Telecom holds steady in the first half. According to preliminary findings, worldwide telecom equipment revenues across the six telecom programs tracked at the Dell’Oro Group*, were flat year-over-year (Y/Y) in the quarter and advanced 2% in the first half of 2023.

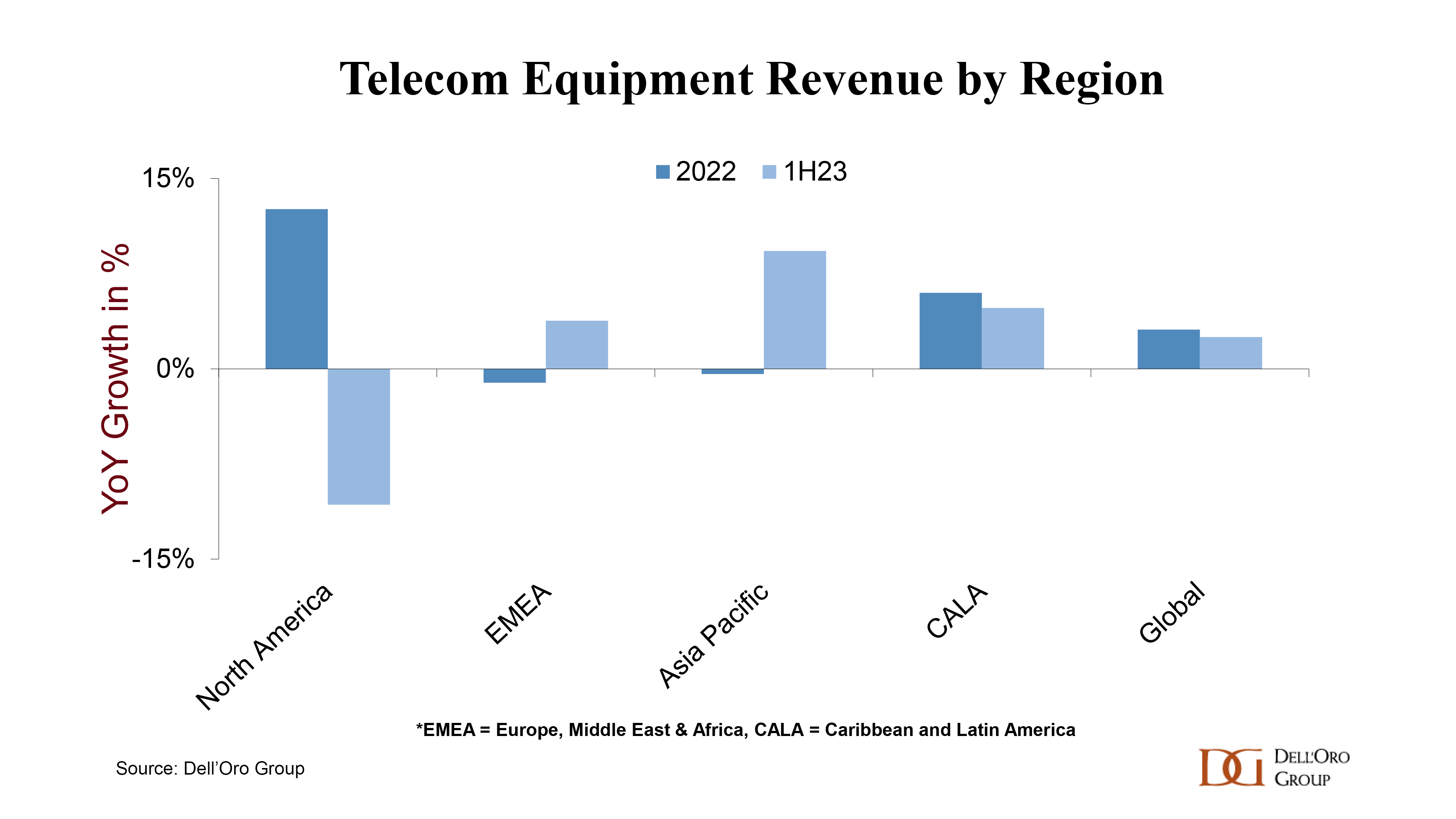

These results mostly align with expectations on an aggregate level, although performance by region and technology varied. After five years of expansion, during which the North America region advanced by around 50%, the pendulum swung toward the negative in the first half. The decline in North America was anticipated, but the pace of the contraction was slightly faster than expected. Alongside more challenging 5G comparisons and inventory corrections affecting some technology segments, North American Broadband Access equipment spending dropped to its lowest levels in nearly two years in the second quarter.

Stable performance in EMEA, CALA, and China, combined with robust growth in the Asia Pacific region outside of China, offset the weakness in the US market. Worldwide telecom equipment revenues, excluding North America, increased by 7% in the first half, supporting the thesis that the telecom equipment market remains robust outside of the US.

From a technology perspective, RAN declined, but the remaining five programs advanced in the first half. Notably, wireline outperformed wireless. Our analysis indicates that the collective results for the wireline-focused programs (SP Routers & Switches, Optical Transport, and Broadband Access) increased by around 7% in the first six months. This, coupled with the positive trends in Mobile Core Networks and Microwave Transmission, was more than enough to offset the more challenging conditions in RAN.

