum becoming available, an ecosystem that is accelerating, and signs of activity picking up pace as new use cases are emerging, there is some optimism that private wireless and 5G NR 2B capex can become more meaningful in the next couple of years.

Huawei’s 2B segmentation is consistent with how the broader industry is now characterizing this market opportunity, consisting of three high-level tiers including the Wide Area Public Network, Wide Area Slicing Network, and Local Area Private Network. Some suppliers are also considering splitting the Wide Area segment into two tiers to capture the various coverage ranges.

Huawei MBBF 2020

What makes the private and 2B markets so exciting is that the opportunities are so vast for both the operators and the suppliers. At the same time, private wireless is different than the traditional public wireless market not only from a technology and standards perspective but also from an ecosystem, go-to-market, and deployment perspective.

Revenues are small relative to overall 5G investments but activity is on the rise. Huawei is engaged in thousands of private 5G projects across China focusing on smart factory, smart port, smart mining, smart utilities, and smart healthcare — consistent with its four-dimensional strategy to move from demo to deployment assessing the opportunity and readiness from a business, technology, standard, and ecosystem perspective. Judging by the proof of concept data shared at this event and progress communicated by other RAN suppliers, the smart factory appears to be emerging as a common theme.

As we have discussed in the 5-year forecasts, it will take time for these non-traditional opportunities to offset declining macro coverage capex post the peak MBB rollout phase. Nonetheless, the progress is promising, bolstering the thesis that the aggregate upside of these smaller opportunities could provide some cushion in the outer part of the forecast period.

The event was also a good reminder that the smaller Open RAN suppliers need to ramp investments to ensure they can deliver simplified and energy-efficient passive/active/hybrid solutions in a competitive form factor that maximizes the use of the sub 6 GHz spectrum.

[wp_tech_share]

We just published the 3Q20 RAN report. Preliminary readings indicate that the positive momentum that has characterized the radio access network (RAN) market since the upswing began in the second half of 2018 extended into the third quarter, with surging demand for 5G propelling the RAN market to robust year-over-year growth, validating the message we have communicated now for some time about the disconnect between the underlying economy and the RAN market in this recession.

In this report, we estimate that the overall 2G to 5G RAN market advanced 10% to 20% Y/Y in the third quarter. With the strong showing in the quarter, the RAN market has now advanced on a year-over-year basis in eight out of the last nine quarters, reflecting positive momentum in multiple markets.

The asynchronous nature of the 5G rollouts in the US, reflecting the FCC’s decision to deemphasize the importance of the mid-band spectrum, has not impacted the overall capex envelope in the US market. On the contrary, this spectrum strategy is pushing the US operators to make the best of the cards they were dealt, and optimize how they allocate the capex between capacity and marketing-driven investments. Following three consecutive years of robust growth in the North America region resulting in a revenue surge of 30% to 40% between 2016 and 2019, the North American RAN market remains on track for a fourth consecutive year of growth.

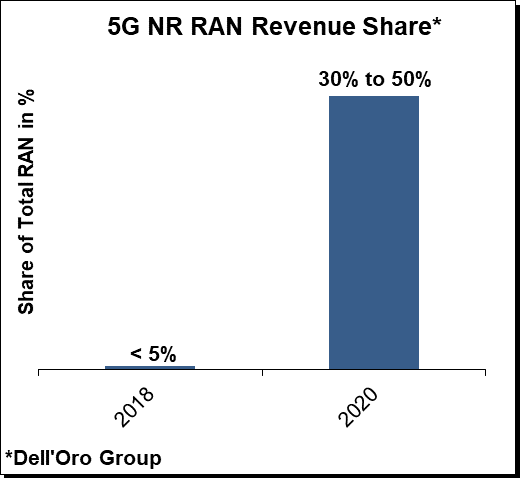

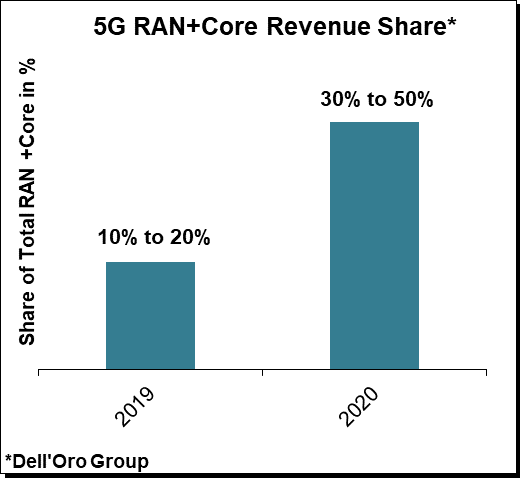

The shift from LTE to 5G NR, low-band and mid-band, continued to accelerate at a torrid pace, with 5G NR revenues more than doubling Y/Y in the first nine months, accounting for 30% to 50% of the RAN market in the quarter. To put this into perspective, it took more than four years for LTE to reach the same revenue share of total RAN.

