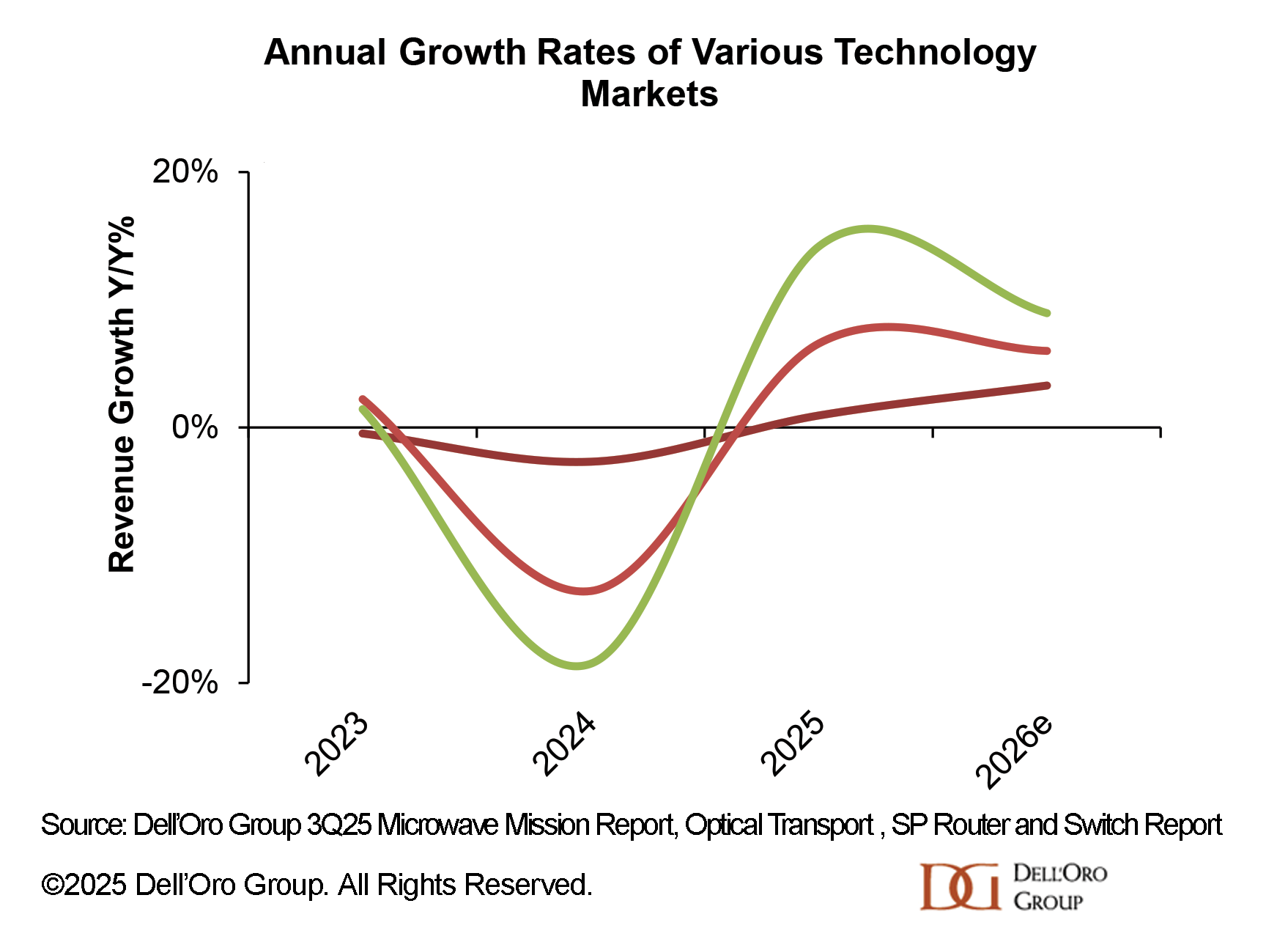

The Microwave Transmission market has gone through some ups and downs, but at a high level, it has been relatively stable and less volatile than the other network equipment markets I track.

Past: 2024

For the full year 2024, the Microwave Transmission market declined by only 3%. While this was a decline, it was minor compared to the double-digit declines in the other markets, where customers pulled back new orders as they digested the excess equipment purchased during the pandemic. In fact, the Microwave Transmission market decline in 2024 was slightly better than we anticipated at the start of the year. The reasons for the market contraction were as follows:

Sharp decline in E-band equipment purchases in India, following a massive deployment cycle the previous year.

Procurement delays and order flow disruptions that followed the acquisition of Siklu and NEC’s microwave business (Ceragon acquired Siklu, and Aviat acquired NEC’s microwave business).

Slowdown in rolling out 5G networks as operators began to question its return on investment (ROI).

Weaker macroeconomic conditions, including:

slower GDP growth in many countries

lower currency exchange rates against the U.S. dollar, and

higher borrowing costs.

Present: 2025

We just concluded data collection through 3Q25, and so far, the Microwave Transmission market is poised to post a very small increase driven by sales in emerging markets and a stable North American market. However, within the year, things were rocky: strong growth in the first half was followed by weakness in the second half, leading us to reevaluate the year repeatedly.

Two things are helping the market this year:

Mobile backhaul deployments in emerging markets are increasing. Although many operators are cautious about the ROI, they are still deploying 5G and mobile backhaul, albeit at a slower, steadier pace.