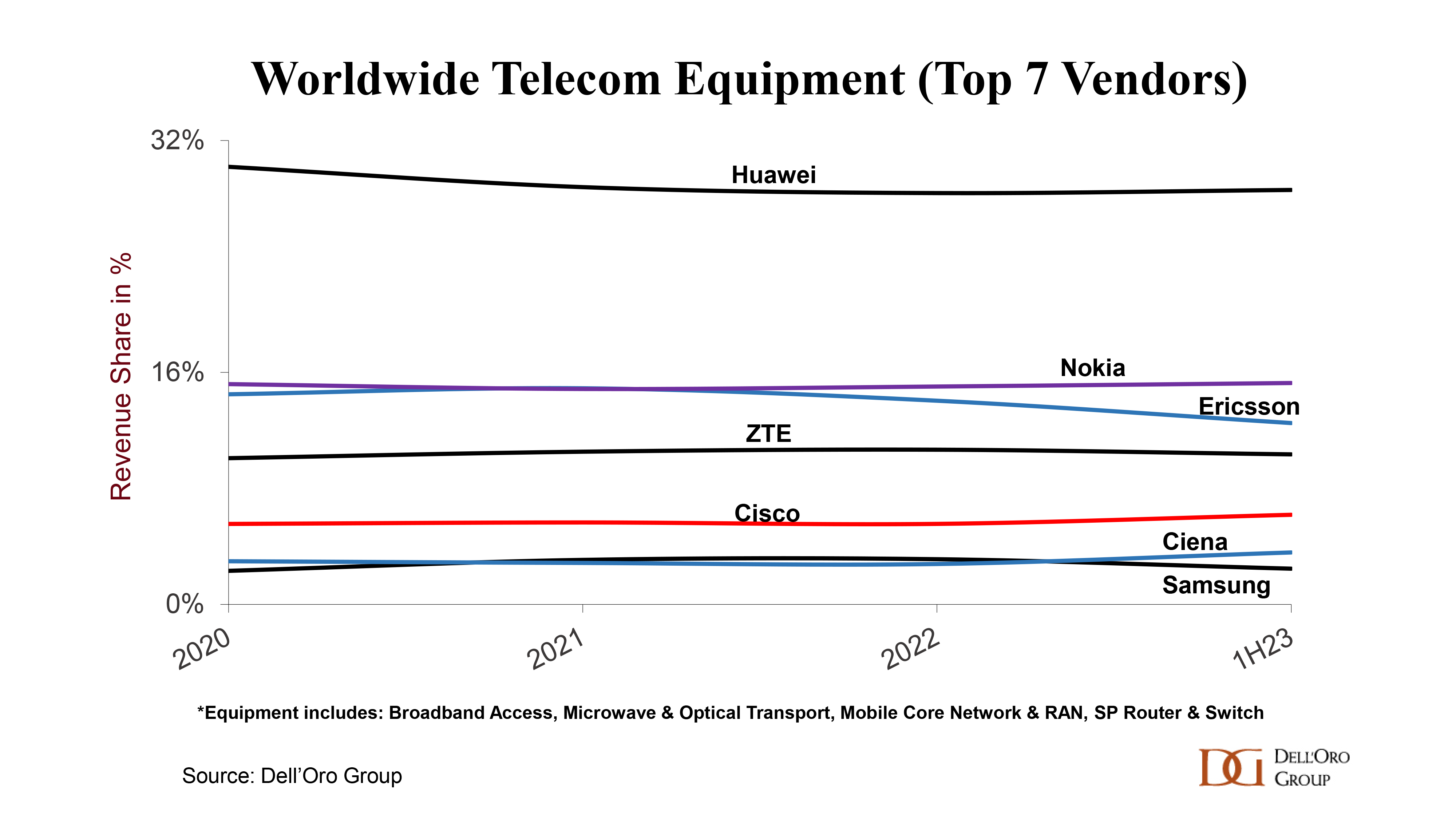

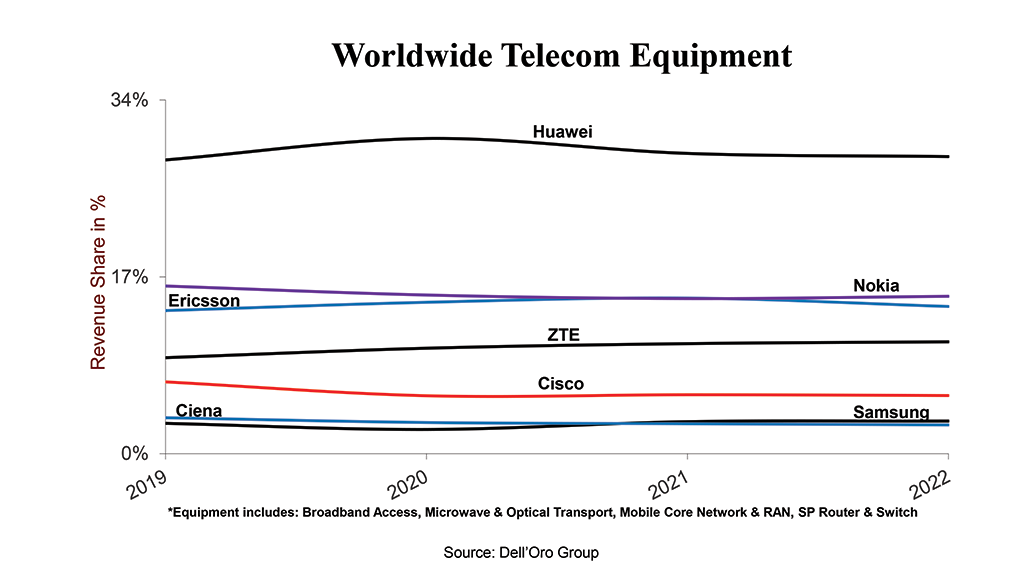

Vendor dynamics remained mostly stable between 2022 and 1H23, with a few exceptions. Ciena surpassed Samsung, and the gap between Nokia and Ericsson widened, reflecting, to some extent, the technology mix between wireless and wireline. Despite ongoing efforts by the US government to limit Huawei’s addressable market and access to the latest silicon, our analysis shows that Huawei still leads the global telecom equipment market. This is partly because Huawei remains the #1 supplier in five out of the six telecom segments we track, and the vendor continues to dominate the market outside of North America, accounting for 35% to 40% of 1H23 revenues.

The analyst team has not made any significant changes to the collective short-term outlook. Following five consecutive years of growth, worldwide telecom equipment revenues are projected to remain flat in 2023. As always, there are risks in both directions. In addition to currency fluctuations, economic uncertainty, and elevated interest rates, inventory adjustments, new technology rollouts, and the anticipated impact of national subsidization efforts can impact steady-state assumptions for the various regions.

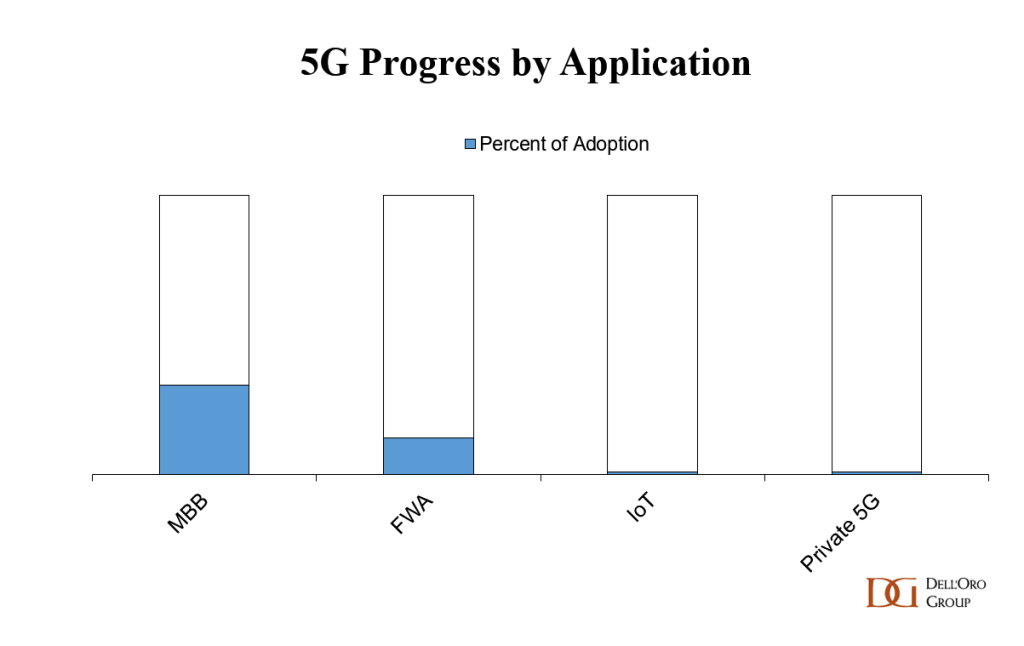

5G has come a long way since the Korean operators launched mobile 5G in early 2019. In just four years, operators have invested more than $300 B globally in 5G-related capex, deploying 15 M+ macro and small cell radios. Adoption has been mixed. On the one hand, 5G has been a massive success for the typical Mobile Broadband (MBB) use cases, providing operators with pivotal tools to support data traffic growth and driving down the cost per bit. On the other hand, 5G is still mostly about MBB and Fixed Wireless Access (FWA). The technology has not touched the surface yet when it comes to connecting machines and industries. As we look to the next part of this 5G journey, any incremental technology advancements that can improve the spectral efficiency will come in handy in a world where spectrum is limited and humans/machines steadily consume increasingly greater amounts of data. More importantly, any enhancements that can improve the growth prospects for Enterprise/Private 5G and Cellular IoT (cIoT)—ultimately helping to realize more aspects of the broader 5G vision—will play an important part in this next phase. In this blog, the objective is to update the 5G Advanced blog we previously posted and review the technologies, opportunities, and RAN implications.

What is 5G-Advanced?