Initial estimates suggest that vendor rankings remained stable between 2019 and the first three quarters of 2020, while revenue shares were impacted to some degree by the state of the 5G rollouts in China and North America, resulting in share gains for the Chinese suppliers – we estimate that Huawei and ZTE collectively gained approximately 5% points of revenue share between 2019 and 2020 (YTD).

We have adjusted the near-term RAN market outlook upward, to reflect stronger than expected activity in China, Europe, and North America, with total RAN projected to approach $70 B to $80 B for the combined 2020 and 2021 period.

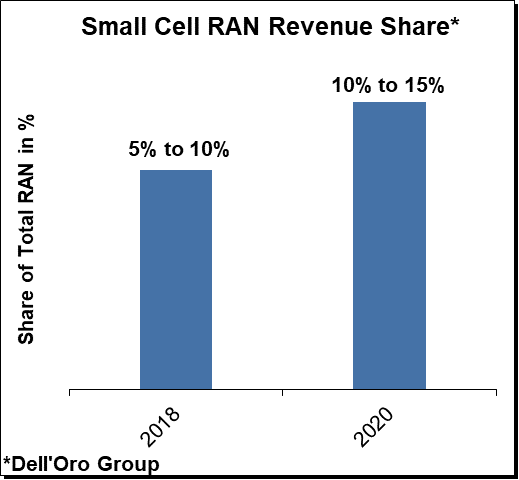

Small cells are expected to continue playing an important role in 2021, approaching 10% to 15% of the overall RAN market. The outlook for mmWave remains favorable, with more than 100 operators investing in the technology.

Open and virtual RAN continues to gain momentum, bolstered by Ericsson now formalizing its support with its Cloud-RAN announcement. The uptake remains mixed. Some suppliers are already shipping O-RAN compatible radios. At the same time, the lion share of any RAN swaps is still going to the traditional RAN players, suggesting the technology remains on track but the smaller players also need to ramp up investments to secure larger brownfield wins.

For more info about the RAN suppliers and the state of 4G, 5G, Massive MIMO, Small Cells, mmWave, CBRS, and Open RAN, please contact dgsales@delloro.com for more info.

[wp_tech_share]

Going into 2020 we outlined ten 5G predictions. Since we now have data for 1H20 and will soon start collecting data for 3Q20, the timing is right for a quick status check on the 5G predictions we outlined going into 2020.

1) 5G RAN+Core Infrastructure Market to More than Double

Prediction: 5G NR continues to accelerate at an extraordinary pace, much faster than expected four or five years ago or even just six or three months ago, underpinned by large-scale deployments in China, Korea, and the US. These trends are expected to extend into 2020. The upside in 5G NR will be more than enough to offset declining LTE investments, propelling the overall RAN (2G-5G) market for a third consecutive year of healthy growth.

Status: This is for the most part playing out as we outlined, though we have adjusted the 5G NR and Core outlook upward to reflect larger than expected deployments in particularly China, which is more than enough to offset LTE capex on pace to decline more than 20% in 2020.

2) Early Adopters to Embrace 5G SA

Prediction: The path toward 5G has become more straightforward since the 2Q19 quarter with only two options now—Option 3 which is 5G NSA, utilizing the EPC, and Option 2 which is 5G SA utilizing the 5G Core. As we move into 2020, we will see the emergence of the first 5G Standalone (5G SA) networks. We expect service providers in China, Korea, the Middle East, and the US to launch 5G SA sometime in 2020.

Status: 5G SA and 5G core is now a reality. According to the2Q20 MCN report, 5G Core revenues accounted for nearly 15% of overall Mobile Core Network Revenues, underpinned by strong developments in the APAC region. “The ramp-up in the second half of 2020 has already begun, with T-Mobile commercially launching its 5G Standalone network in August, recognizing Cisco and Nokia, as their 5GC suppliers,” said Dave Bolan, Dell’Oro 5G Core, and MEC Expert.

