The combination of the faster than expected 5G ramp, positive CBRS momentum, optimism about industrial IoT and private LTE/NR, and the increased focus globally on various spectrum sharing platforms form the basis for the renewed focus on connectivity opportunities in the enterprise.

We recently published the 1H19 Telecom Capex Report. In short, we did not make any material adjustments to the overall capex forecast. With firmer readings about the market developments in the first half of the year, we remain confident that that there are reasons to be optimistic about the underlying demand drivers for both existing and new uses cases. Following three years of declining capex trends between 2015 and 2017 and flat growth in 2018, we forecast global capex to improve at a CAGR of 1% between 2018 and 2021, driven primarily by strong demand for wireless/5G related projects in the Asia Pacific region.

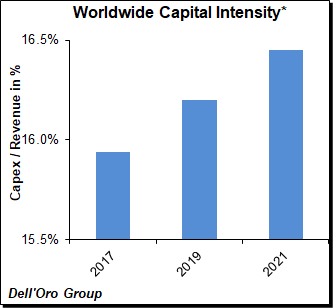

Constrained operator revenue growth is expected to be one of the primary inhibitors of further telco capex acceleration. With currency-adjusted carrier revenues projected to remain relatively stable over the forecast period, strong coupling between revenue and capex growth will ensure that capital intensities remain relatively flat over time. At the same time, the pickup in capex/revenue for the 1H19 period underpinned projections that operators are comfortable with some deviation in the short-term to accommodate the rollout of 5G.

Constrained operator revenue growth is expected to be one of the primary inhibitors of further telco capex acceleration. With currency-adjusted carrier revenues projected to remain relatively stable over the forecast period, strong coupling between revenue and capex growth will ensure that capital intensities remain relatively flat over time. At the same time, the pickup in capex/revenue for the 1H19 period underpinned projections that operators are comfortable with some deviation in the short-term to accommodate the rollout of 5G.

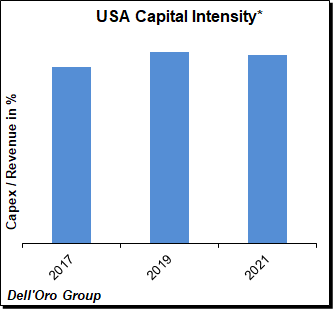

After two consecutive years of robust capex expansion in the U.S., the full year 2019 outlook remains favorable but the investment envelope beyond 2019 will likely be more subdued. The projected capex envelope for the U.S. telecom market assumes mid-band related capex will remain elevated, millimeter wave (mmW) investments will increase, and low-band driven capex will remain flat or decline.

The concept of network sharing is not new. But with operators in Europe and China announcing new passive and  active sharing arrangements, we are fielding more questions than typically for this topic, reflecting a renewed concern an uptick in partnership announcements could impact the RAN market negatively.

active sharing arrangements, we are fielding more questions than typically for this topic, reflecting a renewed concern an uptick in partnership announcements could impact the RAN market negatively.

Our current thesis is that there will be more 5G cycles than 4G cycles and improved efficiencies through sharing agreements will ultimately enable the carriers to address most of the 5G waves without material adjustments to capex/revenue. While operators are comfortable growing the capex/revenue ratio slightly in the short-term, they are also fully aware of the demand side challenges and have no plans to return to historical capital intensity ratios.

In other words, we don’t expect any significant near-term capex cuts as a result of these engagements and instead view sharing partnerships as an opportunity for the operators to deploy broader and deeper 5G networks addressing many of the 5G opportunities with constrained budgets at a much faster pace relative to the base case of deploying 5G independently. And with non-equipment related capex and opex comprising the majority of the cell site TCO (RAN ~15%), the improved utilization will likely have the greatest impact on non-equipment related investments.