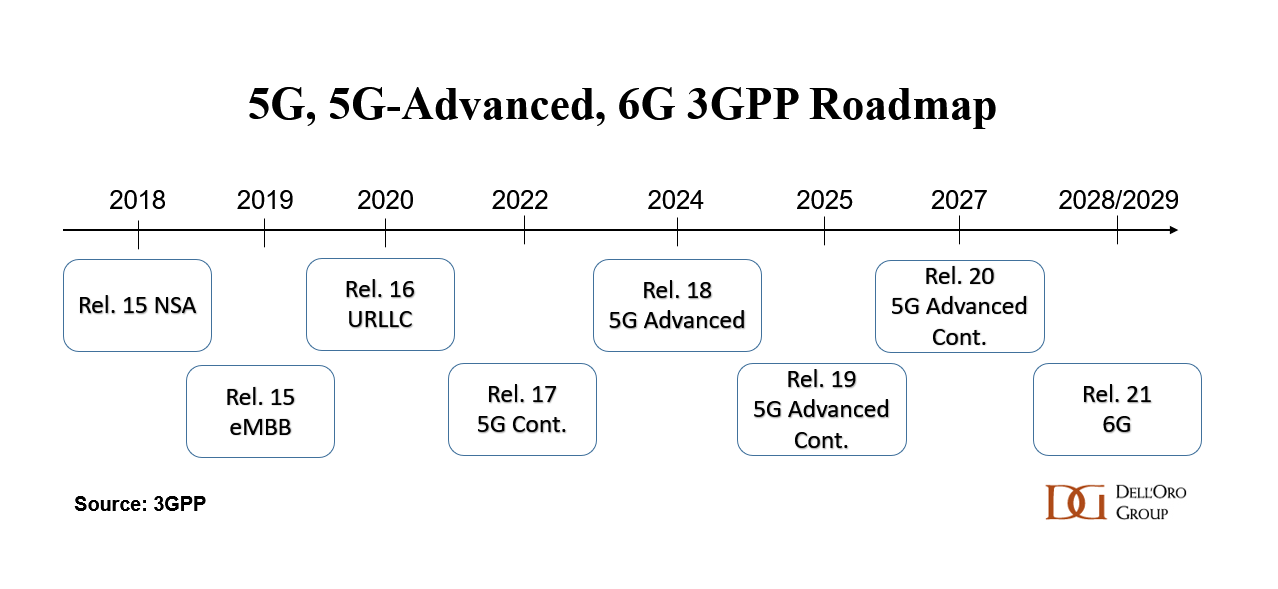

The 3GPP roadmap is continuously evolving to fulfill the larger 5G vision. In this initial 5G wave that began in 2018, 3GPP has already completed three major releases (new releases every 1.5 to 2 years): 15, 16, and 17.

The schedule for 3GPP Release 15 included three separate steps: the early drop, focusing on NSA option 3; the main drop, focusing on SA option 2; and the late drop, focusing on completion of 4G to 5G migration architectures. While MBB is dominating the capex mix in this initial 5G phase, the 3GPP roadmap is advancing to address opportunities beyond MBB.

Release 16, also known as Phase 2, was completed in July 2020. The high-level vision is that Release 16 will provide the initial foundation for taking 5G to the next level beyond the MBB phase, targeting broad-based enhancements for 5G V2X, Industrial IoT/URLLC, and NR-U.

Release 17, also known as continued 5G expansion, was completed in early 2022. This 5G version provides more enhancements, extending operations up to 71 GHz with enhancements to IoT, Massive MIMO, Non-terrestrial networks (NTN), and DSS, among other things. With 3GPP Rel-17, a new device type (“NR Light”) was introduced, to address industrial sensors.

These initial releases have been key to the success of both MBB and FWA. But there are still shortcomings that need to be addressed, in order to fulfill the broader 5G vision. The current thinking with Release 18 and beyond (5G-Advanced or 5.5G) is that gradual technology improvements will help to take 5G to the next level, creating a foundation for more demanding applications and a broader set of use cases.

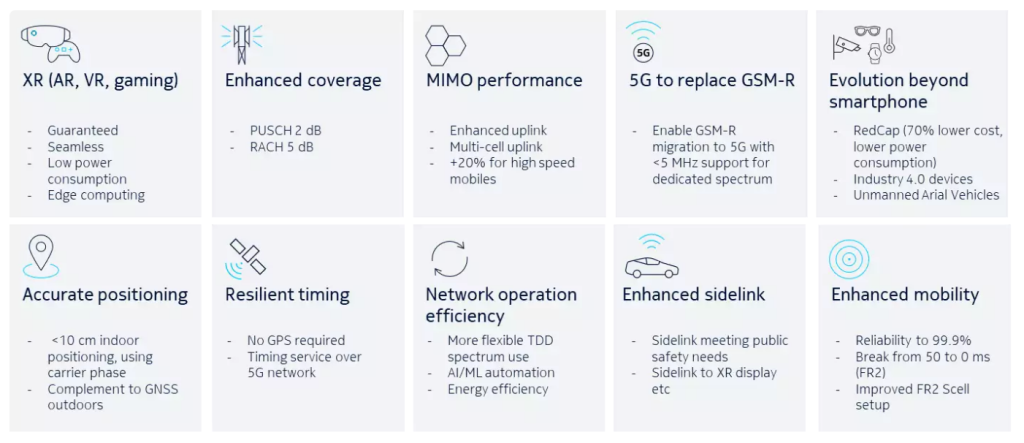

Current priorities with 5G-Advanced include:

More capacity and better performance. Some estimates suggest that MIMO enhancements, better beam management, and full duplex technologies taken together with other advancements will deliver another 20% of speed improvements relative to today’s 5G. Enhanced uplink (UL) and multi-cell UL improvements could pave the way for greater data rate and latency improvements in the UL.

Expanded coverage. In addition to MIMO and IAB coverage enhancements, 5G-Advanced also includes Non-Terrestrial Network (NTN) connectivity improvements, building on the NR/LTE-based NTN support that was introduced with Release 17.

More intelligence. Releases 15-17 already include some AI/ML features. 5G-Advanced will likely offer AI/ML enhancements in the RAN (including the air interface) and the management layers. In addition, Intelligent RAN and AI-powered analytics will help operators to proactively address network issues before they become a major problem.

Energy savings. Release 18 includes a confluence of static and dynamic power-saving enhancements for the radios and the overall RAN. Also, the specification is targeting to define a base station energy consumption model with various KPIs to better evaluate transmission and reception consumption/savings.

Flexible spectrum (FD, DSS, CA). NR is currently based on TDD or FDD spectrum. Full duplex (FD), a 5G-Advanced contender, improves spectrum utilization by allowing UL and DL to share the same spectrum (FD should improve capacity and latency, especially in the UL). Release 18 also includes DSS capacity enhancements (increasing PDCCH capacity by allowing NR PDCCH to be transmitted in symbols overlapping with LTE CRS). Other spectrum-related upgrades with 5G-Advanced include multi-carrier enhancements and NR support for dedicated spectrum bandwidths below 5 MHz.

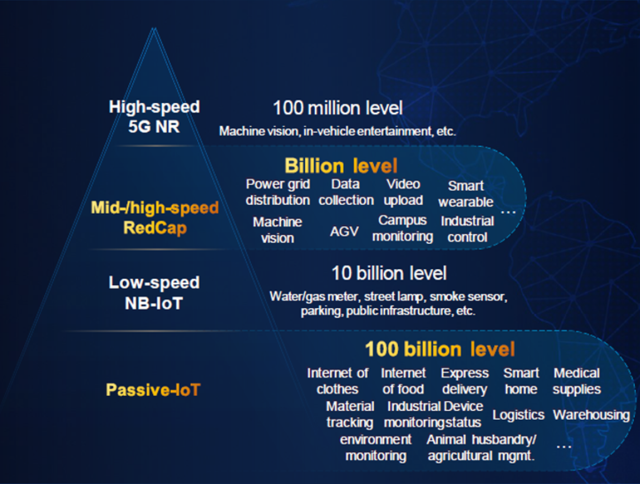

Critical IoT. 5G-Advanced includes multiple industrial and IoT related advancements. Release 17 included support for Time Sensitive Networking (TSN), which will be expanded in 5G-Advanced to support Deterministic Networking (DetNet). NR-Light or Reduced Capability (RedCap) was introduced with 3GPP NR Release 17. 5G-Advanced will introduce lower-tier RedCap devices, seeking to find a better set of tradeoffs between cost, performance, and power consumption.

