We’ve just wrapped up the 4Q20 reporting period for Dell’Oro Group’s Enterprise Network Equipment programs, which include Campus Switches, Enterprise Data Center Switches, SD-WAN & Enterprise Routers, Network Security, and Wireless LAN. Enterprises include businesses of all sizes as well as government, education, and research entities. The equipment tracked in these programs can be used for wired or wireless data communication in private and secure networks.

2020 Market Performance

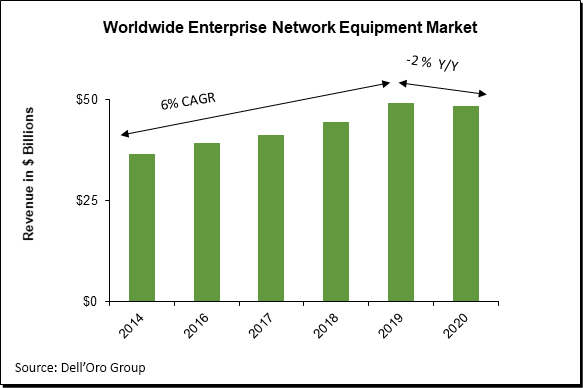

Our reports suggest that the overall Enterprise Network Equipment market declined 2% year over year (Y/Y) for full-year 2020 to $48.5 B as a result of the COVID-19 pandemic. This is a significant departure from the 6% CAGR achieved from 2014 to 2019.

The decline was driven mostly by campus and data center switches. In the meantime, enterprise spending was up on both routers and security and it was flat on Wireless LAN. What’s interesting is that growth in routers and security was actually driven by software and subscription-based products (SD-WAN and virtual and SaaS security). Even within Wireless LAN, we saw growth in controllers and licenses. In the meantime, spending declined on hardware products (access routers, physical firewall, Wireless LAN access points, and Ethernet switches).

The softness in the total Enterprise Network Equipment market was more pronounced in the first half of the year. However, starting in 3Q20, spending on network equipment began to recover, as enterprises showed confidence investing for the future. Government stimulus around the world was also a major factor. Additionally, what caught our attention is the spread across various technologies of this increase in spending. We calculated that enterprises increased their spending on network equipment by about $400 M in 2H20 (compared to 2H19), about 70% of which was allocated to Wireless LAN.

2020 Vendor Landscape

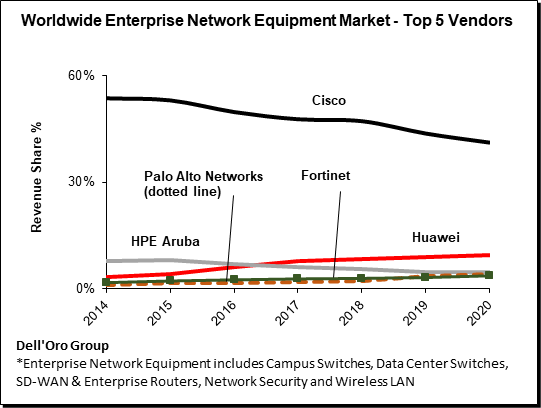

From a vendor perspective, Huawei and Cisco composed about 50% of the Enterprise Network Equipment market in 2020; they were the only two vendors with more than 10% revenue share in the Enterprise Network Equipment market.

Cisco remained the market leader in all segments. However, the company saw revenue-share loss in 2020 due to high exposure to hardware-based products and low exposure to China, which outgrew the market during the pandemic.

In the meantime, Fortinet climbed to fifth place, displacing H3C. Fortinet has high exposure to the security market, while H3C has high exposure to the switching market. Since security performed better than switching in 2020, it helped Fortinet gain share and improve its ranking in 2020.

