Preliminary estimates suggest 1Q20 CBRS RAN revenues were in line with expectations, accounting for 1% to 3% of the overall 1Q20 North American RAN market. Even if the regulatory process has taken significantly longer than expected,

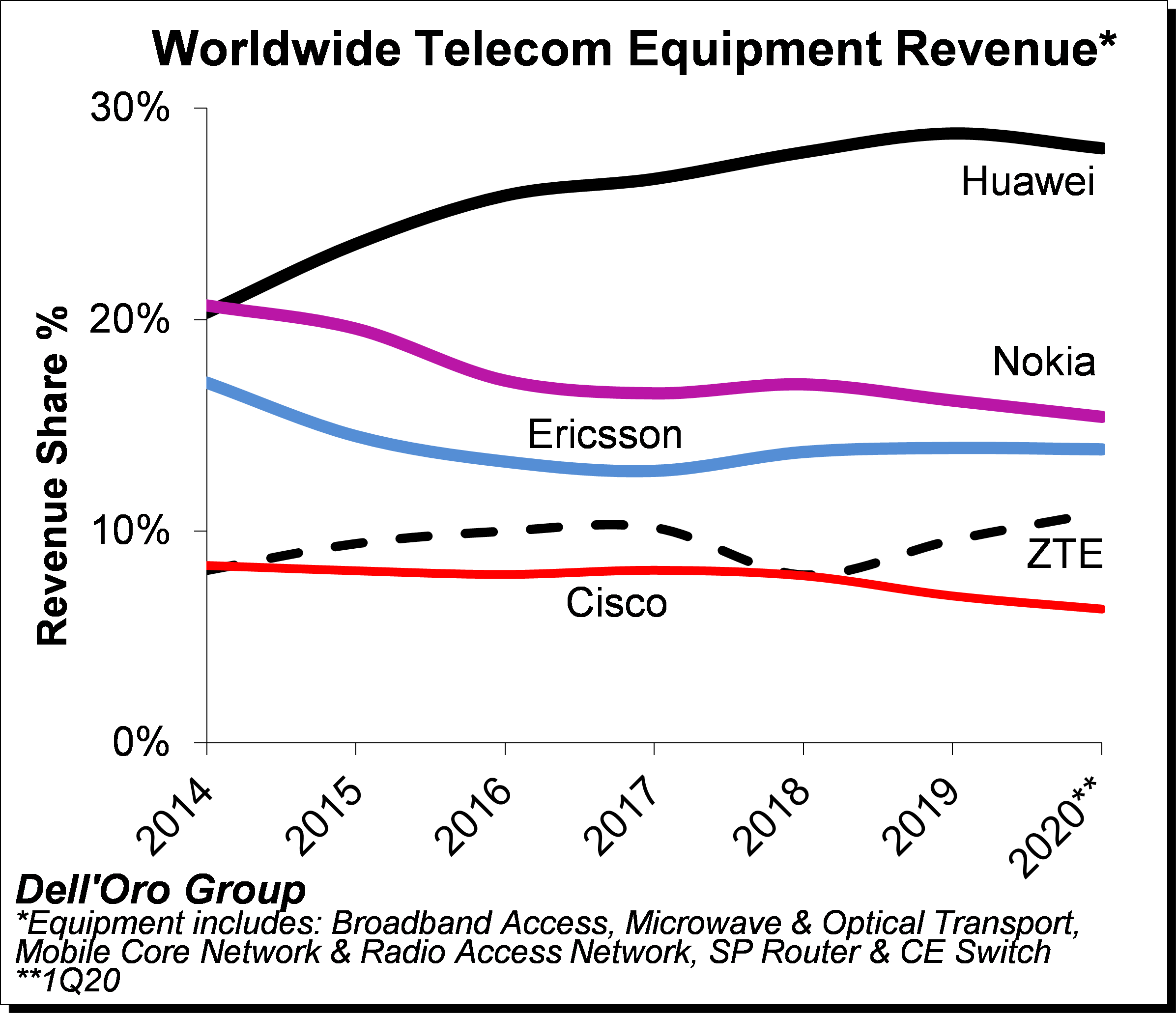

Cisco, Huawei, and Nokia’s revenue shares for the overall telecom equipment market declined in 1Q20 relative to full-year 2019 revenue shares

We just wrapped up the 1Q20 reporting period for all the Telecommunications Infrastructure programs covered at Dell’Oro Group. Preliminary estimates suggest the overall telecom equipment market – Broadband Access, Microwave & Optical Transport, Mobile Core & Radio Access Network, SP Router & CE Switch – declined 4% year-over-year (Y/Y), tracking slightly below the full-year 2020 growth projections of 1%.