Sensing. Harmonized communication and sensing (HCS) is a Release 19 study item.

Positioning. Positioning is already supported in Release 16/17, however, 5G-Advanced is expected to improve positioning accuracy and power consumption (Nokia has said sub-10 cm positioning is doable). In addition, Release 18 will include support for RedCap devices.

With 5G growth now slowing in the public service provider-driven market, the search is on for the next growth vehicle that can help to offset the more tepid consumer MBB trends. All things considered, it is tempting to assume the growth opportunities will align perfectly with the PowerPoint vision, meaning enterprise 5G, new MBB scenarios, cIoT, and FWA all stand to benefit in the 5G-Advanced era. We remain optimistic about most of these potential gold mines, but we also need to keep in mind that disconnects between vision and reality are common.

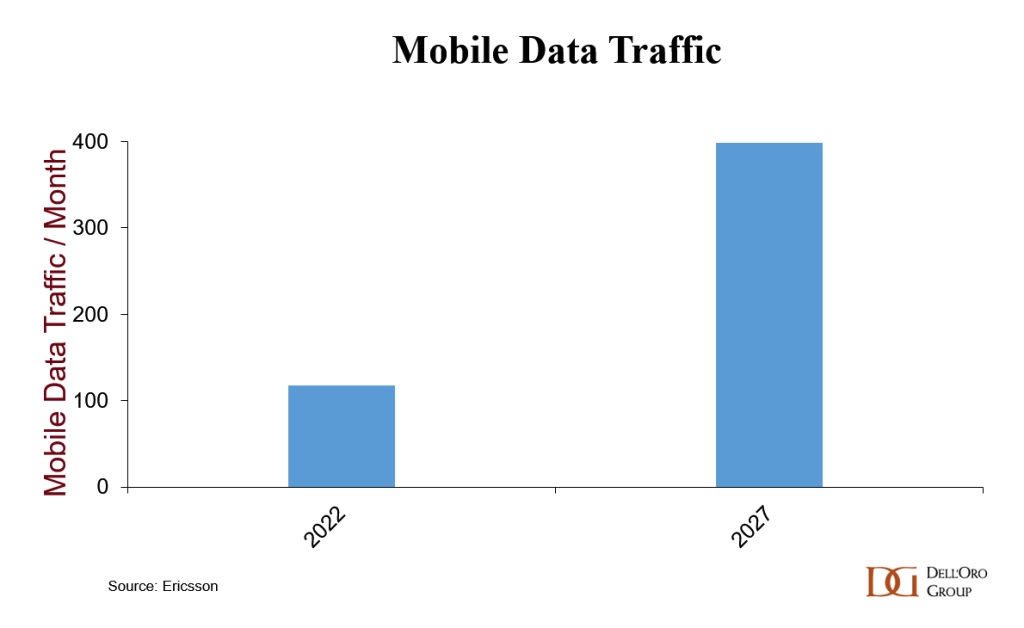

It might not be the most exciting revenue growth opportunity for the carriers but one fundamental aspect with 5G-Advanced will be to support more demanding consumer MBB applications. Currently, total mobile data traffic (including FWA traffic) is projected to advance another 3 to 4x by 2027. More spectrum is always helpful but given the lack of global coordination in the Upper-6 GHz spectrum, operators will need to rely on sub-6 GHz spectrum, spectral efficiency gains, DSS enhancements, and more favorable mmWave economics to support more data traffic and reduce the cost per bit.

But the real excitement with 5G-Advanced is the enterprise opportunity. Private LTE/5G is developing at a slower pace than initially expected and the market remains small, with private 5G still accounting for less than 1% of the overall 5G RAN market. Operators outside of China are also reporting that the incremental revenue upside from industry verticals remains negligible. The slower start is not impacting the long-term growth thesis: proliferating cellular connectivity into enterprises and industrial settings where WiFi or public cellular connectivity is poor remains a massive growth opportunity. Although LTE and 5G NR Releases 15-17 are enough to address the lion’s share of the existing use cases, 5G-Advanced will provide important IoT and industry-focused enhancements.

One of the enterprise contenders with 5G-Advanced is the warehouse segment. Per Nokia’s industrial site assessment, warehouses comprise around 20% to 25% of the overall industrial site opportunity. Covering around 2.3 B square meters globally (Warehouse Building Stock), a shift toward 5G warehousing could move the enterprise needle.

Helping to explain the excitement with 5G-Advanced is the promise of Passive IoT. In addition to the improved economics relative to RFID based sensors, Passive 5G-Advanced IoT solutions should be favorable from a power consumption perspective (according to Huawei, passive IoT devices consume 100x less power than a NB-IoT device).

Source: Huawei

Fueled by the vision that 5G has a growing role to play in the Factory of the Future, 5G and 5G-Advanced manufacturing expectations are rising. While WiFi and LTE still address the great majority of the smart manufacturing connectivity market, our assessment is that 5G RAN revenues to support the manufacturing vertical are improving. In fact, the manufacturing already accounts for a double-digit share of Huawei’s, Nokia’s, and Ericsson’s ongoing private wireless projects. In the case of Huawei, manufacturing makes up roughly half of its enterprise ToB revenues. Nonetheless, it is still early days here and the majority of the enterprises are in the exploratory phase when it comes to using 5G based AGVs, Digital Twin, AR/VR, and quality inspections. The improved reliability, latencies, device costs, positioning accuracy, and UL throughput should all help to improve the industrial 5G business case but as with most enterprise verticals, it will take time. Leading industrial players such as Siemens, GE, and ABB, however, have all taken actions expressing the belief that the timing to introduce more 5G is right.

Sensing has potential with both public and private deployments. Per Huawei’s MWC Shanghai update, 5.5G sensing features have been verified in various traffic and low-altitude scenarios. The improved accuracy and range relative to traditional traffic sensors could help the IoV (Internet-of-Vehicles) segment.

What does this mean for the RAN forecast?

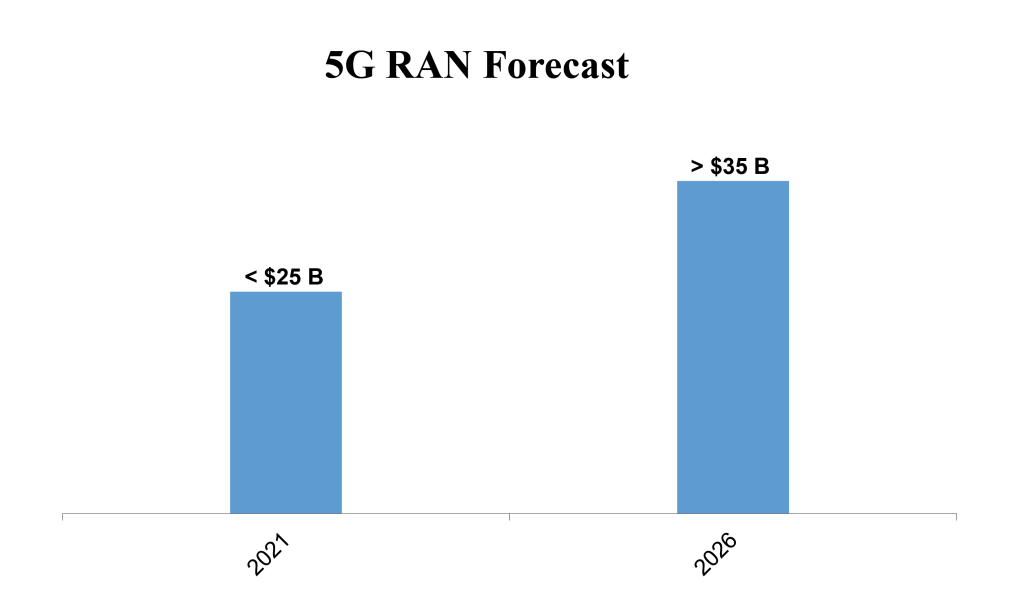

Following a couple years of exponential growth, 5G RAN investments are slowing. At the same time, it is still early in the broader 5G cycle. The message we have communicated for some time still holds: Our baseline scenario rests on the assumption that the 5G cycle will be longer and deeper than the LTE investment phase. And even though the base case is not hinging on the premise that 5G-Advanced will drive another capex cycle, Release 18 and future releases are expected to play important roles in this next part of the 5G journey.