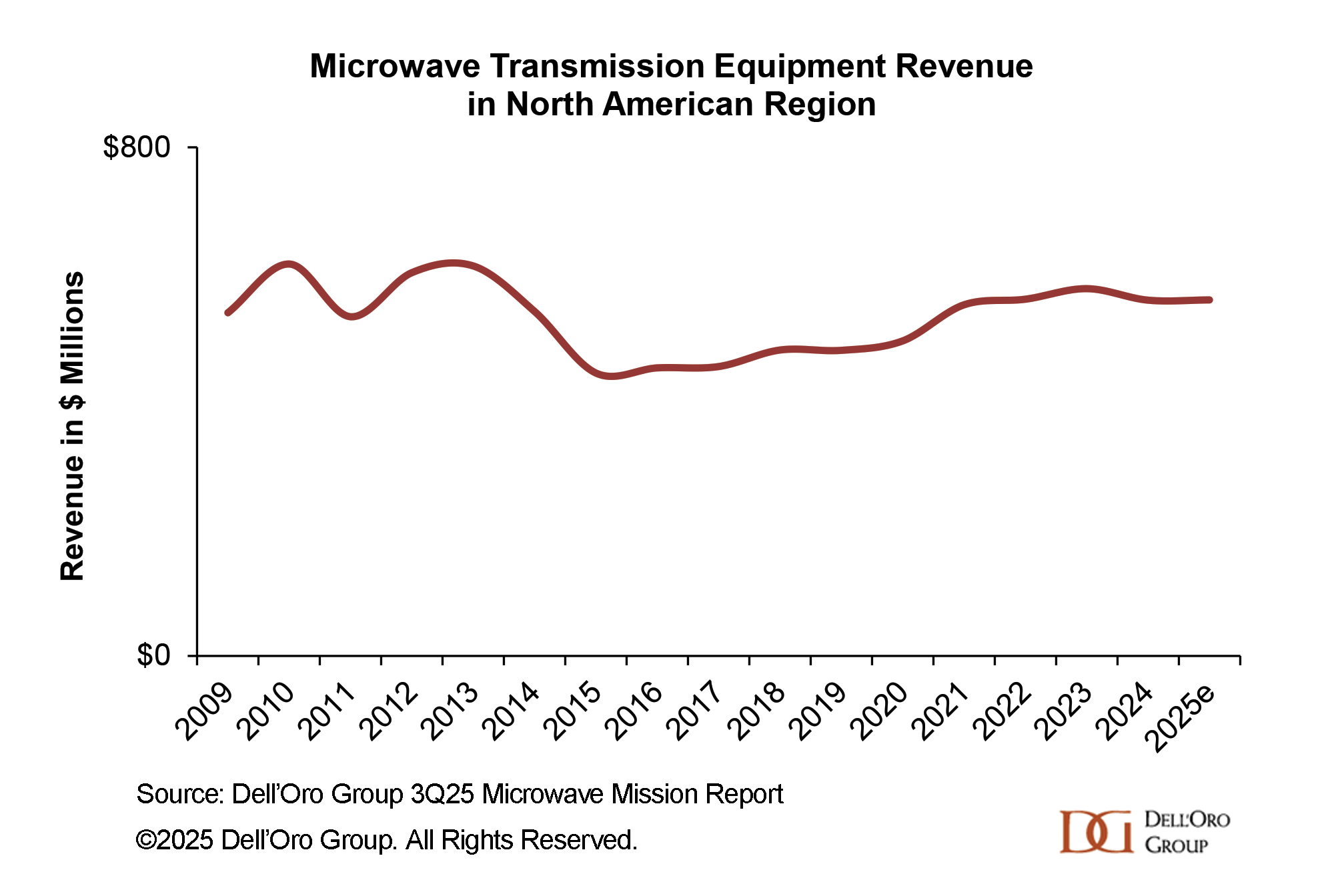

A stable level of demand in North America, which I had always thought would decline. It is actually one of the most fascinating things for me. I have tracked Microwave at Dell’Oro Group since 2008, and everyone (myself included) thought the revenue in this region would shrink with the shift to fiber. This chart shows the microwave revenue in North America between 2009 and 2025. I think the past 15 years have proved us all wrong about North America and that microwave backhaul use would decline.

Unfortunately, offsetting this growth is the weaker Verticals market, which we think is due to lower government funding and delays in project starts.

Future: 2026

We envision the Microwave Transmission market returning to a more normal state in 2026, driven by growth in both mobile backhaul and the Vertical markets.

One major assumption is that we expect demand for mobile network capacity to return to high double-digit growth rates. The demand for bandwidth slowed due to the pandemic, the shift to remote work, weak economic conditions, and reduced travel. However, this all reversed, and we expect network demand to revert to historical growth rates as the world pushes for normalcy. Additionally, integrating AI applications like ChatGPT on mobile devices may increase network usage more than before.

The Microwave Transmission market will not have the high growth rates of the other markets I track, but it won’t have the steep declines either. It is expected to have steady growth in 2026. Operators, especially those in emerging markets still expanding their 5G footprint, are expected to continue adding new cell sites and capacity to their backhaul networks for a few more years. We also believe the Vertical markets may return to growth in 2026, helped a little by rural broadband expansion, which is economically more feasible with wireless links that do not require months of trench digging to bury fiber.

[wp_tech_share]

The signals are confusing. AI boom, global trade war, supply shortages, competitors merging––it takes focus and lots of analysis to cut through the upheaval in the Local Area Networking market and predict the future trends. Luckily, we have decades of historical data and some finely tuned models to enable us to make these top three predictions for the enterprise networking market in 2026.