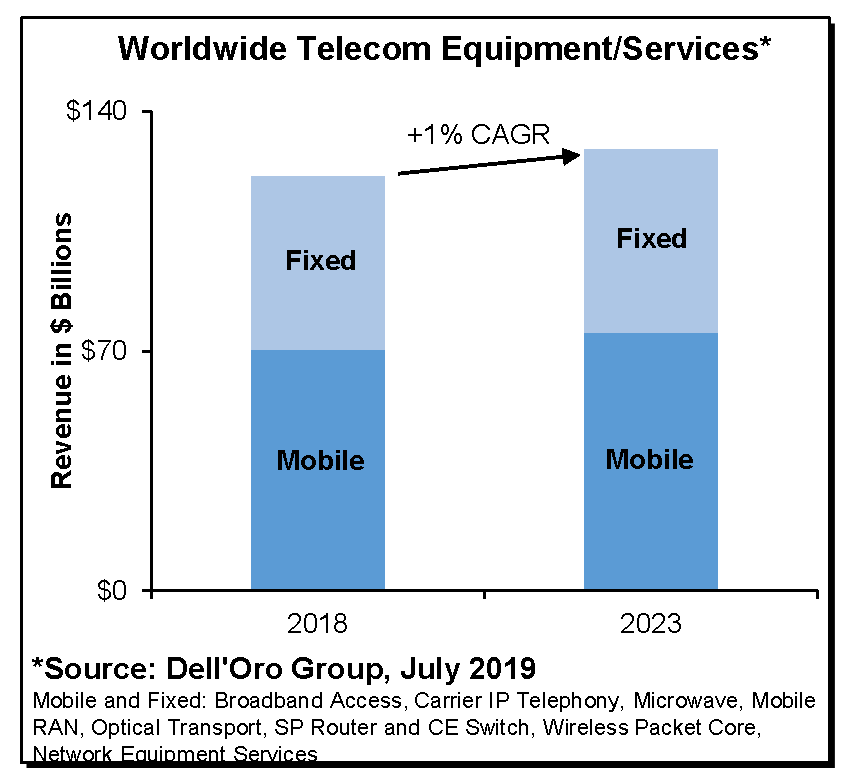

The overall telecom equipment and services market is projected to grow at a 1% CAGR

We just wrapped up the July 2019 5-year Forecasts for all the Telecommunications Infrastructure and Services programs covered at the Dell’Oro Group.

In this forecast, the overall telecom equipment and services market is projected to grow at a 1% CAGR, approaching $129 B by 2023, up from $121 B in 2018. Helping to drive this growth is fairly synchronized growth projections within the application mix, with mobile and fixed revenue projected to both grow at a 1% CAGR over the forecast period.

Additional key takeaways from the reporting period include:

- In order to cope with mobile data traffic that continues to grow at an unabated pace and flattish revenue trends, operators are balancing their investments carefully between the supply side related challenges and the opportunities from a demand perspective. The need to reduce TCO has been a catalyst for the overall 4G to 5G migration acceleration, benefitting not only RAN equipment but also the demand for core, transport, and services.

- Total Transport Market – including Microwave and Optical – is projected to grow at a 3% CAGR.

- The demand for Mobile Backhaul is projected to grow at a 3% CAGR while the overall RAN market is projected to grow at a 2% CAGR, over the forecast period.

- Overall 5G infrastructure projections – including 5G RAN and 5G Core – were revised upward, reflecting a more optimistic view about the 5G Core market.

- The adoption of 400 GE will help to advance the SP Router market and offset flat growth expectations for Broadband Access.

- Following five years of contractions, Network Equipment Services revenue growth is expected to improve, buoyed by improving market sentiment for telecom equipment. Total Network Equipment Services revenue – including Managed Service, Network Rollout Service, and Consulting Service – is projected to grow at a low-single digit growth rate over the forecast period.

Dell’Oro Group telecommunication infrastructure research programs consist of the following: Broadband Access, Carrier IP Telephony, Microwave Transmission & Mobile Backhaul, Mobile Radio Access Network (RAN), Optical Transport, Service Provider (SP) Router & Carrier Ethernet Switch, Telecom Capex, Wide Area IoT, and Wireless Packet Core.