3) More than 100 M Transceivers

Prediction: The Massive MIMO business case has changed rather significantly over the past two to three years with the technology now considered to be a foundational building block for mid-band NR deployments. We recently revised the 2020 Massive MIMO outlook upward, driven by surging year-to-date shipments and improved market sentiment for 2020. The overall 5G NR transceiver installed base – Massive MIMO plus Non-Massive MIMO for sub 6 GHz and Millimeter (mmW) macros and small cells – is projected to eclipse 0.1 B by 2020.

Status: Preliminary estimates suggest combined macro and small cell transceiver shipments for non-Massive MIMO and Massive MIMO configured systems was already in the 50 M to 100 M range for the 1H20 period. The forecast remains on track with total transceiver shipments projected to surpass 0.1 B in 2020.

4) Dynamic Spectrum Sharing Takes Off

Prediction: The attitude towards spectrum sharing is on the upswing, with both suppliers and operators discussing their spectrum sharing roadmaps. In addition to the spectral efficiency gains of 15% to 20%, operators are considering the benefits from a marketing perspective. Operators also see the extended 5G NR coverage with a lower band spectrum as a key enabler for 5G SA and network slicing. The technology is expected to play a pivotal role in upgrading existing low-band LTE sites to NR in the year 2020.

Status: Operators are clearly warming up to the idea that the upside with DSS outweighs the downside, with the key benefits including 1) Accelerate nationwide coverage, 2) Spectral efficiency upside comparing NR and LTE, 3) Overall performance upside using CA, and 4) Simplify and accelerate the transition towards 5G SA.

The downside with DSS is that it can impact the net capacity. But at the same time, operators also know that there are only three paths to move from 4G to 5G with the existing LTE spectrum — re-farming, static sharing, and DSS. And unless the goal is to stay on LTE, the reality is that the picture becomes more favorable when comparing DSS with static sharing. According to Ericsson, the relative performance upside with both the LTE and 5G NR traffic when comparing DSS with static sharing at various subscriber penetration rates is material (for a 50% NR penetration, Ericsson estimates the LTE and NR upside could be around 86% and 57%, respectively).

And more importantly, operators are shifting from talking about DSS to deploying the technology. Swisscom and Verizon have already deployed DSS nearly nationwide. AT&T is also using DSS to expand its low-band coverage. Deutsche Telekom said with its 2Q20 update that its low-band 5G network will cover two-thirds of the German population by the end of 2020, relying heavily on DSS.

Ericsson saidearlier in the year that 80% of customers that are testing DSS have plans to deploy the technology over the next year.

5) 5G NR Indoor Small Cell Market to Surpass LTE

Prediction: With more data points suggesting the beamforming gains with Massive MIMO radios delivering comparable outdoor coverage in the C-band relative to 2 GHz LTE deployments, preliminary data from the field also suggests indoor performance will be a challenge and operators are already migrating the indoor capex from 4G to 5G. These trends are expected to intensify in 2020.

Status: We have not made any material changes to the overall outlook and still expect full-year 2020 5G NR indoor revenues to surpass LTE pico investments. While shipments were impacted negatively sequentially between 4Q19 and 1Q20, partly due to COVID-19, market conditions improved significantly during 2Q20 propelling the overall 1H20 indoor 5G NR revenues to advance more than 10x year-over-year.

6) Millimeter Wave (mmW) to Approach 10% of 5G NR Small Cell Installed Base

Prediction: Even though deploying 5G NR in the mid-band using the existing macro grid will deliver the best ROI for some time for operators seeking to optimize cost per GB and average speeds, 5G NR mmW shipments and revenues increased substantially in the third quarter of 2019, with the overall mmW NR market trending ahead of expectations. We recently adjusted our near-term mmW outlook upward to take into consideration the state of the market and improved visibility about the underlying fundamentals in the US, Korea, and Japan.

Status: As we discussed in the recently published 5-year RAN Forecast, the outdoor mmW market has surprised on the upside while the indoor mmW market has taken a bit longer to ramp than we initially expected. Even with the recent upward adjustment for the outdoor segment and downward revisions for the indoor mmW forecast, the total mmW market remains on track to surpass 0.1 M units and is expected to account for 5% to 10% of the overall 5G NR small cell installed base by the end of 2020.