1. Wi-Fi 7 will dominate enterprise wireless connectivity

For some enterprises, the pristine 6 GHz band will be too alluring to resist. Other organizations will be nearing the end of their WLAN equipment’s lifecycle and, seeing a growing number of Wi-Fi 7- capable devices in their ecosystem, will want to future-proof the network. Yet others may be in the midst of a massive digital transformation project, needing the best quality WLAN to carry steady streams of data feeding their digital operations.

Whereas private 5G deployments will also grow, we expect enterprise adoption of private cellular to remain constrained to a niche, high-end portion of the market. Only especially difficult radio conditions, or very tight security and performance requirements, will justify the additional cost and complexity of private cellular. We don’t expect much cannibalization of private cellular gobbling up the WLAN market either. Enterprises that choose private cellular for their operations are focusing on new use cases and will continue to deploy WLAN as well.

There’s no doubt: enterprise-class Wi-Fi 7 will become mainstream in 2026. With no second, enhanced version (like Wi-Fi 5 Wave 2, or Wi-Fi 6E) to dilute the take up, we expect the Wi-Fi 7 adoption curve to become steeper than it was for any other enterprise WLAN technology.

2. The AIOps business case will prove itself in

AI FOMO is rampant. Enterprises see so much potential with AI, but there are associated risks, and it can be difficult to extract tangible benefits. However, many enterprises have already witnessed dramatic results from using Machine Learning to ease the burden of IT Operations; including shorter deployment times, a dramatic drop in the number of trouble tickets, and faster time to problem resolution. Layering in AI capabilities makes LAN management applications easier to use and more accessible across an organization.

AIOps platforms are available from most of the major enterprise IT vendors. AI and Machine Learning capabilities often have license fees that are recurring in nature, driving up enterprises’ LAN equipment costs. This premium may have dissuaded enterprises from adopting AIOps in the past.

However, over the past few years, vendors have added features and increased the value of those licenses, including 24×7 support bundled into the recurring fee. Now, by paying the equivalent of a fraction of a network engineer’s salary in license fees, a mid-sized enterprise can reduce hours spent on operations and level-one support in order to allocate more of their valuable networking experts’ time to AI projects.

Every enterprise’s business case will be different, but with networking expertise in high demand, we predict that in 2026, the labor savings will outweigh the additional license costs for the majority of mid-to-large sized enterprises.

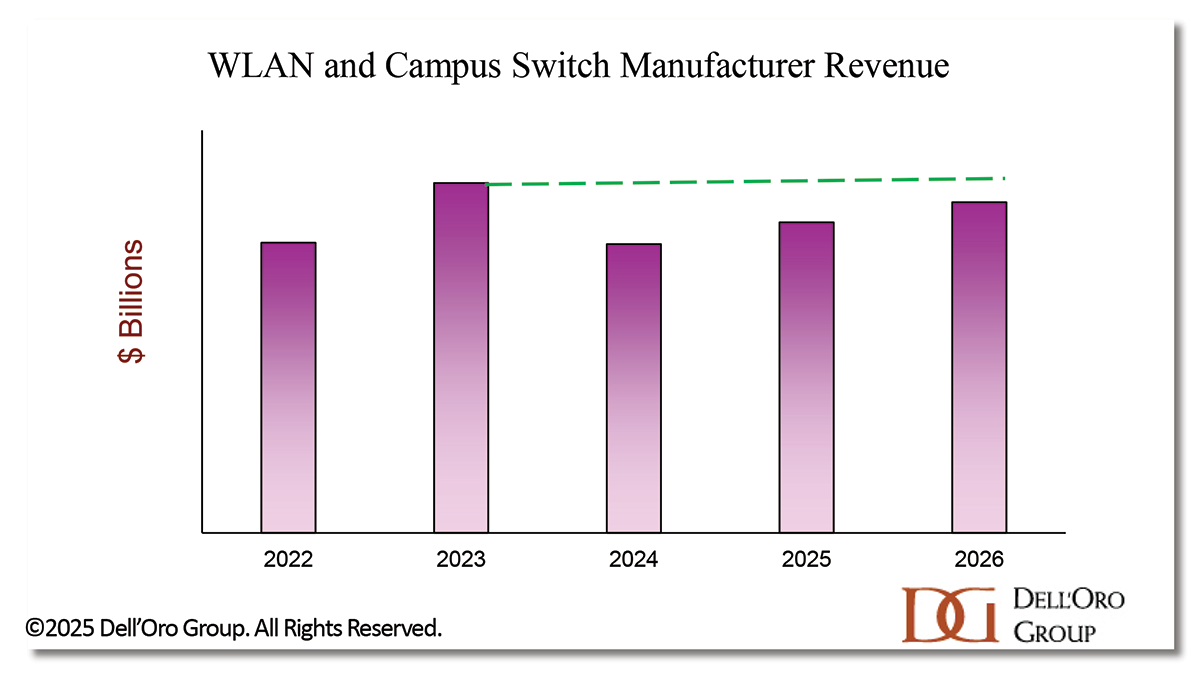

3. 2026 Local Area Networking market will beat $30 B––but still not surpass 2023

The pandemic may seem far away, but the ripple effects are still being felt. After surviving the supply constraints of 2021 and 2022, vendors unleashed a tsunami of WLAN APs and campus switches into the market in 2023, making it the top grossing year of all time for LAN equipment revenue. Following the high volume of shipments, enterprises took time to work through the excess inventory, causing double-digit revenue declines for vendors in 2024. In 2025, the demand-driven market returned, but so has the specter of supply constraints. The AI buildout has caused a shortage of semiconductor components, the most immediate being memory.

