Importance of Optical Transport

When asked to explain optical transport, people usually use automobiles and roads as an example. A person can reach their destination faster in a sports car than in a sedan since the former can travel at higher speeds. Adding more lanes reduces traffic or congestion, allowing vehicles to reach their destination on time without delay. These examples, using cars and roadways, are analogous to optical wavelength signal speed and dense wavelength-division multiplexing (DWDM). While this metaphor is a great way to explain the purpose of DWDM technology, it fails to capture the importance.

I like to use trees to illustrate the importance of optical transport. Beneath every tree lies roots that ferry resources to the branches and leaves and must scale proportionally. If the root system is inadequate, the branches won’t receive enough nutrients and will eventually break. In general, the bigger and more stable the roots, the stronger and healthier the tree, as realized by the many healthy branches and leaves that we see.

In a service provider network, the optical transport layer plays a crucial role. It serves as the roots of a tree that supports all the branches of services offered to customers. Just as tree roots provide the necessary nutrients for healthy growth, the optical transport layer ensures better connectivity to homes, mobile devices, enterprises, and data centers. It needs to be robust enough to support all the services that operators want to deliver. Otherwise, the branch will break. Stated another way—like a tree, the customers see the branches, but they experience the network beneath it through its beauty.

Therefore, like a tree, with each new generation of access technology, there is a need for a new generation of optical transport. I bring this to your attention because of the visible work by service providers to roll out next-generation services, such as Mobile 5G Advanced and Fixed 5G Advanced (F5G Advanced), and enterprise investments in developing new applications using artificial intelligence and machine learning (AI/ML). These buzzword access technologies will need a matching optical transport layer to support the resources they need.