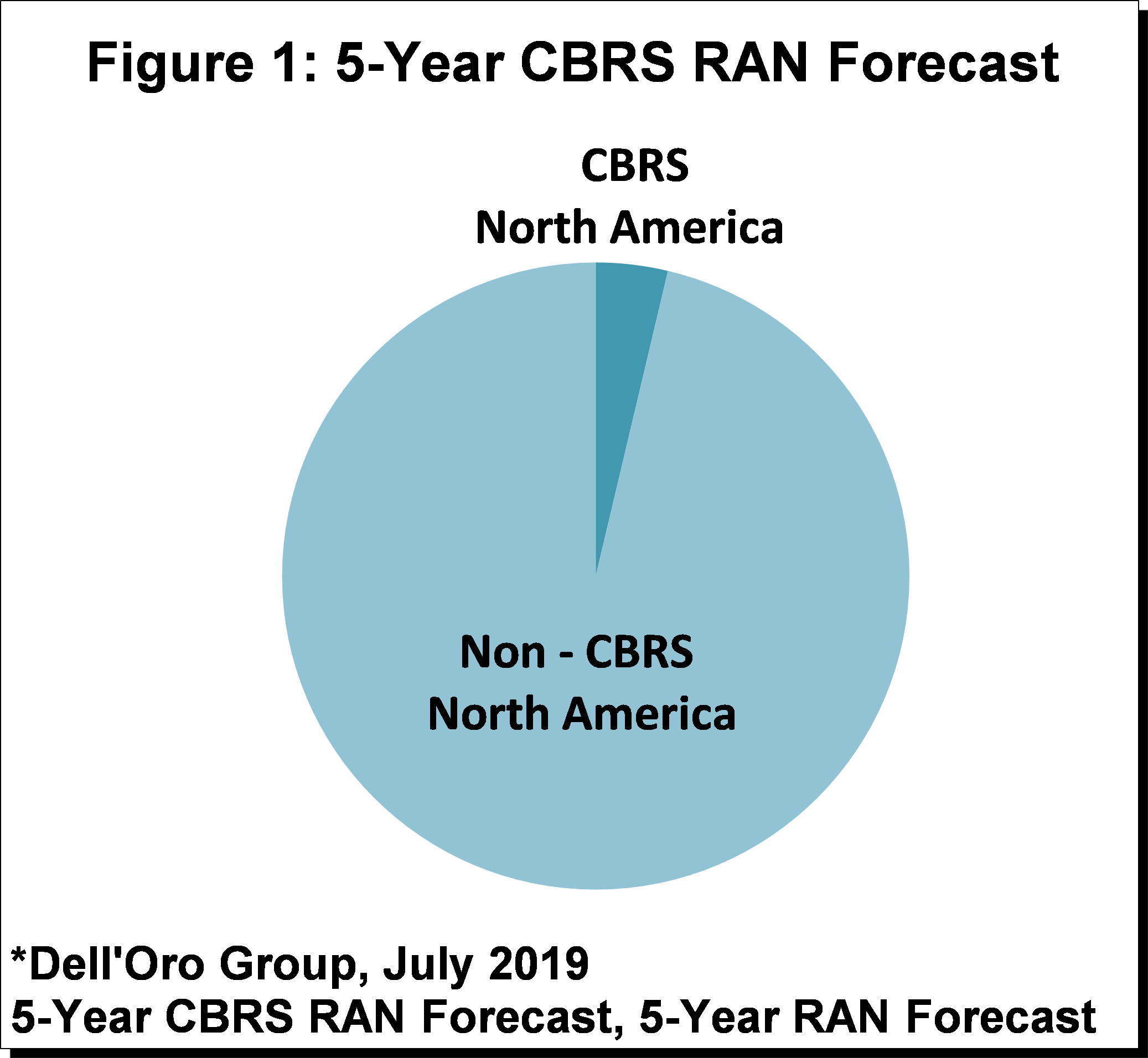

The latest Dell’Oro Group CBRS RAN 5-year forecast suggest short term delays and renewed concerns about the network economics for outdoor deployment will not  impact the long-term demand for LTE and 5G NR CBRS solutions – the overall CBRS RAN market outlook is relatively unchanged since the January 2019 update. The overall CBRS market is expected to grow at a rapid pace between 2019 and 2023 with cumulative RAN investments projected to comprise a tangible share of the overall North America RAN market (Figure 1).

impact the long-term demand for LTE and 5G NR CBRS solutions – the overall CBRS RAN market outlook is relatively unchanged since the January 2019 update. The overall CBRS market is expected to grow at a rapid pace between 2019 and 2023 with cumulative RAN investments projected to comprise a tangible share of the overall North America RAN market (Figure 1).

“There is a fine line between pleasing everyone and no one. And even with more questions raised about the outdoor CBRS TCO, our underlying position has not changed–we remain excited about the CBRS opportunity and continue to believe that the majority will benefit resulting in material CBRS investments over the next five years”, said Stefan Pongratz, Senior Research Director for RAN and Telecom Capex with the Dell’Oro Group.

Other highlights from the CBRS 5-Year Forecast Report:

- CBRS capex is not projected to have a significant impact on the WLAN capex.

- CBRS investments are projected to account for a mid-single-digit share of the overall North America RAN market.

- FWA is projected to drive the lion share of the CBRS capex over the near-term.

Dell’Oro Group’s Advanced Research: Citizen Broadband Radio Service (CBRS) Report offers an overview of the CBRS RAN potential with a 5-year forecast for indoor and outdoor LTE and 5G NR CBRS deployments along with a discussion on the participating suppliers. To purchase these reports, please contact us by email at dgsales@delloro.com.