The high WLAN and campus switch prices of 2022 and 2023 began to erode in early 2025, but in 4Q25, LAN equipment vendors raised prices to compensate for escalating component costs. Higher prices can dampen demand; however, the need to replace ageing infrastructure will be a counterweight. Enterprises must invest in their LANs in order to modernize their operations, and an upgrade to Wi-Fi 7 requires more switching power and higher bandwidth ports. Weighing the puts and takes, we believe the market will continue to grow in 2026, with vendors applying what they learned during the last supply crunch to avoid the worst in this one. The 2026 market will be well into the $30 B range, but we will need to wait one more year for revenues to beat the highs of 2023. Tune back in at the end of 2026 for more on that prediction.

[wp_tech_share]

Over the past several years, we have watched security spend migrate from hardware appliances toward cloud-delivered and subscription models. In this blog, I outline three predictions for 2026 that describe how that pattern solidifies into a durable template: security budgets increasingly split between cloud-delivered security services at the edge and an AI-infused, centralized SecOps layer that looks a lot like “next-gen SIEM.”

On the edge, SASE/Security Service Edge (Secure Access Service Edge/SSE) and cloud Web Application Firewalls (WAFs) become the default way to protect users and applications. In the middle, distributed cloud networking quietly supplies the connective tissue. At the center, next-generation Security Information and Event Management (SIEM) platforms fuse SIEM, Security Orchestration, Automation, and Response (SOAR), Extended Detection and Response (XDR), observability, and Cloud-Native Application Protection Platform (CNAPP)-style cloud visibility into a single, service-delivered control surface.

Prediction 1 – Edge security spend consolidates around SASE/SSE and cloud WAF

From a budget perspective, the branch and user edge is already moving decisively toward as-a-service delivery. SASE, particularly the SSE half of that equation, has been growing at a solid double-digit rate, while legacy access routing and on-premises secure web gateways have been shrinking. WAF has also emerged as one of the most dynamic parts of the network security landscape as more applications and APIs are exposed directly to the Internet.

Put simply, enterprises are standardizing around two cloud-delivered edge controls:

SASE/SSE for user and branch access, combining secure web gateway, CASB, ZTNA, and firewall-as-a-service capabilities delivered through globally distributed points of presence.

Cloud WAF for Internet-facing web and API traffic as part of secure application delivery platforms.

The immediate drivers are familiar: hybrid work, SaaS adoption, and a steady shift away from private WAN circuits and appliance-based security toward Internet-centric architectures. However, there is also a deeper architectural undertow. Underneath SSE and cloud WAF, distributed cloud networking and early WAN-as-a-service offerings are emerging to connect branches, clouds, and security service edges over a programmable fabric rather than static routers.

In 2026, we expect security and networking teams to budget less for discrete “boxes” at the branch and more for recurring spend on SASE/SSE, WAF, and the underlying cloud connectivity. Physical access routers and appliance SWGs will continue to shrink as a share of branch networking and security spend, reinforcing that the edge is now a service, not a rack of gear.

Prediction 2 – “Next‑gen SIEM” becomes the gravitational center of SecOps

If SASE/ SSE and WAF are where packets are inspected, next-gen SIEM is where evidence is assembled and acted upon. We use “next‑gen SIEM” here as a SecOps solution construct, not a product SKU. In this view, a next-gen SIEM is a SecOps solution that combines:

Classic SIEM for log and event aggregation.

SOAR or extended orchestration, automation, and response (XOAR) for workflow and playbook automation.

XDR for cross‑control point detection and response.

Observability and digital experience monitoring (DEM) for performance and user‑experience telemetry.

CNAPP for configuration, identity, and cloud workload context.

A reflection of enterprises’ pivot in this direction is the recent explosive growth of the CNAPP market. In our analysis, the CNAPP market grew nearly 40% in 2024. Cloud-native security tool consolidation, end-to-end coverage, and DevSecOps integration are the core buying drivers.

Architecturally, next-gen SIEMS are a response to the collision of two worlds:

Traditional SecOps built around monolithic apps, north-south traffic, and data center-centric logging.

Modern app environments built on containers, microservices, and hybrid cloud

In 2026, we expect more RFPs to converge on this next-gen SIEM pattern. Buyers will look for a single SaaS platform that can ingest logs, telemetry, and cloud data; power AI-assisted investigations; and orchestrate responses across SASE/SSE, WAF, endpoint, and on-premises and cloud controls.

Prediction 3 – Security budgeting finishes its shift from capex to opex

The common thread between cloud-delivered edge controls and next-gen SIEM is not just architecture—it is the commercial model. Both are overwhelmingly sold as subscription services.

Across SASE, CNAPP, and broader network security, vendors are leaning into subscription licensing because it lets them monetize more features, deliver updates continuously, and smooth revenue over time. Our forecasts assume a continued shift from perpetual licenses and hardware-heavy deals toward SaaS and virtual consumption, with subscription models explicitly called out as a structural assumption for both network security and distributed cloud networking.

For CIOs and CISOs, this shows up in the budget spreadsheet as:

Smaller, more targeted hardware refresh projects.

Growing multi-year SaaS commitments for SASE/SSE, WAF, CNAPP, and next-gen SIEM.