7) 5G MBB to Account for More than 99% of the 5G NR Market

Prediction: We remain optimistic about the IoT upside for Industrial IoT/Industry 4.0, reflecting a confluence of factors including 1) Suppliers are reporting healthy traction with the vertical segments, 2) More countries are exploring how to allocate spectrum for verticals, 3) Ecosystem of industrial devices is proliferating rapidly, and 4) New use cases that require cellular QoS are starting to emerge. At the same time, the LTE platform is expected to suffice for the majority of the near-term vertical requirements implying it is unlikely 5G NR IoT-related capex will move above the noise in 2020.

Status: MBB continues to dominate the 5G capex. LTE IoT is picking up the pace and remains on track to comprise a low-single-digit share of the 2020 LTE RAN market. 5G IoT is moving in the right direction with interesting use cases starting to emerge. But it will take some time before the 5G IoT NR capex will move above the noise. At the same time, we adjusted the overall FWA outlook upward with the recently published 5-Year RAN Forecast, reflecting an improved business case and shifting usage patterns triggered by COVID-19. With this adjustment, we currently estimate 5G MBB remains on track to account for more than 97% of the 5G NR market.

8) Virtual RAN 5G NR Revenues to Exceed Open RAN 5G NR Revenues

Prediction: There are multiple ongoing efforts driven both by operators and suppliers with the primary objective of realizing a more flexible architecture that will optimize TCO for both the known and unknown use cases while at the same time improving the ability for the service providers to differentiate their services. Given the current state of these tracks with the incumbents investing more in virtual solutions and the readiness of Open RAN initiatives for existing 5G MBB deployments, we envision Non-Open RAN Virtual 5G NR revenues will be greater than Open RAN (virtual RAN with open interfaces) 5G NR revenues in 2020.

Status: With Open RAN now developing at a faster pace than initially expected, we might need to revisit this assessment.

9) 5G NR RAN Revenue HHI to Increase > 100 Points

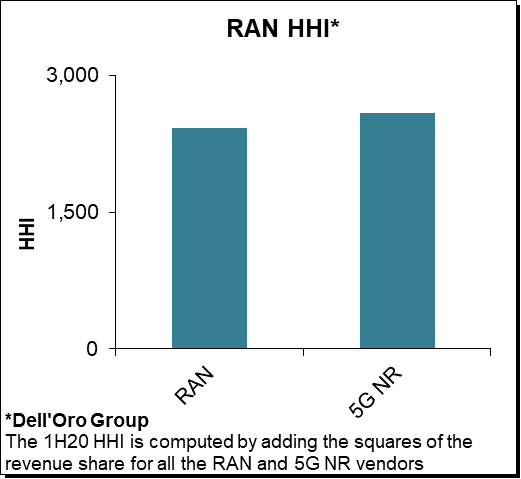

Prediction: Total RAN HHI has been fairly stable over the past three years, reflecting a competitive dynamic that remains fierce, moderately concentrated, and relatively stable. Initial readings suggest the 5G NR HHI for the 4Q18-3Q19 period is trending below the 2018 overall RAN HHI, however, we expect the 5G NR HHI to increase in 2020.

Status: Preliminary estimates suggest the 1H20 5G NR HHI was about 5% to 10% greater than the overall RAN HHI, underpinning projections that large scale 5G NR deployments in China are impacting the 5G RAN landscape.

10) 5G NR Subscriptions to Approach 0.2 B

Prediction: Preliminary estimates suggest the shift from LTE to NR is roughly two to three years faster than the 3G to 4G migration from a RAN infrastructure and subscription adoption perspective. The end-user ecosystem is developing at a rapid pace with multiple chipsets, devices, and phones supporting both NSA and SA for the low, mid-, and mmW spectrum now commercially available. While TDD has dominated mid-band and mmW deployments to date, FDD based 5G NR phones became a reality in 2H19 and will proliferate in 2020. End-user device adoption is projected to accelerate rapidly in 2020, with 5G NR approaching 0.2 B subscriptions, bolstered by healthy NR subscriber adoption in China, Korea, and the US.

Status: According to the GSA, 5G subscriptions approached 138 M in the second quarter. It is possible our 2020 forecast is low with total 5G subscriptions not only approaching but even surpassing 0.2 B this year.