Preliminary estimates suggest 1Q20 revenue shares relative to 2019 revenue shares for the top five suppliers – the latter indicated herein parenthesis – show that Huawei, Nokia, Ericsson, ZTE, and Cisco comprised 28% (29%), 15% (16%), 14% (14%), 11% (10%), 6% (7%), respectively.

Additional key takeaways from the 1Q20 reporting period include:

- Following two years of consecutive growth in 2018 and 2019, the overall telecom equipment market started the year on a weaker note, reflecting mixed market conditions as the positive market sentiment with mobile-related segments, including RAN and Core, was not enough to offset reduced demand for Broadband Access, Routers and CE Switch, and Optical/Microwave Transport.

- While healthy end-user fundamentals and positive 5G momentum outweighed downward risks associated with the COVID-19 pandemic for both RAN and Core investments, the pandemic had a more material impact on some of the non-wireless related segments, driven partly by supply chain disruptions and weakened demand as a result of increased macroeconomic uncertainty.

- Within the technology segments, Mobile RAN and Core revenues together advanced at a single-digit rate, accounting for nearly half of the overall telecom equipment market during 1Q20. At the same time, the combined revenues for Broadband Access, Microwave Transport, and Routers and CE Switch declined at a double-digit pace Y/Y, accounting for about a third of the overall market.

- In contrast to previous recessions, the COVID-19 slowdown is shifting and transforming the way we use the network. But a shift in how users are consuming data doesn’t necessarily result in a corresponding increase in spending on new infrastructure to support that traffic growth. Some suppliers and service providers indicated that network capacity upgrades were required to accommodate data traffic growth, however, traffic surges did not lead to significant demand for network capacity upgrades across all the telecom equipment segments.

- Even though the pandemic is still inflicting high human and economic losses, the Dell’Oro analyst team collectively expect market conditions and supply chain risks to be more favorable in the second half of 2020, propelling the overall telecom equipment market to advance 1% in 2020, reflecting a downward revision from the previous 2% growth outlook.

Dell’Oro Group telecommunication infrastructure research programs consist of the following: Broadband Access, Microwave Transmission & Mobile Backhaul, Mobile Core Networks, Mobile Radio Access Network, Optical Transport, and Service Provider (SP) Router & Carrier Ethernet Switch.

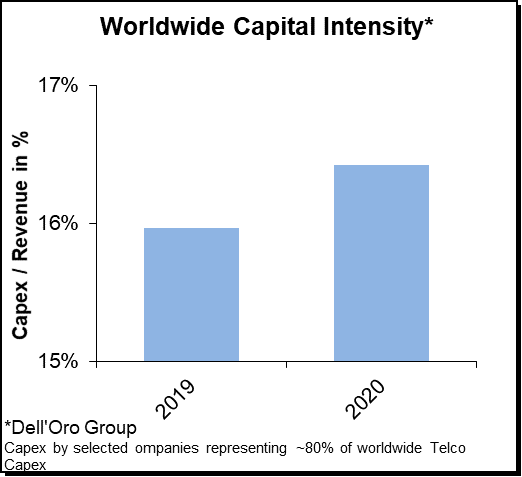

We recently updated the 2020 Telecom Capex Report. In this report, we analyze the relationships between wireless and wireline capex and revenue for more than 50 carriers, accounting for approximately 80% of worldwide capex and revenue. Given that the correlation between the equipment programs and telecom capital intensities remain significant, we believe there is value to study these trends. Some of the highlights from the report are shown below. For more info or if you need full access to the report, please contact dgsales@delloro.com.

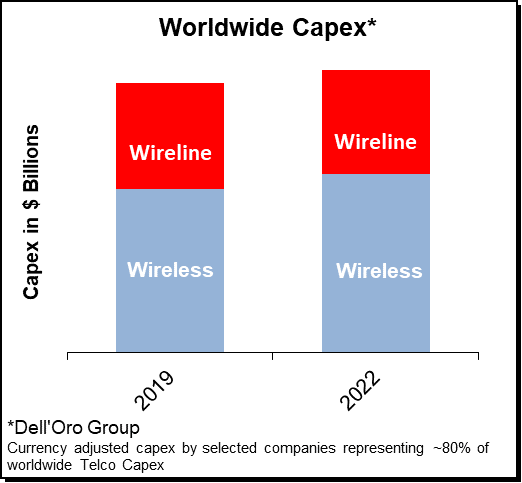

- Following three years of declining capex trends between 2015 and 2017 and flat trends in 2018, preliminary readings suggest that worldwide telecom capex—the sum of wireless and wireline telecom investments—increased 0% year-over-year (Y/Y) in nominal U.S Dollar (USD) and 2% in constant currency conditions.

The growth in capex was driven by stable demand for wireline capex and surging investments in wireless related technologies to accommodate the on-going shift from 4G to 5G. Wireless capex increased 1% Y/Y in nominal USD terms while currency adjusted wireless capex advanced 4% Y/Y. Initial estimates indicate currency adjusted wireline capex was flat in 2019.

The growth in capex was driven by stable demand for wireline capex and surging investments in wireless related technologies to accommodate the on-going shift from 4G to 5G. Wireless capex increased 1% Y/Y in nominal USD terms while currency adjusted wireless capex advanced 4% Y/Y. Initial estimates indicate currency adjusted wireline capex was flat in 2019.- The bulk of the capex growth can be attributed to increasing investments in the Asia Pacific (APAC) region, driven primarily by improving trends in China and surging capex growth South Korea. The data for the operators we track indicate 2019 capex advanced at a low-single digit rate Y/Y in the APAC region. At the same time, capex in nominal USD terms declined at a low-single digit rate in both North America and Europe.

- Preliminary vendor report estimates suggest that the combined revenues of the carrier-related equipment programs tracked by the Dell’Oro Group (Broadband Access, Microwave Transport, Mobile Core Network, Mobile RAN, Optical Transport, and Routers & CE Switches) increased approximately 2% in 2019, suggesting that the relationship between carrier capex and supplier infrastructure equipment revenues remained strong.

- Even as we are issuing this forecast in the middle of a pandemic, we have not made any material downward revisions, partly because we believe this recession is a bit different than previous recessions. While there are clearly some downside risks over the short-term, we also believe there could be some long-term positives. Global capex growth for the 2019-2022 period is projected to improve at a CAGR of 1% in nominal USD terms. We continue to forecast robust wireless capex growth for 2020, reflecting positive demand in the Asia Pacific region with wireless capex in China expected to advance 15% to 20%.

Preliminary guidance suggests 5G will drive more than 80% of the mobile network related capex in 2020 in China, underpinning projections that the operators will continue to rollout 5G at a torrid pace with the collective 5G BTS macro installed base eclipsing half a million by 2020.

Preliminary guidance suggests 5G will drive more than 80% of the mobile network related capex in 2020 in China, underpinning projections that the operators will continue to rollout 5G at a torrid pace with the collective 5G BTS macro installed base eclipsing half a million by 2020.- Even with AT&T’s expected capex pull-back in 2020, we project capex levels in the U.S. to remain stable over the forecast period—total U.S. capex (excluding T-Mobile/Sprint integration capex) is projected to remain elevated over the forecast period. The projected capex envelope for the U.S. telecom market assumes investments in mid-band capex will remain elevated, millimeter wave investments will increase, and low-band related capex will remain flat or decline.

- Global risks are broadly balanced. On the one hand, the fundamentals remain healthy with the on-going shift from 4G to 5G, healthy end user fundamentals, and the increased realization that broadband is an essential utility. Even so, we are issuing this forecast in the middle of a pandemic, and it is still early days to fully grasp the human and economic impact from COVID-19. So at this juncture, we envision there could be some albeit limited short-term capex downside due to the COVID-19. At the same time, there are still some practical short-term challenges as countries shut down for a couple of months impacting the supply chain and the ability to perform network upgrades and deploy new equipment. Medium to long-term, we envision COVID-19 could have a positive impact on capex. We are not downplaying the tragedy that the Coronavirus represents with immeasurable humans losses and massive economic losses. But we do believe COVID-19 has and will continue to expose the digital divide accelerating the need for businesses and governments to review their broadband plans to not only prepare for the next pandemic, but also to accelerate their digital transformation plans.

With virtual MWC coming to an end, we are sharing some of the RAN related highlights below. To access the entire summary, please contact Daisy@delloro.com.

COVID-19 – It is no longer just about the supply chain

When we updated the 2020 outlook in conjunction with the 4Q19 RAN report, we assessed the potential supply chain risks as a result of COVID-19. At the time, the suppliers were not overly concerned about their abilities to meet 2020 shipments. While this assessment still holds, the overall situation has evolved since we published the report. In addition to any potential supply chain risks, other variables to consider include:

- The broader impact on the markets, the economy, and the increased risk of a recession – significant changes in GDP output could impact capex.

- Impact on cellular data traffic as people cut down on commuting and social events and spend more time at home.

- The suppliers might figure out how to minimize supply chain risks, but even with differing revenue recognition practices, sooner or later someone needs to deploy the equipment in the appropriate location.

- Forex exchange movements could affect the RAN market in U.S. Dollar (USD) terms if tightening financial conditions and aggressive stimulus by the Federal Reserve will move the USD relative to the Euro, SEK, and the Yuan.