Increased financial scrutiny of overlapping subscriptions, driving consolidation toward integrated platforms (for example, single-vendor SASE or a single primary analytics plane for SecOps).

We believe 2026 is the year this shift becomes the default assumption rather than a trend to watch. New initiatives will start life in opex, and capex-heavy proposals will increasingly be the exception that must be justified.

Net‑net for 2026

Security budgets will increasingly organize around two SaaS pillars—cloud-delivered security at the edge (SASE/SSE and WAF) and a centralized, AI-infused next-gen SIEM that absorbs CNAPP and traditional SecOps functions. Everything else, from distributed cloud networking to legacy appliances, will be evaluated on how well it supports or can be subsumed into those two spend templates.

[wp_tech_share]

A year of continuous shifts within the sector — and familiar debates beyond it

As we close out 2025, the milestones of the past twelve months underscore just how quickly the industry is shifting beneath our feet. DeepSeek’s breakthrough reshaped assumptions about compute efficiency and cost; NVIDIA’s announcement of Blackwell Ultra signaled yet another leap in accelerator performance; the White House’s AI Action Plan formalized the policy stakes around national compute capacity; Stargate’s Abilene facility began operating at unprecedented scale, becoming a symbol of the AI‑era mega‑campus; debates around AI circular investments highlighted both the ambition and fragility of capital flows into frontier infrastructure — only to name a few of key milestones of this past year

These developments set the stage for a year that will balance continuity with disruption. For vendors and operators, 2026 will bring meaningful shifts in technologies, architectures, and competitive dynamics. Yet from the outside, the narrative may feel familiar. The same themes that began surfacing more prominently in recent years — and defined public debate throughout 2025 — will continue to dominate headlines, even as the underlying infrastructure evolves at a far faster pace.

What we’re not predicting — because everyone else already is

Power scarcity remains the defining constraint, with power availability continuing to be the single most important determinant of site selection for data center projects. Speculation about an AI‑driven investment bubble is expected to intensify, as trillions of dollars in critical infrastructure are deployed amid lingering uncertainty about long‑term monetization models. And public visibility of the sector will keep rising, bringing sharper community pushback, permitting resistance, and societal concerns ranging from energy affordability to the impact of AI on jobs, as well as growing scrutiny over the safe and responsible use of AI, particularly among young people — pressures that intensify most as the industry lacks coherent, accessible, and positive messaging about its value to communities and the broader economy.

Because these forces are so obvious and so deeply embedded in the industry’s trajectory, we will not include them among our predictions. Instead, this outlook focuses on the emerging dynamics that will shape vendors, operators, and the broader ecosystem in ways both expected and unexpected.

The easy ones: our highest-confidence expectations for 2026

These trends are already well underway, with early signals evident throughout 2025, reinforcing a trajectory that leaves little doubt about their momentum heading into 2026.

1. Consolidation and partnerships accelerate

The complexity of gigawatt‑scale data centers is pushing vendors to work together more closely, driving a surge in strategic partnerships that combine expertise across power, cooling, controls, and integration. Expect more joint reference architectures, co‑engineered solutions, and collaborative designs that extend well beyond any single vendor’s historical domain. We anticipate at least ten additional partnership announcements in 2026 as vendors align to meet the growing demands of AI‑era infrastructure.

In parallel, consolidation will continue as vendors with differentiated capabilities become acquisition targets — particularly in high-priority areas such as liquid cooling, solid-state power electronics, and global design and service expertise. These acquisitions will further accelerate the shift toward full-stack delivery models, with integrated chip-to-rack, rack-to-row, and row-to-hall solutions becoming a defining competitive strategy. We expect no fewer than five acquisitions or take-private transactions crossing the $1 billion threshold, underscoring the intensifying race to secure critical capabilities across the DCPI stack.

2. Real builds matter more than bold visions (and vanished ones)

Multi‑billion‑dollar and multi‑gigawatt campus announcements might continue to dominate headlines, but the center of gravity will shift toward execution rather than ideation. Operators will focus on translating these bold visions into reality — securing power, navigating permitting, sequencing construction, and commissioning facilities on time.

With the running backlog of public announcements now exceeding 70 GW of stated capacity, a meaningful share of these projects is likely to remain “braggerwatts” — aspirational declarations that never progress past land options, concept designs, or early‑stage filings. As economic, regulatory, and power‑availability constraints sharpen, attention will shift back to credible projects with clear pathways to completion and well‑defined delivery plans.

Today, several sites are on trajectories that suggest they could eventually cross the fabled 1 GW capacity threshold, but none have reached that milestone yet. By the end of 2026, however, we expect at least five sites worldwide to surpass 1 GW of operational capacity.

3. Divergence grows before convergence returns

Despite efforts toward convergence, 2026 is likely to bring even greater architectural divergence across power and cooling, a proliferation of design pathways rather than a narrowing of them. This is being fueled by rapid technological shifts that show no signs of slowing.

On the power side, even as clarity improves around 400 Vdc and 800 Vdc rack architectures, vendors will diversify rather than narrow their portfolios — developing new families of DC circuit breakers, power shelves, hybrid and supercapacitor‑based energy storage, and MV switchgear integrated with solid-state electronics in preparation for deployments expected in 2028/29.

Cooling will see similar diversification. A testing ground of novel technologies — including two‑phase direct liquid cooling (DLC), CDU‑less single‑phase DLC, and a wide variety of cold‑plate architectures — is expected to gain momentum, expanding the solution diversity of the ecosystem.

