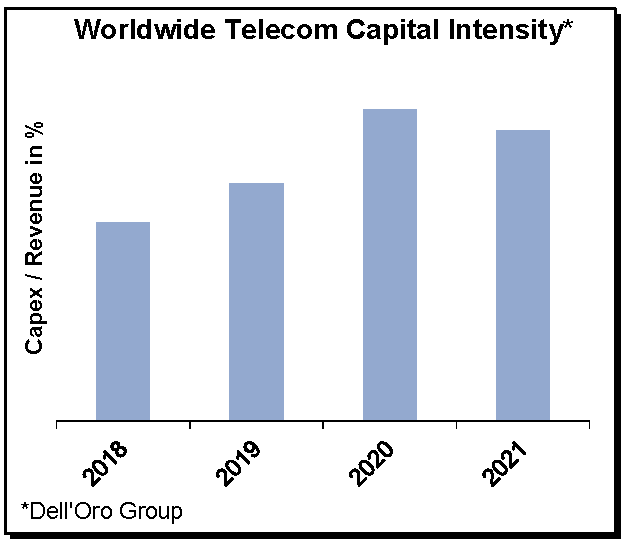

The latest Dell’Oro Group Telecom Capex 2H18 Report (former name is Carrier Economics report) supports the thesis the firm has communicated with its technology equipment forecasts, namely, there are reasons to be optimistic about the telecom sector. Following three years of declining capex trends between 2015 and 2017, and more stable trends in 2018, the report showed that capex growth will outpace operator revenue growth over the next three years, reflecting operators increased focus on rolling out 5G.

“While the relationship between capex/revenue will likely remain strong over time and constrained operator revenue growth will be one of the primary inhibitors of further telecom capex acceleration, we remain optimistic that there will be some deviation in the short-term to accommodate the rollout of 5G,” said Stefan Pongratz, Senior Director at Dell’Oro Group. “And with the preliminary 5G capex guidance coming in stronger than expected, there is a lot of excitement right now about the potential 5G capex ramp,” continued Pongratz.

Followings are additional highlights from the Telecom Capex 2H18 Report:

Currency adjusted telecom capex is expected to grow both in 2019 and over the next three years.

Wireless investments are projected to grow at a faster pace than wireline capex over the forecast period – growing at a low single-digit CAGR.

5G revenue growth is not expected to reverse aggregate smartphone ARPU trends over the forecast period.

The Dell’Oro Group Telecom Capex Report provides in-depth coverage of the revenue, capex, and capital intensity outlook for about 50 operators. The report provides actual and forecasts details by the carrier, by region by country (United States, Canada, China, India, Japan, and South Korea), and by technology (wireless/wireline). For more information about the report, please contact dgsales@delloro.com.

[wp_tech_share]

In March, I attended the 2019 Open Compute Project (OCP) Global Summit at the San Jose Convention Center. The event is growing with 3,600 participants this year, including a broad representation of vendors and end users who make up the OCP community. We continue to see innovation in the server rack for hyperscale Cloud, edge computing, and enterprise environments for OCP-based designs.

Following are three key takeaways in server network connectivity:

1. OCP NIC 3.0 (Network Interface Card) specification continues to evolve and is Smart NIC-ready.

The OCP NIC 3.0 specification addresses shortcomings of the OCP NIC 2.0 specification in the areas of the thermal and mechanical profile, connector placement, and board space. Key members, including Broadcom, Facebook, Intel, and Mellanox, contributed to the 3.0 development process. As it currently stands, the OCP NIC 3.0 specification is defined in two form factors: SFF (small form factor) and LFF (large form factor). The LFF form factor is designed to accommodate accelerated processors, such as an ARM SoC or FPGA for Smart NIC applications.

A Smart NIC designed for OCP is a wise future-proofing strategy. In Dell’Oro Group’s 2019 Controller and Adapter Market 5-Year Forecast January report, I projected that Smart NIC will become a $500 M market by 2023, representing 20 percent of the total controller and adapter market. Furthermore, most of the earlier adopters of Smart NICs are hyperscale and telecom data centers are also expected to widely deploy OCP-based designs within the server rack.

2. The introduction of 56 Gbps PAM-4 NICs enables server connectivity to 400 Gbps networks.

Another important development is the availability of Ethernet adapter products with 56 Gbps PAM-4 SerDes lanes by Broadcom (NetExtreme), Intel (800 series Columbiaville), and Mellanox (ConnectX6). All are available in the OCP 3.0 form factor. The SerDes lane transition from 28 Gbps NRZ to 56 Gbps PAM-4 will enable Ethernet connectivity up to 100 GbE (based on 2 SerDes lanes) or 200 GbE (based on 4 SerDes lanes). We see strong demand for server connectivity at 100 GbE and higher speeds, especially by Tier 1 Cloud service providers, as this segment transitions to 400 GbE networking at the top-of-rack (ToR) switch over the next one to two years. (See Dell’Oro’s press release,“Cloud Service Providers Drove Demand Volatility of High-Speed Network Adapters”)

3. Multi-host NICs have the potential to streamline and densify server connector connectivity.

It is exciting to see multi-host NICs gaining additional support from vendors. This technology has the ability to streamline the network by reducing ToR connections while providing a dense compute rack architecture. Mellanox was first to market with multi-host NICs for Yosemite servers, which provide 50 Gbps Ethernet connectivity to four server nodes. At OCP, both Broadcom and Netronome announced network adapter products supporting multi-host connectivity for the Yosemite platform. Broadcom’s announcements are based on the NetExterme series with the Thor chipset, which provides single and multi-host connectivity for up to 200 GbE with a PAM-4 solution. Netronome’s solution, the Agilio CX, is also a Smart NIC that provides connectivity up to 50 GbE.

I believe that OCP will continue to grow in strength as the industry transitions from off-the-shelf equipment to open designs optimized to end-users’ technical and cost-of-ownership requirements.

[wp_tech_share]

The infrastructure of the cloud—data centers and the computer and networking systems resources housed within—is expanding rapidly as the demand for cloud services spreads globally. The traffic between data centers, as well as traffic into and out of the cloud, is expected to grow strongly, placing pressure on the data center interconnect (DCI) networks used to connect the data centers.

[wp_tech_share]

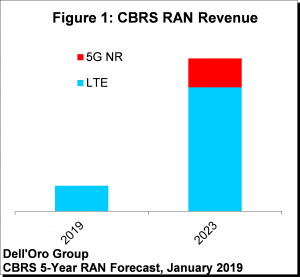

According to the Dell’Oro Group CBRS RAN 5-year January Forecast Report, short term delays will not impact the long-term demand for LTE and 5G NR CBRS solutions – the overall CBRS RAN market is expected to grow at a rapid pace between 2019 and 2023 with cumulative investments surpassing $1 B over the next five years.

“We continue to believe the CBRS band with its unique spectrum sharing characteristics include many of the right ingredients to change the status quo about how networks are built,” said Stefan Pongratz, senior director at Dell’Oro Group. “And recent announcement by the CBRS Alliance to support OnGo over 5G underpins projections that 5G NR deployments in the CBRS band are set to accelerate in the outer part of the forecast period,” continued Pongratz.

Followings are additional highlights from the CBRS 5-Year Forecast January Report (2019 to 2023):

CBRS capex is not projected to have a significant impact on the WLAN capex.

CBRS investments are projected to account for more than a fifth of the U.S small cell market by the outer part of the forecast period.

FWA is projected to drive the lion share of the CBRS capex over the near-term.

This blog post is a summary of RAN-related key takeaways from MWC 2019 Barcelona. For access to the full version, please contact daisy@delloro.com

RAN Optimism

The MWC event supported the premise we have communicated for some time that there are convincing reasons to be optimistic about the RAN market. One of the show’s key findings was a strong consensus that 2019 will be another solid year for the RAN market driven by growth in China, Korea, and the U.S.

While we have already projected that 5G NR would accelerate rapidly in 2019, key findings at the show increase our confidence level that 5G NR shipments and revenues will be material in 2019. We discuss the mobile infrastructure market’s 2018 performance in this press release.

Massive MIMO

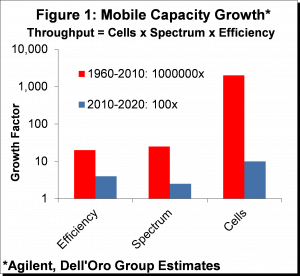

Another key takeaway from MWC2019 was the strong focus on Massive MIMO. This increased confidence in the upwardly adjusted Massive MIMO projections we outlined in conjunction with recently published Mobile RAN reports. Given that operators have multiple tools in their toolkit to manage capacity (Figure 1), why are we so optimistic about the Massive MIMO opportunity in the sub 6 GHz spectrum? Learn more about Massive MIMO at Barcelona in this article.

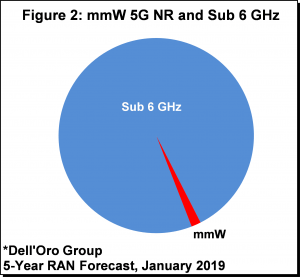

Millimeter Wave

The Millimeter Wave (mmW) narrative has morphed somewhat over the past couple of years with the industry sentiment fluctuating about the role mmW will play for mobile applications. Even though the opportunity cost for operators with significant mid-band assets will be more favorable for

some time leveraging the macro grid and Massive MIMO, our view has always been that mmW will be an important technology over the long-term (there is no fourth alternative in Figure 1).

The most important takeaways from the event include: 1) mmW is now real, phones are coming to the market, and mmW shipments will be material in 2019, 2) The perception about Qualcomm’s mmW simulation is changing, 3) Findings validate our short-term and long-term forecast.

A summary of the latest Mobile RAN five-year forecast may be found here.

Open and Virtual RAN

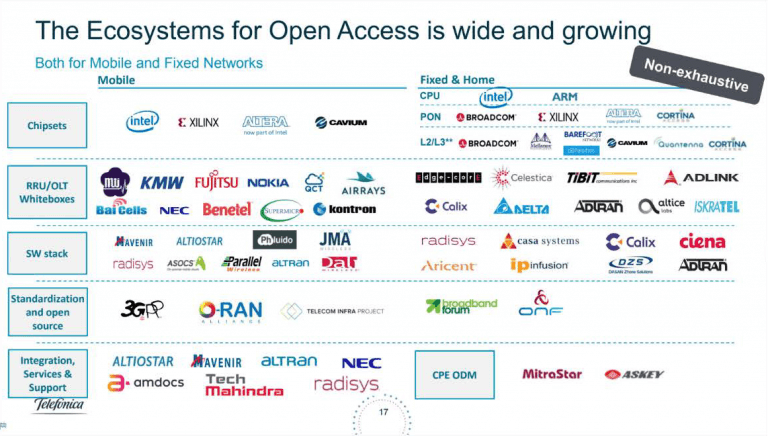

In general good momentum during the show behind the shift towards opening up the RAN and moving away from proprietary hardware with Rakuten communicating its C-RAN (Cloud Radio Access Network) progress in Japan, Ericsson recently joining the ORAN Alliance, and Telefonica sharing its roadmap and ecosystem partners for Open Access – which did not include the larger macro RAN vendors for the SW stack or the radios.

Source: Telefónica

While there is no doubt that virtual RAN sceptics will be monitoring Rakuten’s performance when the company goes to live with its 5500 sites this fall, it remains to be seen how well true C-RAN systems will handle—for example, a site with 64T64R 100 MHz BW Massive MIMO systems, along with legacy 2G/4G systems.

To some degree, the event reminded both virtual and proprietary HW RAN proponents that both sides have something to bring to the table. Open RAN and Virtual RAN are making significant headway and there is excitement about this progress. However, the event did little to convince us of our long-standing thesis—that the shift toward RAN virtualization will eventually occur—but it will take time. Moreover, initially, it will be confined to non-traditional builds, e.g., new use cases, indoor deployments, greenfield deployments, and rural settings. Finally, after such deployments, it will need to be revised.

CBRS

The key takeaway from a CBRS perspective is the reduced risk that regulatory delays could eventually impact the ecosystem. With Pixel 3 and Galaxy S10 now supporting the CBRS band, the ecosystem will undoubtedly get a boost. In addition to Qualcomm’s Snapdragon X20/24, Sierra Wireless and Sequans Cassiopeia now also have production-grade modules.

Our CBRS forecast report, which suggests that will grow at a rapid pace between 2018 and 2022 with total RAN investments approaching $1 Billion and CBRS RAN shipments to eclipse half a million units. Learn more from my blog on the CBRS RAN market.

Subscribe to Dell'Oro Group's Hot Topics news feed for the latest details on market trends in the telecommunications, data center, and enterprise networks infrastructure spaces.

with its technology equipment forecasts, namely, there are reasons to be optimistic about the telecom sector. Following three years of declining capex trends between 2015 and 2017, and more stable trends in 2018, the report showed that capex growth will outpace operator revenue growth over the next three years, reflecting operators increased focus on rolling out 5G.

with its technology equipment forecasts, namely, there are reasons to be optimistic about the telecom sector. Following three years of declining capex trends between 2015 and 2017, and more stable trends in 2018, the report showed that capex growth will outpace operator revenue growth over the next three years, reflecting operators increased focus on rolling out 5G. overall CBRS RAN market is expected to grow at a rapid pace between 2019 and 2023 with cumulative investments surpassing $1 B over the next five years.

overall CBRS RAN market is expected to grow at a rapid pace between 2019 and 2023 with cumulative investments surpassing $1 B over the next five years.