Predicated on the assumption that the first part of the 5G-Advanced standard will be frozen in early 2024, commercial deployments could become a reality by 2025. If so, a significant portion of the 5G base stations deployed in 2027 will include some 3GPP Release 18 features.

In short, 5G-Advanced represents an important part of the 5G roadmap. The excitements levels for the various 5G segments will vary. Before we set unrealistic expectations, it is important to keep in mind that it took more than 10 years for enterprises to achieve an enterprise Wi-Fi installed base of 5% to 10% of the projected 2027 installed base. The enterprise is a major opportunity but 5G-Advanced is not going to change Amara’s Law (the effect of a technology in the short run tends to be overestimated, while underestimated in the long run).

Related blogs:

[wp_tech_share]

The use of AI in the radio access network (RAN) is not new. In fact, 4G and 5G deployments already rely heavily on automation and intelligence to replace manual tasks and manage the increased complexity without raising the costs. AI is also used in both 4G and 5G to improve network performance and the user experience. What is new, however, is the proliferation of consumer and enterprise AI and the change in attitude toward this tool. As the conversation about the implications for society as a whole is now moving to center stage, the timing is right to review how AI is likely to impact the RAN market, both directly and indirectly. In this blog, we will focus on four specific areas: mobile data traffic, operator revenue, RAN economics, and RAN architectures.

Is the proliferation of consumer and enterprise AI fueling an increase in mobile data traffic?

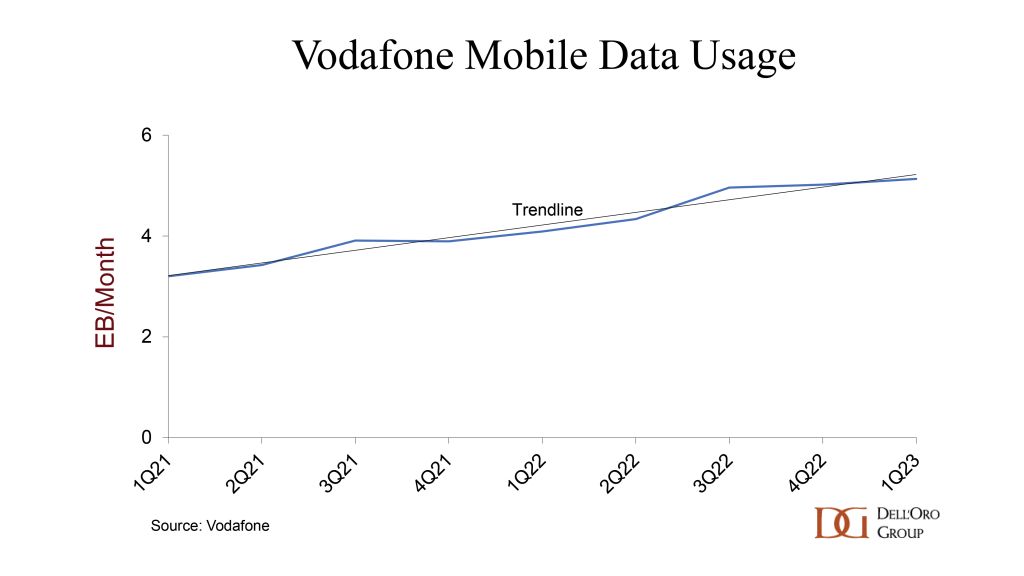

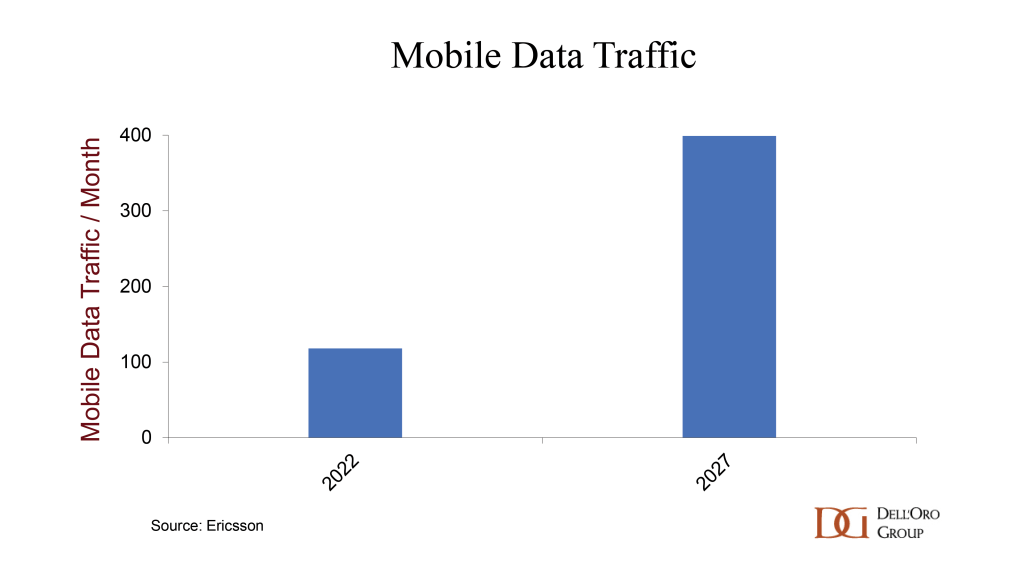

Preliminary findings suggest that AI tools such as ChatGPT and Google Bard are not at this time directly affecting mobile data usage. Data points are limited. Vodafone’s data usage in 1Q23 shows no discernable change in its overall consumption relative to the trend line. And per Ericsson’s latest Mobility report, mobile data traffic grew 36% in 1Q23, in line with the YoY growth trajectory over the past two to three years. While AI is changing computing, power, and cooling requirements inside the data center, the impact on the mobile network has so far been negligible. Over time of course this could change, either directly or indirectly, if for example AI triggers greater video usage or if the computing location changes. But for now, we don’t see a need to change mobile traffic projections to accommodate the rise of consumer AI. Per Ericsson’s Mobility Report, mobile data traffic is projected to grow at a CAGR of 25% to 30% between 2022 and 2027.

What does this mean for operator revenues?