| Top 9 Vendors | 2019 | 2020 |

| CISCO | 44% | 41% |

| HUAWEI | 9% | 10% |

| HPE ARUBA | 5% | 5% |

| PALO ALTO NETWORKS | 4% | 4% |

| FORTINET | 3% | 4% |

| H3C | 3% | 4% |

| JUNIPER | 2% | 2% |

| CHECK POINT | 2% | 2% |

| SYMANTEC / BLUE COAT | 2% | 2% |

2021 Market Outlook

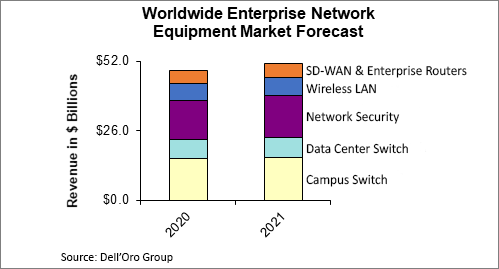

Dell’Oro analysts remain optimistic about the 2021 outlook and forecast 5% growth for the total Enterprise Network Equipment Market. This optimism is prompted by improving macro-economic conditions and business confidence as well as the ongoing government stimulus. Additionally, our interviews with end-users, system integrators, and value-added resellers (VARs) revealed that if a portion of the workforce returns to work by the end of 2021, spending on network infrastructure in preparation for such a development should start a few months in advance, perhaps as early as 2Q21 or 3Q21.

Dell’Oro Group Enterprise Network Equipment research programs consist of the following: Campus switches, Enterprise Data Center Switches, SD-WAN & Enterprise Routers, Network Security and Wireless LAN.

Related blogs for 5-year Forecast Jan 2021:

In our latest forecast published in January 2021, revenue for the worldwide Ethernet controller and adapter market is projected to increase at a 3% compound annual growth rate (CAGR) from 2020 to 2025 to $2.7 billion.

This market is characterized by speed transitions. We project during our forecast horizon, the majority of the Cloud and Enterprise server market will upgrade port speeds from 10 Gbps to 25 Gbps, with a growth of 25 Gbps leveling by 2025. Newer technologies, Smart NICs and 100 Gbps Ethernet, and to a lesser extent, 50 Gbps, with CAGR growing strong double-digits by 2025, fueling market growth opportunities.

- As the Tier 1 Cloud service providers refresh their networks, we anticipate an upgrade in server connectivity to 100 Gbps, based on PAM-4 SerDes, for general-purpose workloads. High-end workloads such as high-performance computing, accelerated computing, and all-flash arrays, will also benefit with 100 Gbps connectivity across all customer types.

- Smart NICs, also referred to as data processing units (DPU), are also gaining traction, with numerous product introductions in 2020. Smart NICs are generally equipped with a programmable processor, such as an ARM-based SoC or FPGA; onboard memory and storage; operating system; and high-speed I/O, and offer various offload and security benefits. In 2020, the Top 4 US Cloud SPs comprised the vast majority share of the Smart NIC port shipments. By 2025, however, we expect Smart NICs to expand in customer segments outside of the Top 4 US Cloud, reaching a third of the Smart NIC port shipments. Due to the higher price premium of Smart NICs over that of traditional NICs, we anticipate that the impacts of Smart NICs on market revenue could be significant. We also predict that 100 Gbps will be the connectivity of choice for Smart NICs.

- While the growth of 25 Gbps will continue to moderate and reach maturity during our forecast horizon, 25 Gbps will likely be widely adopted and become the primary revenue contributor. We forecast 25 Gbps to comprise 38% of the cumulative market revenue by 2025.

We believe that these advances in server network connectivity will enable the major Cloud service providers to continue to scale their networks, and drive the adoption of bandwidth-hungry AI applications.

To learn more about the Ethernet Controller and Adapter market, or if you need to access the full report, please contact us at dgsales@delloro.com.

|

About the Report

About the Report

Dell’Oro Group just published an updated forecast for the enterprise Wireless LAN (WLAN) market, and expects demand to be robust over the next five years, growing to almost $9 B, as Wi-Fi becomes the default connectivity option for users and devices. In spite of a severe worldwide economic downturn, the enterprise WLAN market has proven remarkably resilient in 2020—revenue is on track to decline modestly supported by remarkable government stimulus that became available in 3Q20. We estimate government funding to grow to a disproportionate portion in 2021, which means the magnitude and duration of funding could move the market significantly.