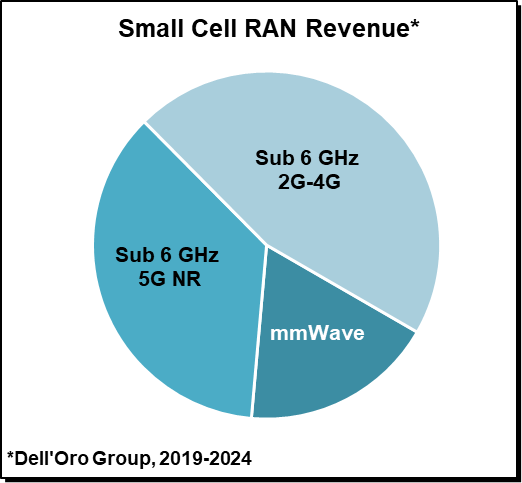

Preliminary estimates suggest the small cell radio access network (RAN) market (excluding residential small cells) approached 1 to 1.5 M units in the first half of 2020, comprising a double-digit share of the overall RAN market. Aggregate small cell growth is tracking slightly below expectations, partly due to logistical challenges associated with the pandemic. At the same time, small cell RAN revenues improved more than 20% Q/Q in the second quarter, adding confidence the bulk of these transitory challenges are now in the past and are unlikely to impact the long-term demand for small cells.

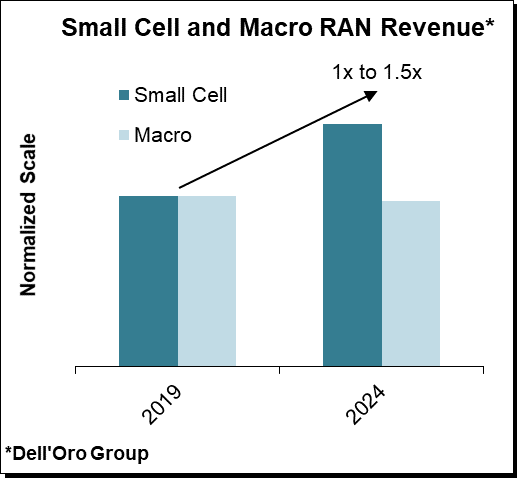

The global growth outlook for small cells remains favorable, underpinning projections the technology will play an increasingly important role supporting the overall RAN network as operators and enterprises navigate new technologies, spectrum bands, and use cases. Cumulative global small cell RAN investments remain on track to approach $25 B over the next five years, advancing at a substantially faster pace than the macro RAN market. Helping to explain this output acceleration is broad-based acceleration across both the indoor and outdoor domains.

The high-level vision has not changed. We expect unlicensed Wi-Fi systems to coexist with cellular technologies. For upper mid-band deployments, operators will need to advance indoor deployments rapidly while the sub 6 GHz micro adoption phase will be more gradual.

Sub 6 GHz small cells, including CBRS, are projected to account for more than 80% of the cumulative small cell market, reflecting the need for operators to complement upper mid-band outdoor deployments with indoor small cells to optimize the combined experience.

Since the last forecast, we have adjusted the cumulative 2019-2024 outdoor micro-small-cell outlook upward, driven primarily by a more favorable outdoor mmWave forecast. With the North American operators leading the way in mmWave, the upward revision is primarily driven by the improved momentum in the Asia Pacific region. In addition to on-going large scale deployments in Japan, the Korean operators are moving forward with plans to deploy mmW for hotspot and smart factory applications. Activity is also picking up in China.

Reflecting back on how we envisioned the market would unfold just a few years back, it is fair at this point to conclude that the outdoor mmWave market has surprised on the upside. At the same time, the indoor mmWave market has disappointed somewhat, reflecting the uncertainty about the timing of this market opportunity. Recent developments with suppliers, including Samsung, announcing the commercial availability of indoor mmWave systems add confidence about future growth prospects.

Preliminary 1H20 estimates suggest the top 5 macro-RAN suppliers accounted for more than 90% of the small cell market. With nearly 30 suppliers planning to support various forms of small cell technologies capitalizing on new opportunities emerging with private wireless, CBRS, Open RAN, and mmWave deployments, it will be interesting to monitor the dynamics between the incumbents and new entrants or small cell suppliers with weaker RAN footprints.

About Dell’Oro Small Cells RAN coverage, please refer to:

Dell’Oro Group’s Quarterly RAN and 5-Year Forecast RAN Reports offer a complete overview of the non-residential small cell RAN market by RF output power (pico and micro) and technology (LTE, 5G NR Sub 6 GHz, 5G NR Millimeter Wave), with tables covering manufacturers’ revenue and unit shipments.

Dell’Oro Group’s CBRS Report offers a complete overview of the CBRS Small Cell RAN market opportunity.

If you want to get a copy of the above report(s), please contact us (dgsales@delloro.com) for more details.