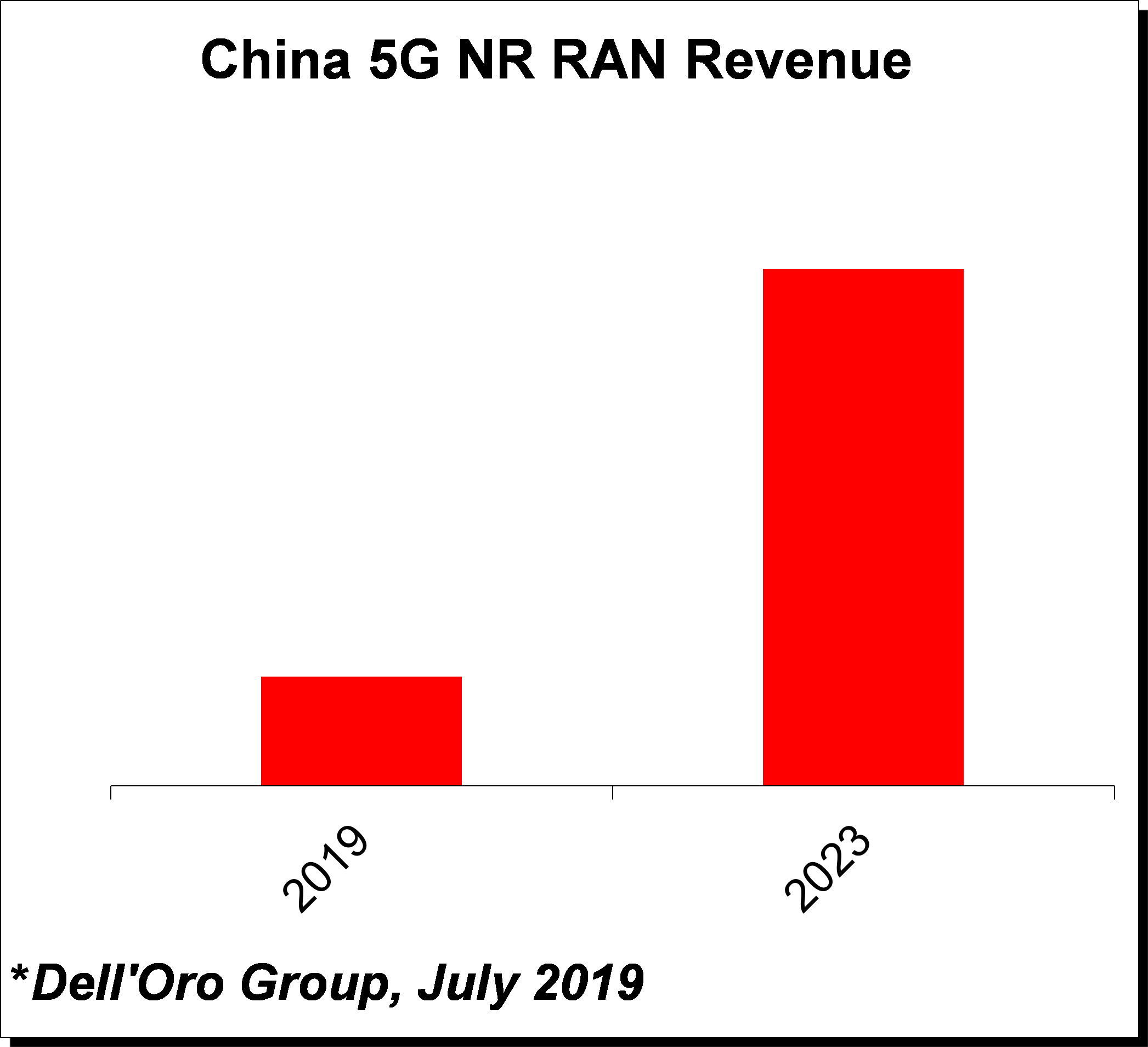

China’s 5G RAN Market to Advance Fivefold

The latest Dell’Oro Group Mobile RAN 5-Year July Forecast Report indicates that the investment recovery in China that  began in the second half of 2018 is expected to extend over the forecast period, propelling China’s 5G RAN market to advance nearly fivefold relative to an already-aggressive 2019 baseline.

began in the second half of 2018 is expected to extend over the forecast period, propelling China’s 5G RAN market to advance nearly fivefold relative to an already-aggressive 2019 baseline.

“While there is still some uncertainty about the 5G NR business case driven by new revenue opportunities, the momentum for 5G NR eMBB is developing at a broader and faster pace than originally anticipated,” said Stefan Pongratz, Senior Director with the Dell’Oro Group. “With data traffic projected to grow 3 to 4 times over the forecast period, no one is asking any more whether there is a business case for using more spectrum and utilizing it more efficiently,” continued Pongratz.

Other highlights from the Mobile RAN 5-Year July Forecast Report:

- China is expected to dominate the 5G capex envelope – cumulative investments projected to be more than twice the size of North America’s 5G RAN investments over the forecast period.

- The shift from conventional antenna systems towards Massive MIMO is accelerating – operators are on track to deploy nearly 400 M transceivers over the forecast period.

- The small cell outlook has been adjusted upward to reflect stronger than expected demand for indoor Sub 6 GHz small cells – total small cell RAN market forecasted to nearly double over the forecast period.

Dell’Oro Group’s Mobile RAN 5-Year Forecast Report offers a complete overview of the RAN industry, with tables covering manufacturers’ revenue, transceivers or RF carrier shipments, and base transceiver stations for 5G NR, 5G NR Sub 6 GHz, 5G NR mmW, LTE, LTE FDD, LTE TDD, WCDMA, GSM, CDMA, and WiMAX. The report also includes regional analysis and splits for macro cells, small cells, and Massive MIMO. For more information about the report, please click here.

# # #