One of the big winners in 2020 was cloud-managed WLAN: adoption of cloud-managed Wi-Fi access points jumped by 6 points in 2020 as the pandemic triggered interest in remote management capabilities, given the difficulty of visiting locations in person. However, going forward, we don’t expect this surge to continue, rather we expect adoption to grow at a more moderate pace as businesses balance the need to manage a distributed network with the desire to maintain control over their data. Issues such as high priced egress fees, and disputes over who owns the data have emerged and need to be resolved.

We were surprised to learn enterprise class Wi-Fi 6E access points are planned for the summer of 2021, as most vendors we spoke with were planning six-to-nine months later. Another surprise was the first products will be 2×2 rather than 4×4. Lower-end products spearheading a technology transition is different from previous technology introductions, and has a huge implication on market penetration, and moving the market. The obvious first impact could be users delaying purchases as they wait for 6E products from their favorite supplier, with the most notable pause coming from the high-end and high portion of the midrange market. We forecast 6E to fuel the market growth through the forecast horizon.

Our discussions with system integrators indicate a notable increase in deployments of competitive wireless technologies (5G, private cellular, Broadband Fixed Wireless) in 2020, particularly from schools and municipalities connecting constituents during the pandemic. We believe the impact on the WLAN market will be limited, as Wi-Fi is not a good fit for these types of deployments due to range, and coverage requirements. There is an opportunity for vendors to build network management systems that bring these different networking technologies together under one roof.

In sum, we address factors suppressing as well as accelerating the WLAN market in our forecast report. One of the main drivers of traffic and network upgrades—the growth engine—is people returning to work.

About the Report

|

Campus switches are used for the purpose of connecting users and devices to the corporate Local Area Network (LAN). With the Work from Home or from Anywhere predicted to become a permanent aspect of the future of work, one of the fundamental questions is whether there is room for growth in the campus switch market. And if so- where will this growth come from?

We just published the latest edition of our 5-year forecast for the campus switch market. In the report, we discuss some of the negative impact from the pandemic such as the following:

-

- Downward pressure on the number of campus switch ports needed to be installed: A more distributed workforce, working remotely either from home or from smaller distributed office spaces, will negatively impact the number of switch ports needed in those campuses. Initial data on commercial real estate, for example, suggests that prices are expected to fall significantly in 2020 and 2021 as demand for new office buildings is suppressed, which will in turn affect demand for campus switches.

- Further cannibalization from WLAN: We expect WLAN to become more favorable for user connectivity than wired Ethernet, as it supports features and services that help businesses comply with re-opening guidelines, such as contact tracing, people counting, and other location-based services. Additionally, our interviews revealed that companies need to provide real mobility to the employees working from home. When these employees return to their offices, even in smaller numbers, their companies want to connect these users via Wi-Fi, as well, so as to maximize use of office space.

Despite the potential downside risk from COVID-19, we expect that the pandemic will also have some upside impact that will drive the market recovery, as detailed below:

-

- Accelerated pace of digital transformation initiatives: Our interviews revealed that customers may be putting many budgets on hold, except for automation. We also learned that the timeline of some of these automation and digital transformation projects has been pulled in by about one to two years. Although the majority of IoT devices will be on wireless, some devices such as security cameras, industrial lighting or some sensors are expected to remain on wired Ethernet.

- A greater portion of higher-priced PoE devices: We expect IoT devices to drive an increased portion of the higher-priced PoE ports. We expect this trend to help boost market average selling prices (ASPs).

- Accelerated pace of the campus switch refresh cycle: We expect the adoption of digital transformation to accelerate the pace of the campus switch refresh cycle. In order to enable digital transformation, the network must undergo numerous changes. Automation, security, visibility, and analytics/intelligence are several added functionalities that IT managers need for the new digital era.

Any other impact from the pandemic on the campus switch market?

The pandemic is also expected to accelerate the adoption of Cloud-managed switches to accommodate the distributed workforce. Additionally, our interviews with end-users, system integrators, and VARs revealed an increased interest in Network as a Service (NaaS) during the pandemic, an interest that is expected to persist even after the pandemic ends.

If you need to access the full report to obtain revenue, units, pricing, relevant segmentation including regions and vertical markets, etc., please contact us at dgsales@delloro.com.

About the Report

|