In this environment, initiatives like the Open Compute Project (and its collaborations with ASHRAE, Current/OS, and others) will become even more important in steering the industry, offering reference frameworks and shared direction to help channel innovation while reducing unnecessary fragmentation.

Watch closely: trends gaining momentum — but not yet locked in

Early signals suggest these trends could gain real traction — but timing, economics, and scale remain uncertain.

4. “Micro‑mega” edge AI deployments are on the rise

As compute density within a single rack skyrockets, many AI workloads will be able to operate on one — or just a handful — of cabinets. These compact yet powerful clusters will increasingly sit alongside conventional compute to support hybrid workloads. Expect a wave of megawatt-class, ultra-dense AI racks for enterprise post-training and inference — small-scale AI factories — embedded within colocation sites, enterprise campuses, or telco edge facilities.

What makes this shift noteworthy is what it reveals about broader AI adoption: AI is moving beyond pilots and proofs‑of‑concept and into day‑to‑day business operations, requiring right‑sized, high‑density compute footprints placed directly where data and decision‑making occur.

Architecturally, this marks a meaningful shift. Instead of concentrating accelerated compute solely in hyperscale campuses or purpose‑built training clusters, enterprises and colocators will increasingly deploy AI directly into existing facilities. This proximity to business‑critical workflows will drive demand for modular, pre‑engineered AI systems that can be “dropped in” with minimal disruption, along with managed AI‑infrastructure services that oversee monitoring, lifecycle management, and performance optimization.

5. Air cooling strikes back

The novelty of liquid cooling has dominated industry discourse for the past three years, pushing vendors and operators to rapidly adapt — bringing new products to market, redesigning systems to accommodate liquid infrastructure, and upskilling operational teams to support deployments at scale. But as AI deployments move beyond frontier‑model training clusters and into enterprise environments, high‑density AI racks will more frequently appear in facilities not originally designed for liquid cooling.

This shift will prompt a resurgence in advanced air‑cooling solutions. Expect a proliferation of 40–80 kW air‑cooled racks supported by extremely high‑performance thermal systems, paired with 60–150 kW liquid‑cooled racks equipped with liquid‑to‑air sidecars. The result: hybrid thermal profiles within the same facility, introducing complex challenges for operators managing uneven heat loads and airflow dynamics.

Far from being overshadowed by liquid cooling, air‑cooling systems are poised for incremental growth as operators seek flexible, retrofit‑friendly approaches to support heterogeneous rack densities across mixed‑use sites.

6. Immersion cooling re-emerges in modular form

After the hype cycle of recent years, immersion cooling is beginning to find its footing in more targeted, pragmatic applications. Rather than competing head‑on with DLC for hyperscale AI clusters, immersion vendors are shifting toward modular, compact systems that deliver differentiated value.

We expect growing traction in edge, telecom, and industrial environments, where immersion’s sealed‑bath architecture offers advantages in reliability, environmental isolation, and minimal site modification. These deployments will remain modest in scale, but meaningful in carving out a sustainable niche beyond today’s supercomputing and crypto segments.

To be clear, immersion cooling is not poised to displace DLC or become a dominant cooling technology. However, it is finally entering a phase where use‑cases align with its strengths — enabling vendors to build viable businesses around modular, ready‑to‑deploy immersion clusters that “drop in” alongside traditional IT and support workloads that benefit from simplified thermal management and rapid deployment.

7. Europe and China wake up — but in very different ways

Europe and China are both poised for stronger AI‑driven data‑center momentum in 2026, but their trajectories could not be more different. In power‑constrained Europe, growth will increasingly hinge on inference deployments located closer to population centers, to minimize network latency (even if compute latency remains the bigger challenge for AI services). This shift toward user‑proximate infrastructure will steer investment toward distributed, high‑density nodes rather than massive gigawatt-scale training campuses. Within this landscape of smaller facilities, a growing cohort of start‑up model builders will prioritize hyper‑efficient architectures that can extract maximum utility from these distributed fleets, for both inference and selective training workflows.

China, by contrast, faces no shortage of power. Its constraint is access to the latest generation of advanced accelerators. We expect operators to continue building at scale using a mix of domestic silicon and whatever Western supply remains available — iterating rapidly as local manufacturers improve capability generation by generation. Over the next few years, this mix‑and‑match strategy will help China bridge the gap until it achieves greater semiconductor self‑sufficiency, resulting in substantial expansion of AI data‑center capacity even under export controls.

The long shots: unlikely swings with outsized impact

Three low-probability but transformative developments, if they emerge, could reshape the data center landscape far more than their probability suggests.

8. U.S. government tightens regulation of the data center industry

A push in Washington to encourage investment in advanced cooling technologies — including a proposed bill aimed at accelerating liquid‑cooling adoption — could have unintended consequences. While well‑intentioned, efforts to steer technological choices risk drawing the federal government more directly into data center design decisions, increasing oversight and potentially making infrastructure requirements more rigid at a time when flexibility is essential.

We do not expect sweeping regulation to materialize in 2026. The current administration has closely aligned itself with AI as a pillar of economic competitiveness and will be wary of stymieing data center buildout, especially given its role in supporting GDP growth. Moreover, political attention will be dominated largely by the mid‑term elections, leaving little bandwidth for complex industry‑specific legislation.

