After spending a few days at OFC 2019, I sat down and read through the notes I took during each meeting at the conference and concluded that I have fewer pages of notes for this OFC than in the past two OFCs attended. Kidding aside…This lack of notes was in no way an indication of the meeting quality. They were great meetings with a lot of information exchange. It was, however, an indication that nothing was “really” new at this conference from the past two conferences. In fact, at times, I felt a sense of Déjà vu.

At the conference 600 Gbps and 800 Gbps coherent optical components, DSPs, and systems were re-affirmed with samples, demos, and timelines. As I understand it, the timeline for system availabilities are as follows:

- 600 Gbps capable coherent line cards

- Cisco’s NCS 1004, Infinera’s Groove G30 using Acacia’s DSP will be available by the end of March 2019

- Fujitsu’s 1Finity T600 using NEL’s DSP was available one week before OFC

- Huawei’s OSN with an in-house DSP will be available by end of March 2019

- Nokia’s 1830 PSI-M with an in-house DSP will be available in 3Q 2019

- 800 Gbps capable coherent line cards

- Ciena is targeting the end of 2019 (I’m guessing last month of 2019)

- Huawei by end of 2020 (I’m guessing last month of 2020)

- Infinera is targeting 2H20 (I’m guessing the first month of 4Q 2020)

Nearly everyone talked more about 400 Gbps ZR in a QSFP-DD or OSFP form factor this year. This was the same as last year. However, now both Ciena and Infinera have announced plans for developing and manufacturing 400G ZR. So, there are definitely more companies interested in making and selling 400G ZR. We should see 400G ZR products and demo in OFC 2020.

The most interesting item I saw at OFC this year was probably a new product that Fujitsu is developing that they call Trans Lambda. It sounded like the company needed a couple more years to develop the product, but the concept was quite unique. The premise is that as the optical world hits Shannon’s limit, the use of L-band will increase. So, Fujitsu is working on a box that can shift C-band signals to L-band without an optical-electrical-optical conversion. I’m looking forward to hearing how this technology develops and fits into the optical market in the future.

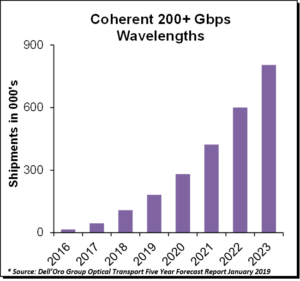

to approach $80 billion over the next five years. The majority of the Optical Transport revenue will be driven by demand for coherent 200+ Gbps wavelengths.

to approach $80 billion over the next five years. The majority of the Optical Transport revenue will be driven by demand for coherent 200+ Gbps wavelengths. We just wrapped up the 3Q 2018 reporting period for all the Telecommunications Infrastructure programs.

We just wrapped up the 3Q 2018 reporting period for all the Telecommunications Infrastructure programs.