- Governments will likely try various stimulus packages. Tax incentives to spur capex growth could be on the table.

Massive MIMO – Strong focus on performance, bandwidth, weight, and power consumption

The Massive MIMO business case has changed rather significantly over the past two to three years with the technology now considered to be a foundational building block for mid-band NR deployments. And with Massive MIMO configured 5G NR systems accelerating at a much faster pace than expected in 2019 and the overall installed base now in the millions, it was not perhaps a major surprise that the technology for a second year in a row remained one of the leading RAN related MWC topics (MWC 2019 Massive MIMO blog, see link).

But what was interesting this year was the different focus among some of the leading suppliers with Huawei and ZTE focusing more on their respective bandwidth advantages while Ericsson and Nokia emphasized the performance benefits with their Massive MIMO systems.

Dynamic Spectrum Sharing (DSS) to play a pivotal role in 2020

DSS was a hot topic during vMWC, validating the message we have communicated for some time, namely that the technology will play a pivotal role in upgrading existing low-band LTE sites to NR in the second half of 2020—Verizon recently confirmed it will launch DSS nationwide in 2020. The timing for any operator that is considering DSS will in addition to device availability to some degree depend on their overall 5G strategy – is DSS a 5G logo, an improved experience, or a stepping stone towards something bigger.

As the operators are doing their best to differentiate their overall 5G strategies, some confusion is inevitable. And with T-Mobile publicly suggesting that DSS is not ready for prime time and the technology its current state would impact the overall capacity negatively, the leading vendors took some time to clarify the state and benefits with DSS. But the key point here is that there are only three ways to move from 4G to 5G with existing LTE spectrum (re-farming, static sharing, and DSS). And if we are going to discuss relative performance of DSS, Ericsson rightly pointed out that we need to compare apples-to-apples.

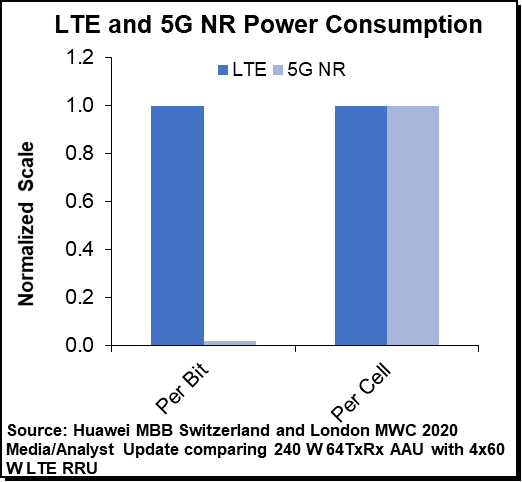

5G is more power efficient than LTE with comparable cell consumption

With operators ramping up 5G while still maintaining their legacy 2G-4G networks, the power consumption KPI appears to be moving up the priority list as operators are trying to ensure total 2G-5G cell site power consumption remains within reasonable power budgets.

With operators ramping up 5G while still maintaining their legacy 2G-4G networks, the power consumption KPI appears to be moving up the priority list as operators are trying to ensure total 2G-5G cell site power consumption remains within reasonable power budgets.

Since there is no shortage of media coverage suggesting 5G cell sites will be significantly more power hungry than 4G cell sites, the vendors have over the past year ramped up the engineering and marketing efforts with their 5G portfolios.

Huawei has on numerous occasions discussed the 25x to 50x (future 100x) power consumption per bit advantage between 5G NR and LTE while acknowledging that the overall NR cell consumption could be slightly higher. And now, partly due to continued channel, carrier, and symbol shutdown advancements, Huawei announced that the total power budget between NR and LTE is comparable when comparing the 64TxRx AAU with the 4×60 W LTE RRU.

Virtual and Open RAN gain momentum

There are multiple ongoing RAN virtualization efforts driven both by operators and suppliers with the primary objective of realizing a more flexible architecture with uniform hardware platforms that will optimize TCO and service differentiation for both the known and unknown use cases.

Given the current progress and the overall readiness with both the Open RAN and Non Open RAN virtualization tracks, we anticipate that the benefits with purpose built RAN will continue to outweigh the benefits with Virtual RAN over the near-term.

At the same time, the Open RAN momentum is moving in the right direction as the ecosystem develops, partnerships are forming, suppliers are ramping up investments, and operators are committing and experimenting with trials.

TIP announced a project targeting commercial multi-band radios by 2021 in the $1 K range. Even if the RAN is a relatively small portion of the overall site TCO, this cost structure is clearly compelling and would go a long way offsetting higher baseband compute costs typically associated with general purpose solutions.

For more details about the shift towards virtualized and Open RAN, please see separate blog.

For full blog access, please contact daisy@delloro.com.