However, affordability and household cost pressures are set to become highly charged political themes — and in that environment, data centers may attract negative scrutiny. As utilities grapple with rising demand and public concern around bills, the industry could face a wave of unfavorable headlines and heightened calls for transparency. To mitigate reputational risk, operators will need to invest more heavily in public engagement, clear messaging, and proactive demonstration of their contributions to reliability, economic growth, and community well‑being.

9. The first liquid-cooling leak critical failure hits the headlines

The early wave of liquid-cooled deployments often moved faster than the industry’s collective design and operational expertise. Many systems were installed without fully accounting for the nuances of coolant management, materials compatibility, monitoring, and routine maintenance — conditions that naturally elevate leak risk. Throughout 2025, we saw scattered reports of cluster-level shutdowns tied to liquid-handling failures, but nothing approaching the scale or societal visibility of a major cloud outage.

While we still believe high-profile failures are possible, their broader impact will likely be limited. Despite growing enterprise adoption, most AI systems are not yet embedded deeply enough in critical business processes to trigger widespread disruption. As a result, even a significant leak-related outage is unlikely to spark the kind of global headlines seen after the AWS blackout — though it may accelerate industry efforts around standards, training, instrumentation, and risk-mitigation practices.

10. The GPU secondary market skyrockets

As hyperscalers and neo cloud providers refresh their fleets, early generations of GPUs — notably Ampere- and Hopper-based accelerators — will increasingly face retirement to make room for newer, more efficient architectures. This raises a key question already weighing on investors: what is the real depreciation timeline for AI hardware on hyperscaler balance sheets?

We expect most older GPUs to shift into lower‑complexity inference workloads or the training of smaller, less compute‑intensive models. We believe it is still too early for widespread scrapping of full data centers built on these platforms, which could flood the secondary market of GPUs looking for another productive life somewhere else.

Enterprise IT environments and colocation providers will see growing volumes of these second‑hand GPUs entering their ecosystems, often at attractive price points. Integrating these “intruders” into general‑purpose, lower‑density compute environments will introduce new operational and thermal challenges. Operators will need to manage concentrated heat loads, non‑uniform rack densities, and power profiles that differ from their conventional estate.

The bubbling question we can’t avoid — even if we tried

Speculation about an AI “bubble” has increasingly dominated media narratives throughout 2025, and the conversation is unlikely to quiet down in 2026. It is true that many AI‑adjacent companies are trading at lofty valuations, buoyed by optimism around future adoption and monetization, an optimism may not prove durable. There is a meaningful possibility that equity markets enter correction territory in 2026, bringing P/E ratios closer to historical norms.

Yet even in a cooling market environment, we do not expect the data‑center buildout to slow materially. Hyperscalers continue to generate ample cash flow to support aggressive infrastructure expansion, and their balance sheets remain low‑leveraged, giving them capacity to secure additional capital if needed. Strategic imperatives will outweigh short‑term market pressure: these companies are locked in a race to establish AI hegemony — or risk being left behind.

In other words, financial markets may wobble, but the underlying drivers of AI infrastructure investment remain intact. The bubble debate will rage on, but the buildout will continue.

Looking ahead: embracing another year of acceleration and uncertainty

As with every prediction cycle, only time will reveal which of these dynamics take hold and which fade into the background. What is certain, however, is that 2026 will yet again challenge our assumptions. The pace of AI‑driven infrastructure evolution shows no signs of slowing, and the industry will continue navigating a rare combination of technological disruption, supply‑chain reinvention, and unprecedented demand for capacity.

While we avoid grand year‑end platitudes, it is fair to say that much will change — and much will stay the same. Power will remain the currency of competitiveness, AI will continue to push infrastructure to its limits, and operators and vendors alike will be forced to adapt faster than ever. At Dell’Oro Group, we look forward to tracking, analyzing, and interpreting these shifts as they unfold.

Here’s to a 2026 that will undoubtedly keep all of us in the data‑center world busy — and to the insights that the next twelve months will bring!

[wp_tech_share]

More stability is expected in 2026. After two steep years of declines that erased roughly $8–9 B of RAN revenue between 2021 and 2024, preliminary findings indicate that market conditions continued to stabilize in the third quarter. This supports the flat-growth thesis we have been communicating for some time and reflects both the maturation of the 5G network and the limited RAN upside beyond traditional consumer-driven MBB, including FWA, private wireless, and premium MBB.

Reflecting on the year and the expectations outlined for 2025, it appears that the high-level message that RAN conditions are improving is mostly correct, though with some regional caveats. Europe, the Middle East, and Africa (EMEA) is performing better than initially expected, in part due to currency exchange rate fluctuations. At the same time, 5G activity in India is coming in below expectations, partly due to coverage delays with the smaller carriers.

The results are mixed across the emerging RAN segments. Private wireless growth is in line with expectations. Preliminary findings from the recently updated Private Wireless report suggest that the positive momentum driving the roughly 40% increase in 2024 extended into 1H25, with worldwide private wireless RAN revenue accelerating rapidly in the first half. And even though Open RAN is stabilizing, growth is still landing at the low end of the 5% to 10% target for the year, in line with market conditions in the U.S. and Japan and the pace of adoption in Europe.

Looking ahead to 2026, we expect more of the same with stable overall investments dominated by regional MBB variations. At the same time, growth prospects will remain favorable with select RAN segments, including 5G, AI RAN, Open RAN, Cloud RAN, and Private Wireless.