Next-Generation Services

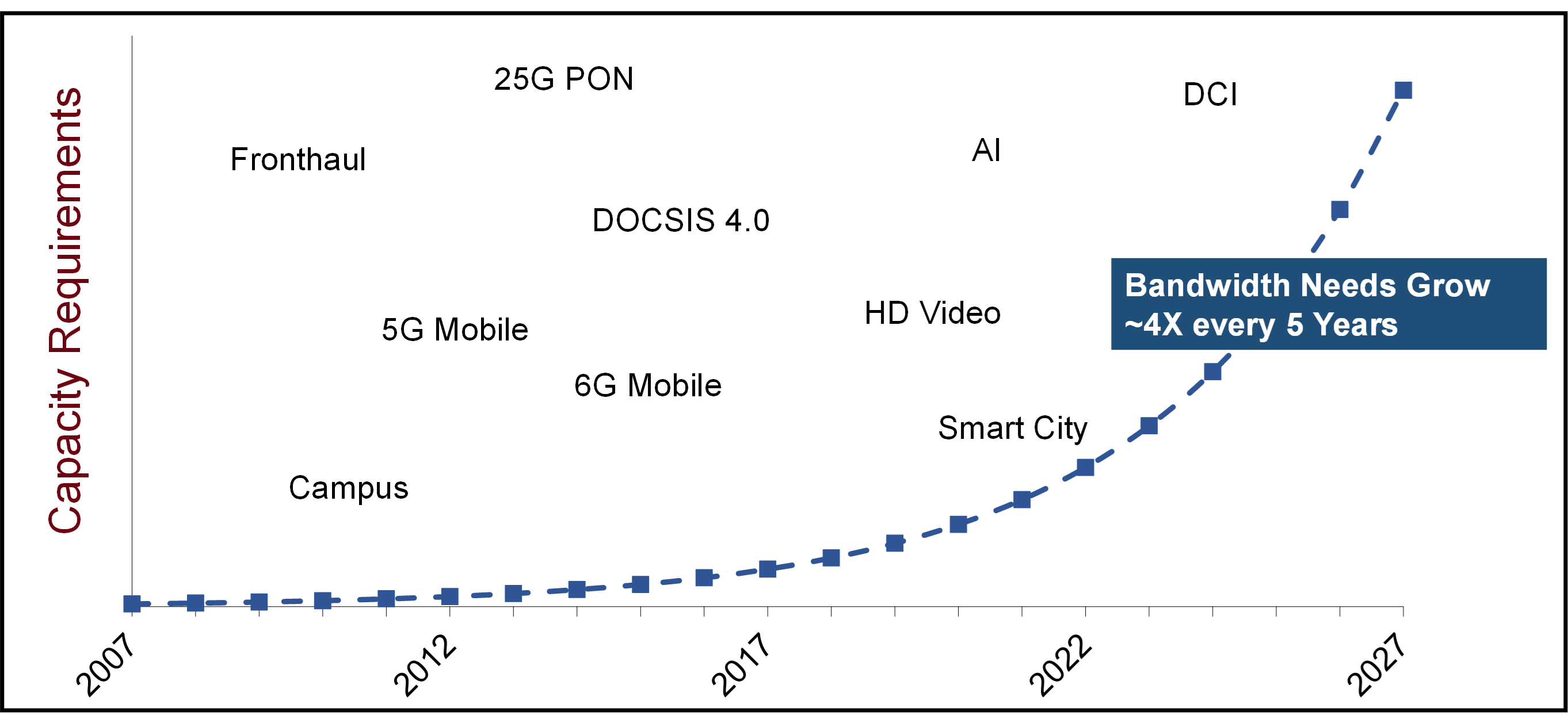

Access is moving to a new generation of services that deliver higher speeds, lower latency, and greater reliability. Some of these service offerings include 50 Gbps PON to homes, 5G-Advanced to devices, and ultra-high-speed connections between AI/ML data centers. In some cases, the bandwidth at the network edge will need to double, and in many cases, it will need to increase by over 10 times. For example, in residential broadband, the market is moving from the current technology (2.5 Gbps PON) to 10 Gbps and then 50 Gbps PON. This means the backhaul capacity may need to increase by as much as 20x.

In addition, the applications run by end users over their network will determine the speed and architecture required by the service provider to meet consumer expectations on quality and latency. Imagine a customer with a broadband service of 10 Gbps using the operator’s 50 Gbps PON network playing a virtual reality game with the same latency and service quality as before. Was the higher price for the 10 Gbps connection worth it? Will they keep it? The answer is “no” to both. And while we do not know what applications and services will emerge from AI/ML, we do know they will require more bandwidth, ultra-low latency, and much higher network quality. Additionally, due to the higher power consumption of AI/ML systems, data centers are required to be geographically distributed and interconnected (DCI) with a high-speed, high-availability optical network.

Therefore, beyond the new generation of access technology, the optical transport layer must also be upgraded to match it. The roots of the tree must grow to support the bigger branches.

Next-Generation Optical Transport

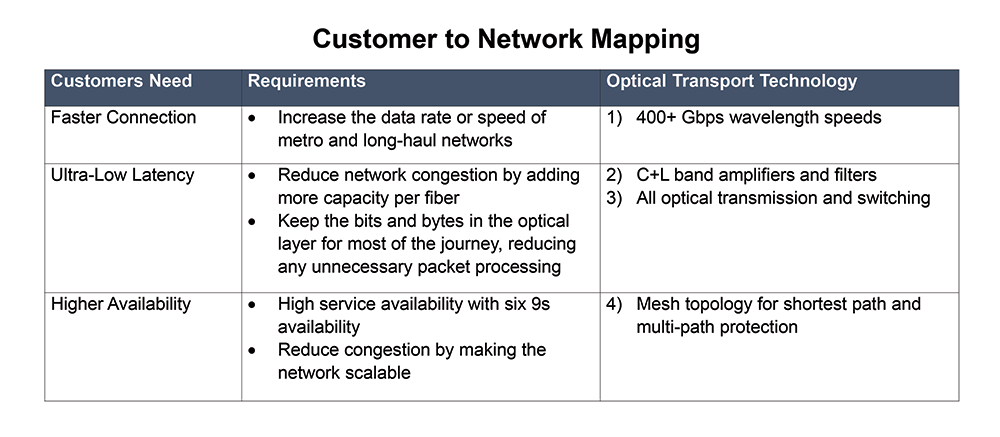

What are the requirements for the next-generation optical transport network? To answer this, we listed some key optical network technologies that are mapped to critical customer needs.