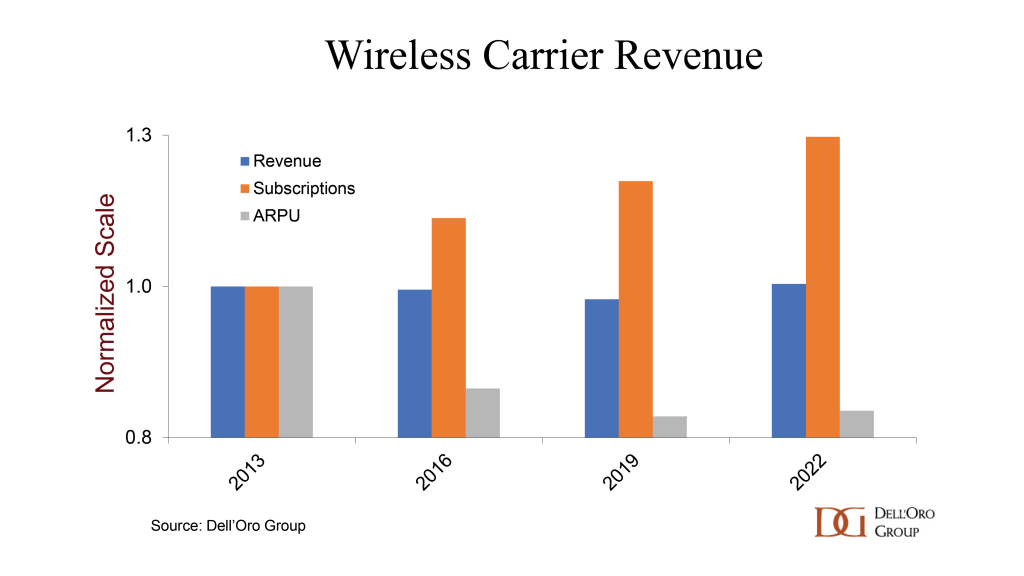

Global wireless carrier revenues advanced at a double-digit rate during the 1G-3G era, as mobile subscriptions exploded. But growth slowed with 4G and fresh data show that wireless revenues have stayed flat over the past ten years. The root cause is not the lack of subscription growth. Instead, we attribute the stable revenue trends to the slump in average revenue per user (ARPU), which has been down by roughly 20% over the past ten years. Even as AI is improving the optimism for potential revenue expansion, the downward pressure in ARPU in combination with slower subscription growth will continue to weigh on the prospects for growth in the area of consumer mobile broadband (MBB).

It is unlikely that AI will change these forces that now underpin the lion’s share of carrier wireless revenues. However, it is still crucial that operators invest in these tools so that they can extract more value from enterprises and verticals, improve the business case for fixed wireless access (FWA), and enhance their competitive position in all areas, including consumer MBB. In addition to improving performance and customer experience—which will indirectly improve revenues by minimizing churn—AI could assist with data monetization, especially in the enterprise, where this tool can help to optimize the user experience for 5G use cases and secure QoS levels that are key for premium services. In the future, AI might also play a role in terms of network slices.

How will AI and Intelligent RAN change RAN economics and performance?

As mobile data traffic continues to grow 25% to 30% annually while carrier revenue growth remains flat, operators have limited wiggle room to expand capex and opex to manage the increased complexity typically inherent with the technological and architectural advancements required to deliver the appropriate network performance while supporting more demanding and diverse end-user requirements. The impact on topline expansion will be limited but AI capabilities taken together with recent technology advances that allow suppliers to place intelligence inside the base station will be crucial for improving RAN economics and performance. Recent proliferation with generative AI is raising the expectations that continuation of this trend will:

Improve performance and experience

Maximize ROI on network investment

Improve the vRAN business case

Boost network quality

Accelerate time to market

Reduce complexity

Reduce energy consumption

Bring down CO2 emissions

The use of AI in the RAN is already delivering benefits in network deployment, optimization, and healing, ultimately contributing to an improvement of network performance and quality. These AI tools can be used to analyze end-user drivers and traffic patterns, while improving resource utilization. In addition, Intelligent RAN and AI-powered analytics will help operators to proactively address network issues before they become a major problem. Vodafone’s Zero Touch Operation Strategy, for example, aims to prevent 50% of the faults. A North American service provider was able to detect RAN issues 120x faster with Nokia’s AI/ML-powered SON.

According to Ericsson, operator opex could double over the next five years without more automation across deployment and management & operations, just to support the MBB-driven changes. AI will play an important role here simplifying complexity and curbing opex growth. Most of the greenfield networks are clearly moving toward new architectures that are more automation-conducive (Rakuten Mobile operates 300 K+ cells with an operational headcount of around 250 people). Change typically does not happen as quickly, however, with the brownfields. The average brownfield operator today falls somewhere between L2 (partial autonomous network) and L3 (conditional autonomous network), with some way to go before reaching L4 (high autonomous network) and L5 (full autonomous network). Still, China Mobile remains on track for L4 automation by 2025. Huawei remains optimistic that L4 Autonomous Driving Network (ADN) will be more prevalent by approximately 2025 (70% of its customer base plans to achieve L3 ADN by 2025). Rakuten Mobile previously said that its network could achieve L4 automation by the end of 2022. Vodafone has also set the target of achieving zero-touch intelligent networks by 2025, while Zain is targeting L4 automation by 2025.

Performance gains underpinned by Intelligent RAN will vary, depending on a variety of factors. Ericsson estimates that Intelligent RAN Automation solutions can improve the spectral efficiency by 15%, while Huawei has been able to demonstrate that its Intelligent RAN multi-band/multi-site 3D coordination feature can improve the user experience by up to 50% in some settings. ZTE and China Mobile have demonstrated a 3x rate of throughput improvement at the cell edge, in addition to a 50% reduction in handover delays.

With the RAN comprising around 1% to 2% of global electricity consumption (ITU), the intensification of climate change taken together with the current power site trajectory forms the basis for the increased focus on energy efficiency and CO2 reduction. Preliminary findings suggest that Intelligent RAN can play a pivotal role in curbing emissions, cutting energy consumption by 15% to 25%. As an example, Zain was able to realize 23% energy savings at a test site in Kuwait utilizing Huawei’s Intelligence-based energy saving solutions. Some operators are even more optimistic: Tele2 recently published a report demonstrating how smarter mobile networks can reduce energy consumption in the long term by as much as 30% to 40%.

The proliferation of AI now also offers the potential to improve vRAN economics. One of the main TCO challenges with vRAN/Cloud RAN is the difficulty of realizing efficiency gains from orchestrating several workloads. As a result, some are now exploring the possibility of improving the vRAN business case by realizing synergies in other ways (such as between 5G and AI). Softbank and Nvidia recently announced that they are looking at the utilization and financial benefits of deploying 5G vRAN on the same servers that run AI. While the TAM for centralized vDU implementations is limited, it will be interesting to follow Softbank’s progress here.

What does AI mean for future RAN architectures?

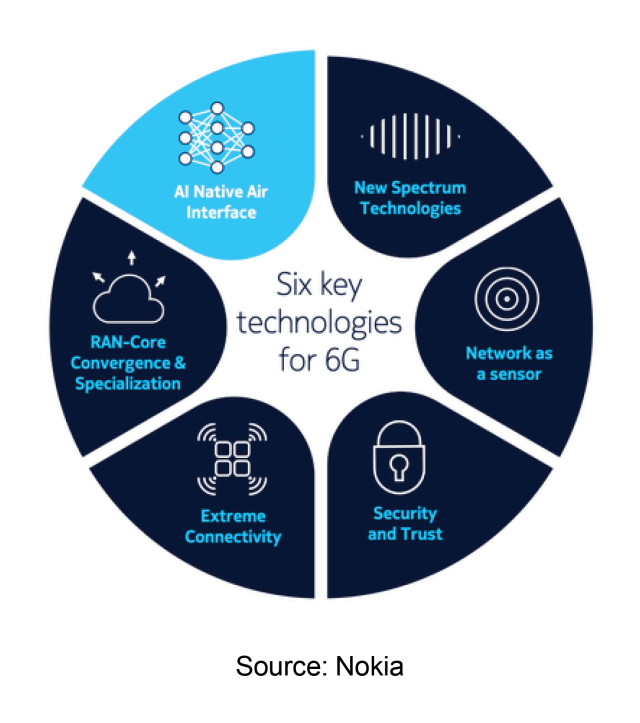

AI is already available in the RAN today to some degree, albeit to a limited extent. Going forward, however, the share of AI in the RAN will undoubtedly rise. In addition to increased use of AI with existing 5G networks, 5G-Advanced promises to introduce more AI and ML enhancements in the RAN, including in the air interface. And while we are still in the early days of 6G the current thinking is that AI native Air interfaces will be one of the fundamental technologies.

It would be premature at this early stage to attempt to paint a comprehensive picture as to how AI will transform society and the telecom networks. But compared to previously hyped technologies, one of the differences with AI is the broad-based acceptance that all roads lead to more of it. So even if this is not the magic answer for operators to grow consumer ARPU, there is no doubt that suppliers and operators will gradually increase the use of AI in and around the RAN.

[wp_tech_share]

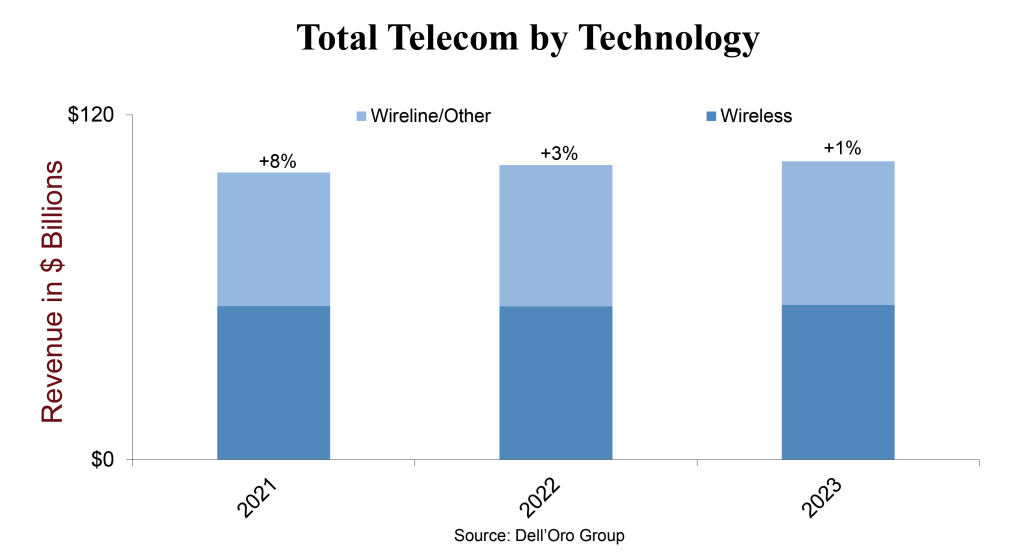

Following four consecutive years of modest telecom equipment growth across the six telecom programs tracked at the Dell’Oro Group*, preliminary findings show that the aggregate telecom equipment market moderated somewhat from the 8% revenue increase in 2021 to 3% year-over-year (Y/Y) in 2022.

Looking back at the full year, the results were slightly lower than the 4% growth rate we projected a year ago going into 2022. In addition to more challenging comparisons in the advanced 5G markets and the supplier exits in Russia, the strengthening USD weighed on the broader telecom equipment market. Supply issues also impacted the market negatively during 1H22 but eased somewhat in the second half.

Regional developments were mixed, underpinned by strong growth in North America and CALA, which was enough to offset more challenging conditions in EMEA and the Asia Pacific. With China growing around 4%, we estimate global telecom equipment revenues excluding China increase around 3% in 2022.

From a technology perspective, there is a bit of capex shift now underway between wireless and wireline. Multiple indicators suggest Broadband Access revenues surged in 2022, however, this double-digit growth was offset by stable or low-single-digit growth across the other five segments (Microwave Transport, Mobile Core Network, Optical Transport, RAN, SP Router & Switch).

Vendor dynamics were relatively stable between 2021 and 2022, with the top 7 suppliers driving around 80% of the overall market. Despite on-going efforts by the US government to limit Huawei’s TAM and access to the latest silicon, our assessment is that Huawei still leads the global telecom equipment market, in part because Huawei remains the #1 supplier in five out of the six telecom segments we track. At the same time, Huawei has lost some ground outside of China. Still, Nokia, Ericsson, and Huawei were the top 3 suppliers outside of China in 2022, accounting for around 20%, 18%, and 18% of the market, respectively.

Following five consecutive years of growth, the Dell’Oro Group believes there is more room left in the tank. Collectively the analyst team is forecasting the overall telecom equipment market to increase 1% in 2023 and record a sixth consecutive year of growth. Risks are broadly balanced and the analysts will continue to monitor the 5G rollouts in India, capex cuts in the US, and 5G slowdown in China (preliminary data by MIIT suggest new 5G BTS volumes will drop by a third in 2023 relative to 2022), wireless and broadband investments in Europe, forex fluctuations, and inventory optimization.

*Telecommunications Infrastructure programs covered at Dell’Oro Group, include Broadband Access, Microwave & Optical Transport, Mobile Core Network (MCN), Radio Access Network (RAN), and SP Router & Switch.

[wp_tech_share]

We just returned from MWC after a couple of intense days of meetings. RAN might not be the fastest growing market but from a technology perspective, the pace of change simply remains impressive and the MWC is a great event to witness the progress. Although we are not the right source to capture all of the PR activity involving incremental product announcements, we want to point out a few RAN-related observations that could potentially impact the RAN forecast or vendor dynamics.

Virtualized RAN is gaining momentum

As we now know, vRAN started out slow but picked up some speed in 2022 in conjunction with the progress in the US. The challenge from a forecasting perspective is that the visibility beyond the greenfields and the early brownfield adopters is limited, primarily because purpose-built RAN still delivers the best performance and TCO. As a result, there is some skepticism across the industry about the broader vRAN growth prospects.

During MWC, we learned four things: 1) Near-term vRAN visibility is improving – operators in South Korea, Japan, US, and Europe are planning to deploy vRAN in the next year or two. 2) vRAN performance is firming up. According to Qualcomm, Vodafone (and Qualcomm) believes the energy efficiency and performance gap between the traditional and new Open vRAN players is shrinking (Vodafone publicly also praised Mavenir’s OpenBeam Massive MIMO AAU). Samsung also confirmed (again) that Verizon is not giving up any performance with Samsung’s vRAN relative to its purpose-built RAN. 3) vRAN ecosystem is expanding. In addition to existing vRAN suppliers such as Samsung, Ericsson, Mavenir, Rakuten Symphony, and Nokia announcing improvements to their existing vRAN/Cloud RAN portfolios, more RAN players are jumping on the vRAN train (both NEC and Fujitsu are expecting vRAN revs to ramp in 2023). And perhaps more interestingly, a large non-RAN telecom vendor informed us they plan to enter the vRAN market over the next year. 4) The RAN players are also moving beyond their home turf. During the show, Nokia announced it is entering the RAN accelerator card segment with its Nokia Cloud RAN SmartNIC (this is part of Nokia’s broader anyRAN strategy).

256T256R Massive MIMO

For a technology that was initially viewed as being mostly fit for high-traffic locations, Massive MIMO has come a long way in just a few years, ramping at a much faster pace than initially expected. As we recently outlined in the Massive MIMO 2022 blog, the days of exponential growth are in the past but there is still Massive MIMO upside ahead to support TDD MBB expansions in the less advanced markets, FDD hotspot deployments, FWA, and TDD product refresh to take advantage of continuous product improvements such as wider IBW, lower power consumption, smaller form factors, and more transceivers/antenna elements.

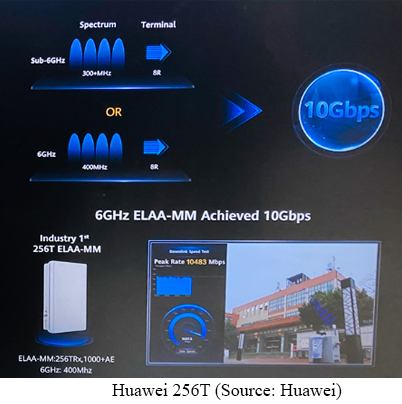

With limited new sub-7 GHz spectrum on the horizon, improving the spectral efficiency using more didoes and transceivers will continue to play a fundamental role with 5G, 5G-Advanced, and 6G. This is not a surprise. However, since we previously assumed the 128T128R would be the de-facto configuration for the 6 to 7 GHz band, it was somewhat surprising to see Huawei’s 256TRx prototype in the booth (ZTE had a 128T128R AAU in its booth).