Stable RAN in 2026

We have not made any material changes to the short-term outlook and continue to expect both wireless capex and RAN to remain mostly stable in 2026. Although the underlying drivers shaping the RAN market—slower 5G coverage expansion and mobile data traffic growth/capacity investments, ongoing monetization challenges, and limited upside from growth vehicles—are unlikely to change, regional variations should even out next year as growth in North America and APAC outside of China helps to offset weaker investments in China. While there is still uncertainty around the optimal steady-state capital intensity levels in the post-peak 5G phase, we remain cautiously optimistic that growth prospects in markets with steep peak-to-trough setbacks will remain more favorable in 2026.

Suppliers are cautiously optimistic that the improved momentum around 5G SA and premium MBB could improve RAN growth prospects as operators move beyond the coverage/capacity-driven capex and focus more on performance improvements to enable differentiated services while also addressing different UL/DL ratios.

While the networks need to evolve to support changing end-user trends and evolving performance-driven models, we are not forecasting any performance differentiation-driven capex boost in 2026.

Source: Ericsson 3Q25 Network Update

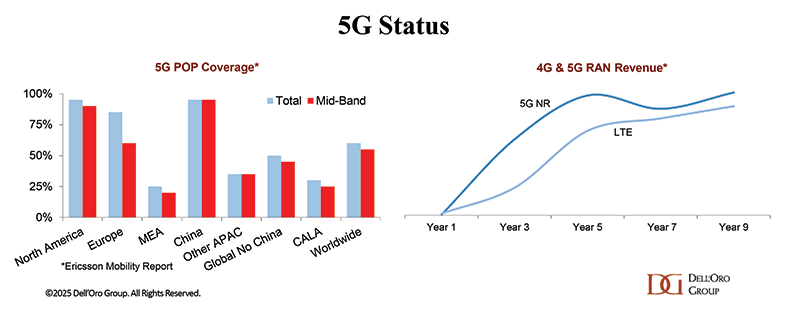

5G is still growing

5G has made significant progress, but further investment is needed to improve coverage, capacity, and overall performance. According to Ericsson’s latest Mobility Report, 5G now reaches roughly 60% of the global population. We estimate that the installed base of 5G macro gNBs represents only about half of the eventual end-state target when accounting for all frequency variants. At the same time, year-over-year comparisons are becoming more challenging, which will weigh on growth prospects. Even so, global 5G RAN growth is expected to remain healthy in 2026, expanding at a modest pace across both macro and small-cell deployments. The overall RAN market, however, is expected to remain stable, as sharply declining 4G investments offset the gains in 5G.

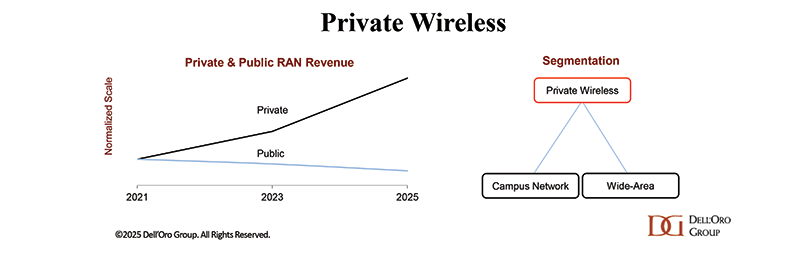

Private Wireless Campus Network to top $1 B

The overall private wireless market remains on track to outpace public RAN growth, increasing by roughly 20% in 2025, supported by both wide-area and local deployments. Looking ahead, private wireless adoption is expected to continue advancing at a healthy pace. Although the overall private wireless RAN growth rate is projected to moderate slightly in 2026—rising 10% to 20%—private wireless campus network RAN revenue is forecast to surpass $1 B. This outlook is underpinned by 1) increased availability of local and shared spectrum, 2) growing enterprise awareness of private cellular benefits, and 3) improved TCO and simplified solutions.

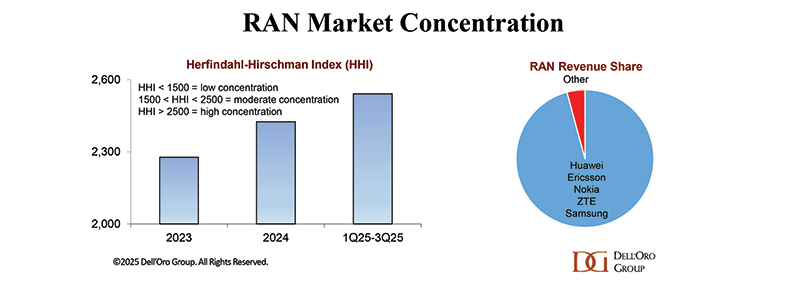

RAN Concentration to remain stable/increase

RAN is becoming more concentrated and divided. Preliminary findings suggest the top five RAN suppliers accounted for 96% of the 1Q25-3Q25 RAN market, up from 95% in 2024. The rise in concentration reflects the status of the smaller suppliers and the share developments among the top suppliers. Given current contract swap visibility and the lack of progress with the smaller suppliers to change the status quo in greenfield settings, the base case is for RAN concentration to remain stable, with a possible increase in 2026.

In summary, the RAN market is adjusting to a post–5G peak-rollout environment characterized by slower data traffic growth and few catalysts likely to alter the flat-growth outlook. Global RAN projections remain essentially unchanged, with the market expected to hold steady in 2026. Beneath the flat topline, however, several segments—including private wireless, 5G, Open RAN, Cloud RAN, AI RAN, and small cells—are still poised for growth. In other words, while overall revenue growth will be muted, 2026 should nevertheless be an eventful year.