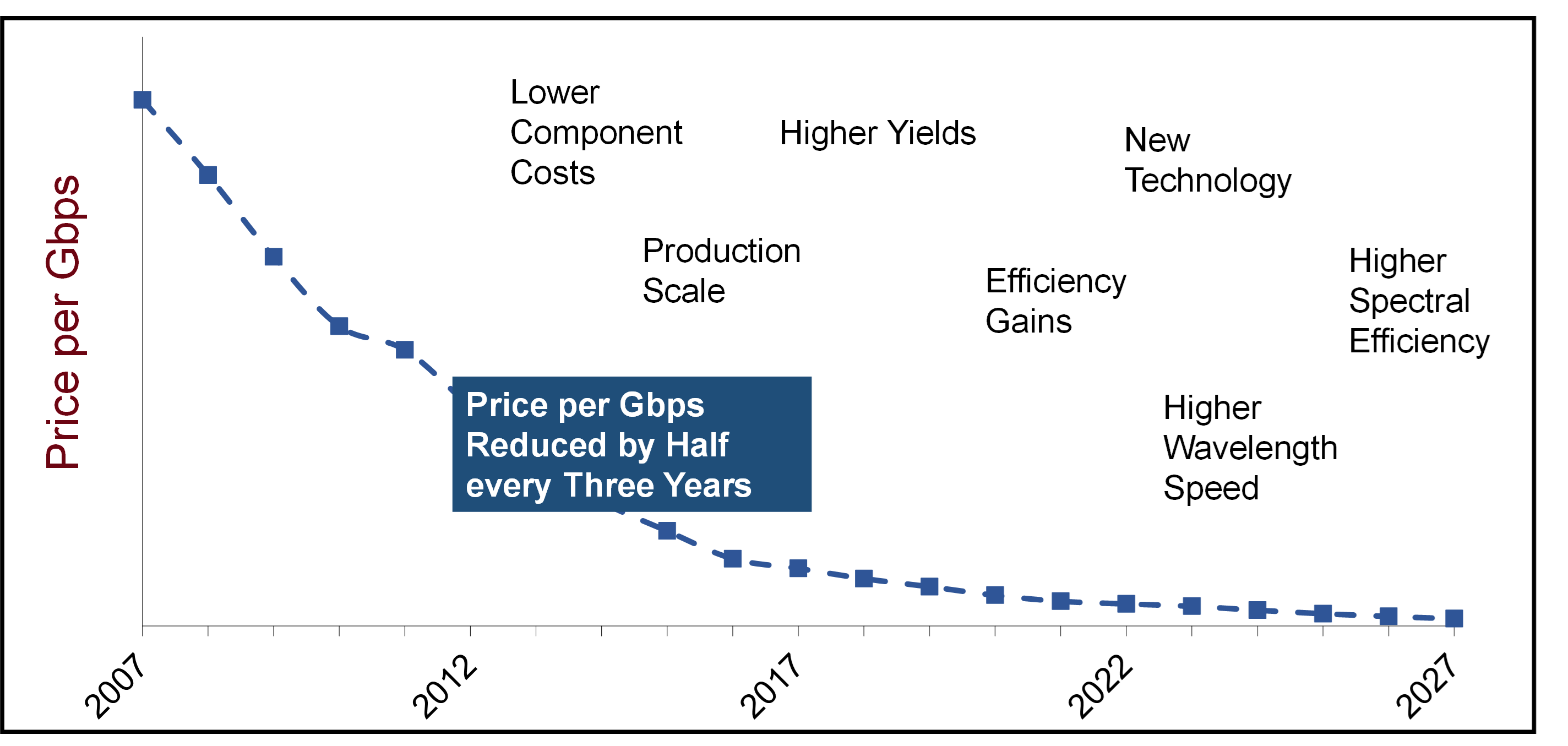

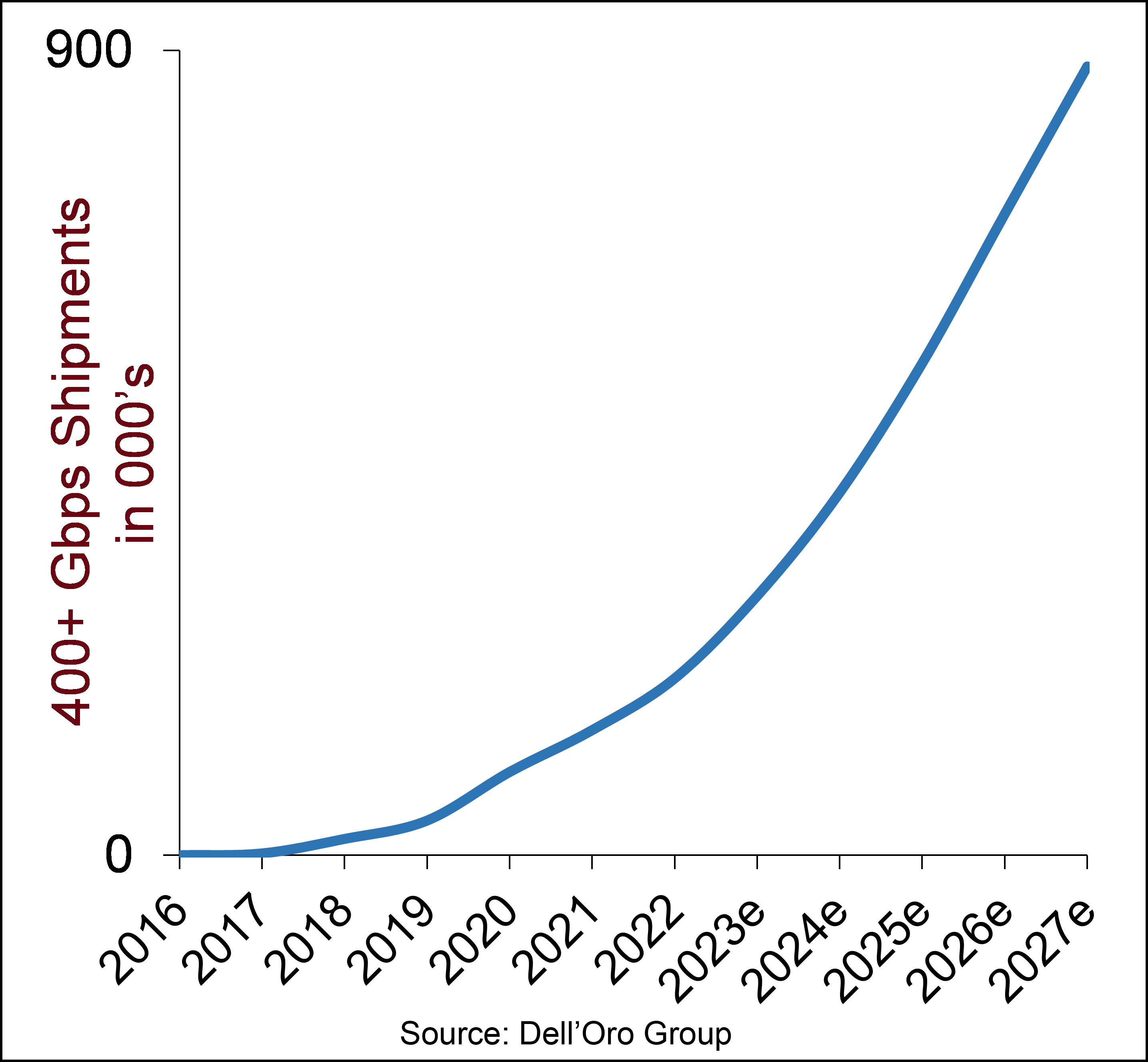

(1) 400+ Gbps wavelength speeds: End users want faster connections to their devices, using new broadband access technologies that require higher backhaul speeds. Therefore, the transceiver speed in the aggregation, metro, and long-haul network will need to increase beyond the installed base of 100/200 Gbps. The optical transport network will need to move to at least 400 Gbps wavelengths and, ultimately, 800 Gbps to support the higher load placed on the network. Additionally, there are many benefits to moving to 400+ Gbps wavelengths, including higher network efficiency, less rack space, lower power per bit, and lower cost per bit.