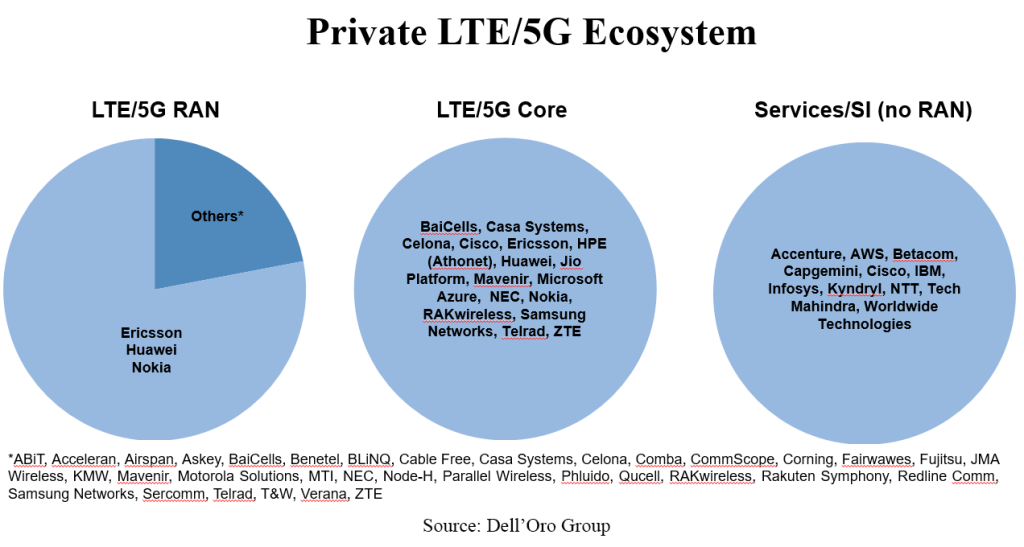

Private 5G ecosystem is evolving

Private 5G is running behind schedule. We recently adjusted the private wireless forecast downward to reflect the current state of the market. Still, the slow uptake is not dampening the enthusiasm for private wireless. If anything, the interest is growing and the ecosystem is evolving as suppliers with different backgrounds (RAN, core, Wi-Fi, hyperscaler, in-building, SI) are trying to solve the enterprise puzzle. Below is a summary of the private RAN, core, and SI/services providers that we are currently monitoring.

More suppliers want a piece of Europe

Per our 4Q22 RAN report, Ericsson, Nokia, and Huawei collectively accounted for around 95% of the European RAN market in 2022. Other RAN suppliers have tried to expand their respective footprints over the past couple of years without much success. One of the takeaways from the MWC discussions is that activity with the smaller suppliers is on the rise:

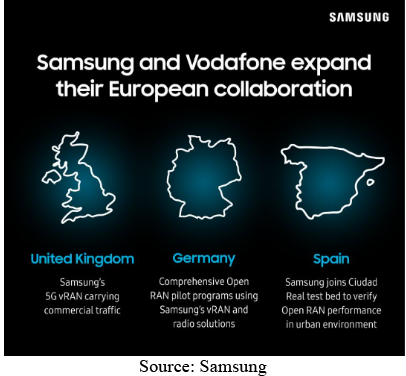

Samsung highlighted its vRAN/Open RAN progress with Vodafone in the UK, Germany, and Spain and remains optimistic its European RAN revenues will soon become more material.

NEC started recognizing European RAN revenues in 2022 (primarily driven by 1&1 in Germany).

Fujitsu believes its European RAN growth prospects will improve in 2024.

Mavenir has 10 K brownfield Open RAN sites in the pipeline for 2023/2024 – Deutsche Telekom is part of the mix, however, the exact upside in Europe remains unclear.

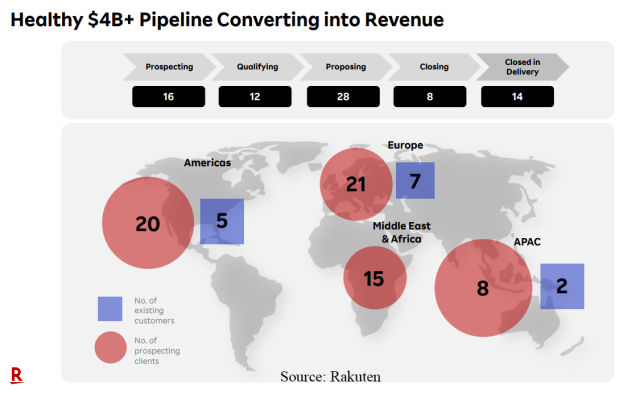

Rakuten Symphony recently estimated its Open RAN pipeline is worth around $2B (half of the total pipeline). We don’t know the size of the European component. However, the company recently reported that nearly half of the # (not value) of prospecting clients (for RAN and non-RAN) are located in Europe per the chart below.

While it is unlikely that management over at Ericsson, Nokia, and Huawei are losing a ton of sleep at this juncture from these announcements, it might be worthwhile to check back in a year if the collective share of the top 3 is still around 95%.

Skepticism is on the rise

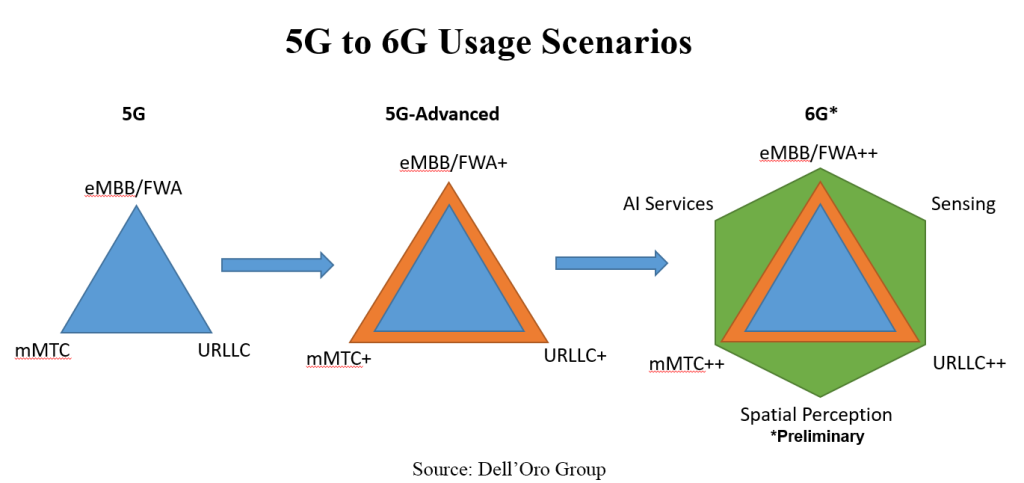

Not surprisingly, disconnects between vision and reality are common when new technologies are introduced. Even if this is expected, we are sensing more frustration across the board this time around, in part because RAN growth is slowing and 5G still has mostly only delivered on one out of the three usage scenarios outlined in the original 5G use case triangle. With 5G-Advanced/5.5G and 6G starting to absorb more oxygen, people are asking if mMTC+/mMTC++ and URLLC+/URLLC++ are really needed given the status of basic mMTC and URLLC. Taking into consideration the vastly different technology life cycles for humans and machines, there are more questions now about this logic of assuming they are the same and will move in tandem. If it is indeed preferred to under-promise and over-deliver, there might be some room to calibrate the expectations with 5G-Advanced/5.5G and 6G.

And most importantly, this was our first live MWC event since 2019. It was great to be back and meet people in person without any Covid restrictions. The energy level at the show was amazing – now if this energy could somehow start showing in the RAN numbers, that would be even more exciting.