(1) 400+ Gbps wavelength speeds: End users want faster connections to their devices, using new broadband access technologies that require higher backhaul speeds. Therefore, the transceiver speed in the aggregation, metro, and long-haul network will need to increase beyond the installed base of 100/200 Gbps. The optical transport network will need to move to at least 400 Gbps wavelengths and, ultimately, 800 Gbps to support the higher load placed on the network. Additionally, there are many benefits to moving to 400+ Gbps wavelengths, including higher network efficiency, less rack space, lower power per bit, and lower cost per bit.

(2) C+L band amplifiers and filters: Two factors heighten the need to increase the capacity per fiber. The first is that demand for bandwidth has risen every year since the beginning of the Internet era, and it will continue to rise for many more years into the future. The second reason is that, because of Shannon’s Limit, every new generation of wavelength speeds utilizes higher baud rates, consuming more spectrum. As a result of these factors, operators need fiber strands to carry more capacity. Otherwise, they will need to add more strands of fiber, which may not be possible, causing network congestion along some routes. The solution is to add more usable spectrum in a fiber.

Originally, optical equipment was designed to operate in 4 THz (80 channels @ 50 GHz) of fiber spectrum located in the C-band. Over time, equipment manufacturers increased it to 4.8 THz (96 channels @ 50 GHz). The next generation of equipment will inevitably be designed to operate in 6.0 THz (120 channels @ 50 GHz) of spectrum, referred to as Super C-band. This action alone increases the amount of bandwidth-per-fiber by 25 percent. The spectrum can be nearly doubled by adding L-band, which supports 100 channels @ 50 GHz. Consequently, a fiber that had a maximum capacity of 38.4 Tbps (calculated using a spectral efficiency of eight) can now support 88.0 Tbps.

(3) All optical transmission and switching: The speed of transmission is important, but for some applications that require real-time response and feedback, latency is critical. We mentioned gaming as one application for consumers, but there are numerous additional applications in industries such as medical, power utility, automotive, and aerospace, where lower latency is a major requirement. One way to improve or lower latency is to remove any points along the signal’s route where it must be read, processed, buffered, or converted to electrical and then back to optical. Hence, the approach would be to use optical transmission and switching, such as reconfigurable optical add/drop multiplexers (ROADM) or optical cross-connect (OXC), as much as possible.

(4) Mesh topology for shortest path and multi-path protection: Mesh topology has many benefits: reduction of the number of hops between endpoints, improved path protection, and increased network scalability. More importantly, due to the exponentially higher number of paths a signal can take versus a ring topology to its destination, network quality is dramatically improved, moving the network towards six 9s availability.

“At the Root of It All”

Optical Transport is the network layer that delivers on the services and features that consumers want. Hence, any upgrades or addition of new services to end users will require changes in the optical layer. Using our tree analogy: there is no tree without the roots, and there is no network without optical transport. Therefore, to support all the next generation of services (5G Advanced, F5G Advanced, AI/ML applications, and DCI) that operators and cloud service providers are rolling out and ensure a high-quality of experience, the optical transport layer must also be upgraded.

There were a number of announcements by service providers confirming that 1.2 Tbps-capable devices are ready, and that they themselves were looking forward to these new high-performance transponders. Three of those announcements were as follows:

There were a number of announcements by service providers confirming that 1.2 Tbps-capable devices are ready, and that they themselves were looking forward to these new high-performance transponders. Three of those announcements were as follows: